Ask any successful long term investor about what he/she looks in a business. A majority would list at least half a dozen key characteristics like:

I have not come up with something new or unique here.

Instead, in this post, I will just pick one of the above characteristics and go deep.

And I pick Debt for this post.

What is Debt?

Debt is an important metric to judge the financial health of an individual or a corporate balance sheet.

Investopedia defines debt as follows:

“Debt is an amount of money borrowed by one party from another. Debt is used by many corporations and individuals as a method of making large purchases that they could not afford under normal circumstances. A debt arrangement gives the borrowing party permission to borrow money under the condition that it is to be paid back at a later date, usually with interest.”

So, from the above definition we understand that there are two types of debt:

- Personal Debt: Debt which is taken by individuals like you and me to make large unaffordable purchases like house property, a car, higher education, etc.

- Corporate Debt: Debt which is taken by corporations to make a large capital expenditure for making their businesses sustainable and grow.

Now let’s dive into probably the best resource to understand more about debt in the investing world.

And that valuable resource is arguably the most well-known investor of all time- Mr. Warren Buffett.

Buffett on Personal Debt

When asked for just one advice by a 14-year-old shareholder at the 2004 Berkshire Hathaway annual meeting, Buffett said,

“it would be just to don’t get in debt,”

“It’s very tempting to spend more than you earn, it’s very understandable,” he said.

“But it’s not a good idea.”

“And if you’re deep in the red, it may be a good idea to never look at a credit card the rest of [your] life,” Buffett added.

This was on Personal Debt, now let’s see what he says about debt taken by corporations.

Buffett on Corporate Debt

Our consistently-conservative financial policies may appear to have been a mistake, but in my view, they were not. In retrospect, it is clear that significantly higher, though still conventional, leverage ratios at Berkshire would have produced considerably better returns on equity than the 23.8% we have actually averaged. Even in 1965, perhaps we could have judged there to be a 99% probability that higher leverage would lead to nothing but good. Correspondingly, we might have seen only a 1% chance that some shock factor, external or internal, would cause a conventional debt ratio to produce a result falling somewhere between temporary anguish and default….. We wouldn’t have liked those 99:1 odds – and never will. A small chance of distress or disgrace cannot, in our view, be offset by a large chance of extra returns. If your actions are sensible, you are certain to get good results; in most such cases, leverage just moves things along faster. Charlie and I have never been in a big hurry: We enjoy the process far more than the proceeds – though we have learned to live with those also.— 1989 letter to investors.

Buffett further argues against debt on balance sheet in his 2005 letter to investors:

We are not interested in incurring any significant debt at Berkshire for acquisitions or operating purposes. Conventional business wisdom, of course, would argue that we are being too conservative and that there are added profits that could be safely earned if we injected moderate leverage into our balance sheet….

Maybe so. But many of Berkshire’s hundreds of thousands of investors have a large portion of their net worth in our stock (among them, it should be emphasized, a large number of our board and key managers) and a disaster for the company would be a disaster for them…

Any other approach is dangerous. Over the years, a number of very smart people have learned the hard way that a long string of impressive numbers multiplied by a single zero always equals zero. That is not an equation whose effects I would like to experience personally, and I would like even less to be responsible for imposing its penalties upon others.

That’s enough historical evidence for us to shun companies with high debt on books. In fact, most investors (including myself) have a quick mental checklist of looking at the debt levels first in any company we track. We tend to quickly get biased against a company that has a high debt on books.

But have we ever thought what do we actually mean by high debt?

And what is the level of debt we are comfortable with?

Keep the above questions in mind before proceeding further. I will come to the answers a little later. Let me first dwell on something else.

Many of us use screening tools to look for new investment prospects. A typical long term investor would put something like this on a screener:

- ROE> 18%

- Market Capitalization > 500 Cr

- 10 year Sales growth CAGR >10%

- 10 year Profit growth CAGR >10%

- Debt < 0.5

I am not saying everyone would exactly put the above conditions. But broadly we look for similar traits.

I ran that on the screener and the results were obvious. The list of 61 companies mostly contained really good businesses that have created long term wealth for its shareholders.

But then, I just thought for a moment, are these the only companies that did well in the last decade or so?

Of course not.

There would be many companies that would not have met the above conditions but still managed to do well. For example, a company might be generating an ROE of 15% but higher Sales and Profit growth rate of > 20% CAGR for the last ten years.

Similarly, there might be companies that have a slightly higher debt on books. However, these companies might have used the debt efficiently in a way that could give them the advantage of leverage but managed to avoid the debt-trap.

This is where I want to address the above two questions about high debt and comfortability with it.

A simple answer to the first question on high debt can be:

A high debt company is where the business is incapable of generating enough cash for making the interest payment on the loan.

Similarly, an answer to the second question on debt comfortability can be:

A company would be comfortable with that much amount of debt, which it can service and repay through its internal accruals.

A thumb rule which many of us use is – if the Interest coverage ratio is more than five, the company is generating enough to pay off the interest on the debt. This doesn’t guarantee that the company would not default, but it increases the probability of servicing the debt without much pressure at present.

I thought why not invert the whole idea of debt-free or low debt companies and find companies which are having a decent amount of debt (debt to equity ratio of more than 0.5) but have the financial muscle to service that debt.

So, I ran another screen with the following conditions:

- Debt to Equity > 0.5

- Interest Coverage Ratio > 5

- Market Capitalization > 500 Cr.

I got 49 companies on this list. And when I sorted the list in the order of maximum returns generated in the last 5 years, the top 20 names were:

- Minda Inds.

- Aarti Inds.

- Kama Hold.

- Black Rose Indus

- DFM Foods

- Fermenta Biotec.

- Jubilant Life

- Hester Bios

- SRF

- JK Paper

- Safari Inds.

- West Coast Paper

- V I P Inds.

- Apollo Tricoat

- Sudarshan Chem.

- Lumax Inds.

- Titan Company

- Balrampur Chini

- Engg.Ind.

- Sundram Fasten.

All the above 20 companies have given CAGR returns between 20% and 57% in the last 5 years. The above list was made on 24th December 2019. So it takes into account the fall in the broader market in the last two years as well.

Maybe not all, but many of the above 20 companies do have a very good business with long term potential to grow consistently.

I won’t recommend you to screen companies like this. Because just being able to manage debt is not enough for a company to be termed as a great investment opportunity. There are several other important factors like the business model, industry characteristics, management track record and so on. And we have not talked about valuation, which is another very important metric for making an investment decision. The point I am trying to prove here is that when you look at a screener and put in the regular conditions of high ROE and low debt and stuff like that, you would be missing out on some really good businesses.

Don’t blame your screener tool for that. You have to do the hard work beyond the simple initial screening.

Read the annual reports of companies.

Try to understand the business dynamics and industry scenario.

And then try to figure out what is working or not working for a company.

There is no doubt that the best businesses are those which hardly require any outside capital to grow themselves. In fact, these businesses generate so much cash year on year, that they have no other option but to return a significant part of the capital to the shareholders in the form of dividends and buybacks.

But there is one problem.

Almost everyone knows about them.

In a digital world where business information travels so fast through social media and online stock screeners, all of us would know about those companies and hence the valuation of those companies would not be attractive from the return potential. So, the odds of multiplying wealth from them would be low due to the high entry valuations.

That is about the best businesses.

The worst businesses are those which are so heavily laden with debt that they can hardly survive.

Between these two types of extreme businesses, there are some good businesses that have decent economics. They may not show up on your stock screener. Because they do not pass your stringent test conditions. But they are not inherently bad businesses. There lies the opportunity for you to go deep and find this scrip if the broader market has not discovered it yet. And if you can dig in and find something which the market as a whole does not understand or appreciate today, you have an edge.

One way of creating an edge for yourself is to look at debt on the books of the company and ask the following questions:

- Is the debt on the books comfortable for the company to manage? (Interest coverage Ratio discussed above)

- How does the company plan to pay back its debt? (Internal accrual or by issuing new debt)

- Is the long term debt used for the working capital requirements or capital expenditure? (Long term debt for short term needs like working capital is a recipe for disaster)

- Is the company producing sizeable cash from operations to pay back the debt and also invest in Capex? (If Cash Flow from Operations is negative or close to zero, it is a sign of trouble)

- How has the management fared in terms of managing debt in the last few years? (Any default or delay in the past?)

- Do you think the situation has changed for the better or worse in recent years? (Management has become more aggressive or conservative compared to the past)

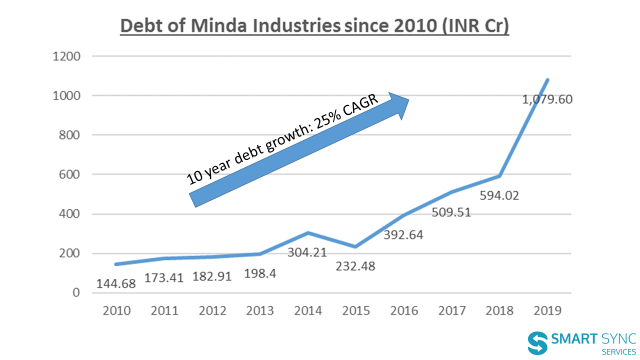

Let us take the example of Minda Industries which sits at the top of the above list. Let me share some data about the company’s past performance.

That’s a staggering amount of debt getting increased on the books year after year. Debt from the year 2010 till 2019 has grown at a CAGR of 25%.

No investor would feel comfortable with it. Right?

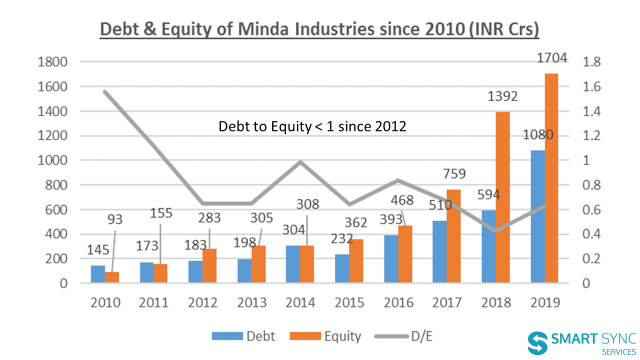

Now let me share some more data about the company.

While the debt has grown at a CAGR of 25%, equity has grown at a CAGR of 38% in the same period. Hence, the Debt to equity ratio did not move beyond 1 after 2012.

Now by taking other data from the screener, I calculated the interest coverage ratio for the same period.

Interest coverage ratio = EBIT/Interest

For my calculation, I have taken EBIT = Operating Profit Less Depreciation.

I have not included other Income in my calculation of EBIT.

Some people use EBITDA for interest coverage ratio, which gives a much higher interest coverage ratio.

However, let us be conservative and take EBIT for our calculation.

The following picture turns up:

If you look at the numbers, Interest coverage was pretty low (<5) until 2016. But from 2013 onwards, it is consistently rising and in a very comfortable position from 2016.

Now, assuming that

You understand the business of Minda Industries.

You are confident about the industry’s long term potential.

You know that in the last 10 years sales have grown at a CAGR of 28% and profit has grown at a CAGR of 32%.

In FY16 numbers, you see that the interest coverage ratio number is very comfortable,

And you see that the stock is available at less than 15 times trailing earnings at that time.

Do you still not buy it because it does not appear on your screener as you had put a condition of debt to equity ratio of less than 0.5?

I think, not buying the stock at that time would be a costly mistake.

In May 2016, the stock was quoting at Rs. 70, today it is at 350. A 5 bagger in three and a half years.

Minda Industries above is just one example, there have been many other examples from different industries where the companies have managed to do exceedingly well with some debt on their books which they have the ability to service comfortably. And we keep on ignoring them as we are blinded by our stringent condition of only looking for debt-free companies.

I have nothing against debt-free companies.

Rather I continue to believe that if you can find debt-free companies with a solid business model and growing earnings at a reasonable valuation, there is nothing like it.

However, we all know, satisfying all the above conditions is not possible for every company most of the time.

We must also remember that almost all investors like us are not Warren Buffett. We do not have the liberty of holding a large amount of cash in our portfolio for a very long time. We have to put them to work and hence the opportunity cost for such a miss like Minda Industries is huge.

When I look back into my journey as an investor for about a decade now, I think I missed a lot of opportunities like these by relying a little too much on the screeners in the early part of my investing career.

And I have also observed that even though I do not specifically go by screeners now, there are certain investing traits so ingrained at the subconscious level of my mind that I still find it difficult to get over with.

Looking at debt on books of any company in an objective manner is one of them. Whenever I see a 500 Cr debt in a balance sheet, a strong bias against the company creeps in my brain. That is what I am trying to overcome.

We should not see debt as a burden that is hampering the company’s growth. Rather we should follow the remark by Warren Buffett that “leverage just moves things along faster” which shows that debt acts as a booster for any company like nitrous for a car. Whether the company will be able to use this booster to zoom past its hurdles or crash to the side is entirely dependent on the management or the driver at the helm.

So, what are the key takeaways from this post?

- Screening tools are the starting point and not the endpoint.

- As an investor, if you have not seen multiple market cycles, be flexible. Don’t be too rigid on your investment selection criteria.

- High-debt is bad, but taking some debt on books is not a crime.

- Look for cues where debt has been consistently managed well by a business over long periods.

- And keep looking for opportunities, it can come from anywhere.

Happy Investing!!!

Disclaimer

Stocks discussed in this post are for educational purposes. Please do not take it as a recommendation. Please read our terms and conditions.

Related Posts

How to Find Emerging Moats — From the Lens of an Investing Legend