Ramesh, an IT Engineer in USA’s Silicon valley is worried. He has lost his job a month back & is now planning to return to his home country India. He knows the impending recession & the job cuts in the technology sector would make it difficult to find another job in the United States. He thus has to move his family back to India, find some rented accommodation in Hyderabad or spend the days with his parents in a small town till he lands up a new job. His strong resume built over the years is granting him comfort, but how will he make ends meet, is the worry.

Compare that to Suresh, an IT Engineer in India’s Silicon valley Bangalore. He also has lost his high paying job in the startup & is looking for a stable job in some MNC. But Suresh is not worried as he has given himself 5 months to search for a good job. He also plans to do a short up-skilling course if he doesn’t land a job in a month.

Before you guess or ask why Suresh is worry free, let me bring your attention to one fundamental aspect of life. Uncertainty! Life is uncertain & equally unpredictable, in spite of our best efforts to harness certainty. You can have a plan for your goals & aspirations. But no plan can be perfect when it comes to dealing with uncertainty. Coming back to Ramesh & Suresh. Loss of income is the uncertainty that both are facing but what makes Suresh so carefree?

Emergency Funds.

Well for beginners, emergency funds is money kept aside for the rainy day. Because, when the weather turns bad, it doesn’t just rain, it’s a downpour. Think about Ramesh. A loss of income is one problem. That is compounded by the task of moving countries, finding accommodation, settling his family, kids education etc.

In short to quote Shakespeare:

Source: www.azquotes.com

An emergency fund is the seat belt in the car that protects you from sudden jerks due to potholes or larger accidents on the road. Although emergencies are majorly unplanned, there are some which you can predict quite well. Say, breakdown of your old vehicle that will need an eventual replacement. Instead of buying on EMI, have an emergency fund.

Here are some common emergencies that can put your financial health in jeopardy:

- Pay cut

- Demotion

- Loss of job

- Breakdown of vehicle

- Sudden medical surgery

- Shifting to a new location

- Immobility due to accident or health issue

- Major unplanned house repair/renovations

The natural reaction to such emergencies is to swipe out the credit cards, delay some investment or borrow from friends. The more worrisome are taking a loan, redeeming an investment, distress sale of an asset. Moreover, financial distress leads to emotional distress. An emergency fund is your insurance to avoid such ignominy.

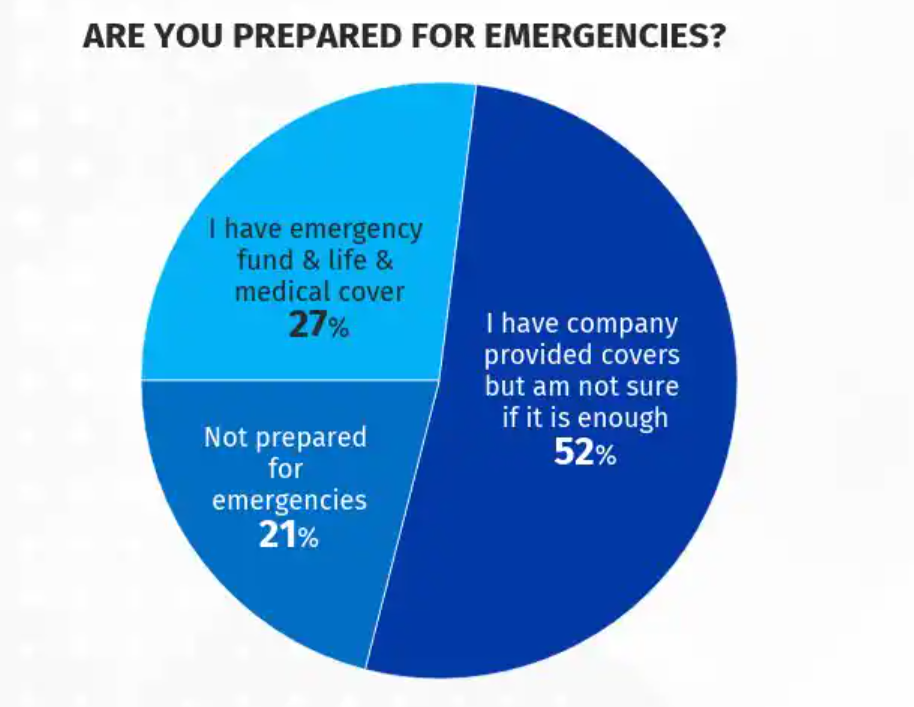

There is another reason to have an emergency fund. I am sure, you would have come across people who have kept lakhs of Rupees in a savings bank account. Ask them why & you get the response:

“Kya pata kab jarurat pade!” meaning, for uncertainties. Observe, in majority of the cases, these people are also equally afraid to invest their money. Here’s a stat from a survey conducted by Finsafe India based on responses of 5769 salaried individuals in India.

Source: www.moneycontrol.com

An emergency fund, ensures you are stress free about dealing with the uncertainties. That frees up your mental & financial energy to tackle other aspects of personal finance like insurance & investments.

Source: Let’s Talk Money by Monika Halan

With this primer, let us look at some of the features of an emergency fund.

Features of an Emergency Fund

The fund is to be used for uncertainties that are… well uncertain! So, you can never accurately know how much is too much & how much is enough. The best way to estimate the emergency fund’s size is to record your expenses. That is budgeting. If you haven’t read our other blog on Basic Tenets of personal finance, then this is probably the right time. Head over to it, here.

So, budgeting will tell you where & how much you spend. Segregate the mandatory expenses. For a student those could be fees & study material, for a bachelor it could be his housing rent & bike maintenance etc. These are expenses that are essential to live your daily life. The emergency fund should ensure these expenses don’t suffer, in case you lose your source of income. Now, there’s a simple thumb rule to start with:

Emergency fund size = 6 x monthly expense

How did we arrive at that? This thumb rule is just a safe estimate to start with. The predictability of your income & the probability of it’s loss should determine this. Let’s take the example of Suresh, working in a startup. A startup generally works with a handful of customers and if the startup happens to lose a couple of them, they are bound to be in trouble. Hence, Suresh could have a higher probability of losing his job than a person working in an established MNC. Again, Suresh’s job profile, his replacement value in the organisation all need to be factored in. Individuals having a working partner can afford to have a less corpus for emergencies. An individual starting out in his business should have a higher emergency fund than an individual who is starting out a job. Remember, we are talking about emergency funds, a basic tenet of personal finance.

An emergency fund’s size is hence, entirely personal & you are the best judge to tweak the thumb rule.

Now uncertainties don’t follow a schedule, plan or timing. Emergencies & misfortunes strike at the most inopportune moment. The emergency fund must have the highest form of accessibility. No! That doesn’t mean you stash cash below your pillow.

Source: https://www.dreamstime.com/

It means having your money in instruments that don’t have a lock in period. The money should be available as quickly as possible.

Some of these instruments are:

- Liquid cash

- Savings account with a debit card

- Fixed deposits accessible from internet banking

- Fixed deposits with auto-sweep in facility

- Liquid funds with a debit card facility

Notice how these instruments earn some of the lowest interest rates. The liquid cash keeps losing its value to inflation & the savings account interest rates are no match to it either. Fixed deposits are not tax friendly for people in high tax slabs, while liquid funds don’t generate inflation beating returns. The purpose of an emergency fund is never to earn returns, but to have a safety net. This means we need regular replenishment of the emergency fund.

Regularly review expenses & re-calibrate the size of the emergency fund accordingly. Expenses increase as you move through different phases of your life e.g. a student, bachelor, married, parent etc. As the saying goes:

Source: www.achronicvoice.com

So, every new phase of your life requires a different size of emergency fund. The best way is to allocate some part of the lump sum amounts you receive once a while, e.g. annual bonus.

Let’s understand how you should build an emergency fund?

Building an Emergency Fund

For newbies who have just taken baby steps in their career, it’s prudent to start allocating a fixed sum every month for the emergency fund. Start slowly but surely.

Some of the best ways to keep an emergency fund:

- Have a separate bank account and transfer a fixed sum to it each month.

Pro-tip: Have a standing instruction to transfer the fixed money. - Start a recurring deposit in the existing savings bank account

Over the months you would have a sizable corpus for emergency funds. With every rise in income, allocate more money to the fund, till you have the desired corpus.

It’s that simple.

But what is not simple is to stop using the fund for something which is not an emergency. Say for an impulse purchase. Our minds are prone to multiple biases when out in the market & having a sizable sum of money lying in the account, could tempt you to use it. Well, if you wish to learn how you can be fooled by your own biases, head over to our other blog here.

To ensure you don’t spend the emergency fund, it’s best to have a separate bank account or FD. Don’t keep this money in the account from where you do your routine transactions. Further, mentally label it as an Emergency Fund. So, whenever you refer to it, refer with the name. If the account has a debit card (ideally, it should have), paste a sticker with the name written in big bold letters: “Emergency Fund”. You can also add some more flavour to it by adding a tagline like: “To turn crisis into convenience!”

Monika Halan, journalist, writer & author of the book Let’s Talk Money, says that:

“A name gives something an identity & we hate to violate that identity.”

Hence, assigning a name ensures you don’t use the money for some other purpose.

Where to keep the fund?

An emergency fund’s purpose is never to earn returns. So, never invest that money in equity, long term debt instruments, illiquid assets such as gold. However, you also can’t just let that money lie idle in a savings bank account.

Set up a Fixed deposit (FD) through internet banking. Park about 50% of your emergency corpus here. Note, an online FD, can be assessed quickly, and most banks let you have the money almost immediately. Make sure you are aware how much time it takes for the money to be available. 25% of the emergency corpus can be kept in a savings account. Some banks offer the option of sweep-in FDs or Multi-option Deposit (MOD).

Basically, an amount above a certain threshold in the savings account, is converted into an FD. Say you have Rs. 10,000/- in the savings account & Rs. 30,000/- in the sweep-in FD. You happen to withdraw Rs, 25000/- using the account’s debit card. Rs. 10,000 from the savings account will be consumed and Rs. 15,000 from the sweep-in FD would be withdrawn automatically.

Remaining 25% of the corpus can be kept in a liquid fund, ultra short term or short term debt fund. These mutual funds earn better returns than a typical FD and are more tax friendly. They can transfer money to a bank account within a day or two of receiving the redeem (withdraw) request. As we said earlier, some liquid funds also offer the option of a debit card, that can allow withdrawal of money (up to a limit) through an ATM card.

Conclusion

So, dear readers, an emergency fund is certainly a necessity. It would be a liability if you let the money lie idle in your savings bank account. Park this corpus in the right instruments, ensuring ease of accessibility & liquidity. Last but not the least, share the details of the bank accounts, debit card, mutual funds, with your closest family member. Ensure, they are able to operate them & access these funds, in case you are not in a position to.

Review, re-size & replenish this fund periodically. Of course, never forget to restore the fund, once you have used it for some emergency! Calculating the size of the emergency fund is the vital part & there are thumb rules to guide you. But, there is no one size fits all in personal finance.

Reach out to Smart Sync Services & ZenNivesh to help you chalk out the perfect size of emergency funds customised as per your financial profile. Not only this, we are committed to serve all your financial planning needs under a single roof!

This was Part-III of our Samadhana series on attaining financial zen and a follow-up to our earlier post – “The Basic Tenets of Personal Finance“.