About the Company

VIP Industries Ltd is an Indian luggage maker which is the world’s second-largest and Asia’s largest luggage maker. The company has more than 8,000 retail outlets across India and a network of retailers in 50 countries. VIP’s products are imported in numerous other countries. It acquired the United Kingdom luggage brand Carlton in 2004. It also owns the Aristocrat and Skybags brands which are very popular in India.

Q4FY23 Update

Financial Results & Highlights

Detailed Results:

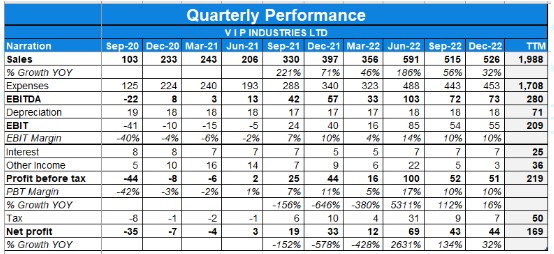

- Q4 revenues grew by 27% YoY at Rs. 451 Cr vs Rs. 356 Cr the previous year.

- Q4 EBITDA margin stood at 15.1%, up 4.5% YoY with PBT being at Rs. 41 Cr, up 154% YoY.

- FY23 consolidated revenues stood at Rs. 2081 Cr ( up 61% YoY), EBITDA margins at 15.8% (up 2.1% YoY), PBT at Rs. 229 Cr (up 165% YoY) and PAT at Rs. 152 Cr (up 128% YoY).

- The company’s split for sourcing of goods for FY23 stands as:-

- Own Manufacturing :- 70%

- Controlled Manufacturing(In India) :- 20%

- China :- 7%

- 3P sourcing :- 3%

- Q4 revenue reported an all-round growth of 27% YoY (volume 27%) and 45% over base (volume 40%).

- Gross margins reported sequential improvement of 8.4% and YoY improvement of 4.6%, mainly on account of operational efficiencies combined with favorable raw material prices and ocean freight.

- Q4 overall expense is at Rs. 196 Cr as compared to Rs. 157 Cr last year in line with increased operations.

- Net Debt at on Mar’23 stood at INR 122 Cr vs 61 Cr the previous year. Working Capital Days went down to 89 days from 126 days the previous year.

- Investments in own manufacturing were at INR 100 Cr in FY23, which is planned to go to INR 200 Cr in FY24.

- The Channel Wise Revenue salience for Q4FY23 and FY23 stood at:-

- The Brand Wise Revenue salience from brands from Q4FY23 and FY23 stood at:-

- The Category Wise Revenue salience for Q4FY23 and FY23 stood at:-

Investor Conference Call Highlights:

- The management states that fundamental cost efficiencies and the much-awaited softening of all input costs, helped the gross margins for Q4. Gross margins for Q4FY23 stood at 58%, with the gain of 843 basis points sequentially and 459 basis points YoY.

- The company had to take the final hit of the Future group outstanding, with the charge-off in terms of doubtful being Rs. 23 Cr for the year.

- The company faced an unfortunate incident of fire that burnt one of the factories in Bangladesh. While it has a full insurance cover for the quarter and for the year, the company has booked an exceptional loss of Rs. 47.2 Cr on account of loss due to fire.

- The company invested INR 100 crore in manufacturing CAPEX during the year and plans to invest INR 200 Cr in the current FY.

- The company’s traditional trade distribution has crossed the 1,200 town mark in FY23. The management plans to continue its penetration to target covering all 50,000 population towns by the middle of next FY.

- During the year, the modern trade channel had huge setbacks due to the closure of Future group accounts, the company covered up for the loss of stores and made up their growth through other store chains.

- The company has gotten the firm BCG onboard for consulting, to accelerate the E-commerce growth.

- The management is very positive about the overall current demand scenario and lead indicators for demand.

- The management gives guidance in the range of 53% to 55% for the company gross margins.

- The management gives guidance in the range of 17% to 18% for the company EBITDA margins.

- In regards to a previous fire damage that the company had faced, the management states that the claim is expected to be received in the next two to three months.

- The management explains that Capresse is a fundamentally positioned in the premium segment, and not in the luxury or super-premium segment. This is helping the company to trend more towards the masses while playing in the 2000 to 4000 ASP bracket.

- The management explains that Q4 having the lowest revenues, did not see operating efficiencies kick-in along with a 12 Cr provision for doubtful debts, which made expenses higher.

- The company has 8 factories in Bangladesh, out of them 1 got completely burned down to the fire incident. To cover-up, an outsourcing stopgap arrangement within India has been made along with accelerating pipeline of future capacities in Bangladesh.

- The management states that the burnt Bangladesh factory will take time to get rebuilt, but in lieu of that, the space in other factories that were coming up have been made operational. There was a monetary issue of supplies for four to six weeks which has been covered up.

- The management states that they have very aggressive and robust plans in the mid-premium and premium segment under the VIP Skybags and Carlton brand.

- The 200 Cr capex guidance given for FY24 will be for manufacturing sites and for plant and machinery. 70% of it will be for Soft luggage mainly being backpacks and DFT.

- The management is looking to enter the backpack segment priced below INR 1000 MRP. It sees the entire backpack area to be a very large growth area in the current FY and coming years for the company.

- The management states that from a go-to-market point of view, it is aiming at making Capresse a very dominant Ecommerce brand initially.

- The management sees the current FY to be mainly driven by backpacks and the premium side of the portfolio.

- The management expects the in-house manufacturing to further improve working capital efficiency bringing it down from 90 to 75 days in the next 18-24 months.

- Out of the 300 EBOs outlined by the company, the majority will be franchisee-led at 80%-85%.

- For industry guidance, over the next two to three years the management expects overall growth rate at 8%-10%, with the organized sector having accelerated growth at an upward of 15% for the next few years.

- The capex investment for FY24 will be a combination of both greenfield and brownfield in India and Bangladesh. The management is also looking in the north to put up an integrated plant.

- The guidance for growth in the core luggage category is at 15% by the management.

Analyst’s View

VIP Industries Limited is amongst Asia’s leading manufacturers and suppliers of luggage, backpacks, and handbags and the market leader in the organized luggage segment. It witnessed a good quarter with 24% YoY revenue growth and negative PAT due to booking a one-off loss.

At VIP, premium portfolios have started to kick in as the company has gone very high on driving the value portfolio. The overall commodity and raw material prices are softening, the ocean freight is much lower than before, so it may not have kicked in into the business as of now, but it will as we go ahead. So on one side, the tailwind is prices coming down, on the other side the headwind is also the mix and the value category growing and the unorganized sector pushing the growth further progress in terms of backward integration. VIP remains to be a very important company for the near future to track.

Q3FY23 Update

Financial Results & Highlights

Detailed Results:

- The company had a 32% revenue growth over last year

- gross margin sequential improvement of almost 1.3% and Y-O-Y improvement of 0.5%.

- Q1 FY23 saw a 5% growth, thereafter in Q2 FY23 scaled it up to 25% and the company now (Q3 FY23) continues to be at 20% plus.

- The management stated that the volume growth on the business has been quite good i.e. 25% year on year and almost 18% over base.

- The organized sector share has increased from 45% in FY19 to 56% in FY22,

Investor Conference Call Highlights

- The management states that the volume growth is happening on a completely altered supply chain at VIP.

- The management talked about some exciting launches that happened in their portfolio during this quarter.

- Skybags did a FIFA collection, VIP had a Highlander which is a rugged hard luggage and in Carlton, they launched a couple of premium soft luggage ranges and icing on the cake was their launch in Caprese with a range of products by Manish Malhotra.

- Skybags did a FIFA collection which did very well. In VIP we had a Highlander which is a rugged hard luggage. In Carlton, we launched a couple of premium soft luggage ranges and icing on the cake was our launch in Caprese with a range of products by Manish Malhotra.

- The management states that the company faced some challenges in Q1 FY23 because of the future group issue. It also stated that by the end of december a large part of the future group stores that got shut had started coming up.

- the management stated that modern trade is moving beyond its expected numbers in the year and also above its base without future group

- The company has launched its direct to consumer (D2C) website and have started to get green shoots on the whole D2C business of Caprese

- The management states that in UAE the company is starting to get double digit market share in chains like Carrefour and Lulu because of channels.

- The management talks about the category performance that hard luggage continues to dominate in the recent past, but they have started seeing some change of that in terms of soft luggage coming up and with their supplies picking up in soft luggage.

- The management states that 73% of their volumes in Q3 FY23 were supplied by their own manufacturing facility in India and Bangladesh. In a way, this has been the highest ever ratio reported in any quarter.

- The company’s capacity has now increased to 65% since the pandemic and this year they would be investing almost Rs. 100 crore in this financial year only to increase their capacities. This is almost equally split between India and Bangladesh in terms of Rs. 50 crore reach

- The management states that the reason for improvement of gross margin is largely the prices of raw material and ocean freight.

- EBITDA margin flow through from above has been lower, one large reason other than increasing in advertisement is the provision the company did on all the future group doubtful debt that’s almost taking out 1% out of the EBITDA

- The management states that there is a seasonality factor that plays a major role in e-commerce driving the revenue up.

- The management states that the lower tax rate is on account of the receipt of dividend from Bangladesh which they are in turn giving it back to their shareholders. The effective tax rate is going to be around 18% to 19% for the year.

- The management claims that there is a higher demand in Tier 2 & Tier 3 and downward cities.

- For the Caprese brand the company is looking at the mid premium and the slightly above range, so anywhere between Rs. 2000 to Rs. 4000 range is what will be the mid part of what the brand should have.

- The management states that about 20%-25% will be outsourced within India and maybe have about 10% to 15% at the outer limit, this includes Caprese from China.

- The company is targeting a gross margins of around 52% to 53% in FY24 and EBITDA of 20 %

- the management states that the advertisement cost in Q3 FY23 was Rs 29 crore versus Rs 9 crore in Q3 FY22

- The company will target to invest 5-6% of its sales in advertisements.

- the management stated that the future group contribution modern trade was 44% pre COVID and now it’s about 20%-22%

- the company went strong in Vishal Mega Mart and some more entry into some more regional chain

- The company is looking at manufacturing trolleys and wheels subsequently to further make itself more competitive.

- The company is aiming to increase their intensity of spends in e-commerce with the other part of portfolio and pricing as well, so that is continuously happening.

Analyst’s View

VIP Industries Limited is amongst Asia’s leading manufacturers and suppliers of luggage, backpacks, and handbags and the market leader in the organized luggage segment.

At VIP, premium portfolios have started to kick in as the company has gone very high on driving the value portfolio. There used to be 279 big bazaars stores and today almost 235 stores are open i.e. 3/4th of those stores have come in, and therefore that’s going to hopefully help the company in the coming quarter. The overall commodity and raw material prices are softening, the ocean freight is much lower than before, so it may not have kicked in into the business as of now, but it will as we go ahead. So on one side, the tailwind is prices coming down, on the other side the headwind is also the mix and the value category growing and the unorganized sector pushing the growth further progress in terms of backward integration.

Q2FY23 Update

Financial Results & Highlights

Detailed Results:

- The company saw its revenue grow by a huge 56% YoY whereas PAT grew by 134% YoY.

- The company currently has 20 branches in 4 regions with geographical coverage of 1072 towns.

- Revenue Split by Source for the quarter:~

- Own manufacturing – 64%

- China – 11%

- 3P sourcing – 25%

- Hard luggage accounted for 67% of revenues while soft luggage stood at 33% of the Uprights revenue. Uprights revenue was 75% of the total revenue for Q2.

- Duffel Bags contributed 8% of the total revenue while Backpacks contributed 12%.

- Gross Margin for VIP was 48.1%, compared to 49.9% in the sequential quarter & 47.1% the previous year.

- Brand Salience for Q2FY23 was:

- VIP – 21%

- Skybags – 32%

- Carlton – 6%

- Aristocrat + Alfa – 37%

- Caprese – 4%

- International – 5%

- EBITDA margin was at 14.8% for Q2 vs 18.3% the previous quarter and 14.4% the previous year .

- Category Salience for Q2FY23 was:

- Uprights – 75%

- Duffel Bags – 8%

- Bagpacks – 12%

- Ladies Hand Bags – 4%

- Q2FY23 had 38 new launches in Luggage and 127 in backpacks.

- Company’s market share stood at 43% in the branded market in Q2FY23

- The company faced headwinds in terms of inflation and non-functional future group accounts.

Investor Conference Call Highlights

- The company’s strategy involving increasing the number of exclusive retail outlets has worked for the company beneficially.

- The company stands at a lower retail outlet count as compared to the previous year but has witnessed a growth in total revenue indicating a higher store throughput.

- The headwind in terms of future group not being active has been nullified as the demand has been caught very well in other modern trade chain stores.

- The board is not actively pursuing international business in its mega strategy and is focusing on just getting an inroad in some geographies.

- The company has expanded well in the middle east and more 7-8 countries. The international business currently stands at 5% of the total business as compared to 2.5% pre-covid era.

- The management states that the pent up demand witnessed recently is now middling-out. It was majorly contributed by a shift from the unorganized to the organized sector.

- The company is majorly focusing on premiumization of the brands and is having new launches for VIP and Skybags.

- For advertising of Skybags, VIP is connecting to GenZ through social media and other ways.

- The management states that gross margins witnessed minor erosions due to raw material costs and freight costs being at their peak in Q2FY23 which are expected to go down going ahead.

- The management plans to keep gross margins in the range of 50%-55% going ahead.

- The management states that an increase in the share of sales of Aristocrat brand will not affect the gross margins due to reductions in cost and increase in efficiency. The company can thus continue to play the value market share gain.

- The management states that the industry has been growing more on the value side and the value will grow faster going forward because of the unorganized to organised shift.

- The company has very aggressive plans for the Capresse brand. This includes being supremely active in the e-commerce area and activating physical channels and exclusive outlets.

- The company is continuously investing to increase its capacity in Nashik and Bangladesh. Currently, the company has invested to increase capacity base by 25%, covering for next year’s growth in sales.

- The management sates that organized players will have more advantage than unorganized players going forward compared to pre-covid for various reasons.

- The management states that the company is pursuing both market share and margins and projects 18%-20% EBITDA margins range for the longer period.

- The management maintains its revenue guidance for FY23 at 2000 crores.

- Benefit from reduction in crude oil and raw material prices have an effect on the company’s financial lagging upto five to six months.

- There were no further price hikes in the company’s products post the March hike.

- The company has a capex plan of INR 100 crore for FY23 and its own manufacturing stands currently at 65%, which will increase to 75% by the end of FY23.

Analyst’s View:

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. Luggage sales in all segments are picking up with the value segment growing very well and expected to grow very fast with the continuous shift from the unorganized sector to the organized sector. The management is also very confident that there are comparatively less issues regarding the supply of raw materials. It remains to be seen how VIP continues to strengthen its internals in the meantime and grow the eCommerce channel along with headwinds in the form of competition and price wars. Nonetheless, given the company’s strong brand image, leadership position in the industry and the tailwinds supporting its journey along with the resilient balance sheet of the company, VIP Industries can be a pivotal mid-cap wealth creator to watch out for.

Q1FY23 Update

Financial Results & Highlights

Detailed Results:

- The company saw its revenue grow by a whopping 186% YoY whereas PAT grew by 2631% YoY.

- The company currently has 20 branches in 4 regions with geographical coverage of 824 towns.

- Revenue Split by Source for the quarter:

- Own manufacturing – 64%

- China – 11%

- 3P sourcing – 25%

- Hard luggage accounted for 64% of revenues while soft luggage stood at 36% of the Uprights revenue. Uprights revenue was 71% of the total revenue for Q1.

- Gross Margin for VIP was 50%, compared to 53% in the sequential quarter & 51% the previous year.

- Brand Salience for Q1FY23 was:

- VIP – 23%

- Skybags – 30%

- Carlton – 4%

- Aristocrat + Alfa – 35%

- Caprese – 4%

- International – 5%

- EBITDA margin was at 18% for Q1 vs 11% the previous quarter and 12% the previous year .

- Category Salience for Q1FY23 was:

- Uprights – 71%

- Duffel Bags – 7%

- Bagpacks – 12%

- Ladies Hand Bags – 4%

- Export & Accessories – 6%

- Q1FY23 had 38 new launches in Luggage and 127 in backpacks.

- The company faced headwinds in terms of inflation and non-functional future group accounts.

Investor Conference Call Highlights

- Q1 was the first disruption free quarter for the company, especially during the peak season which benefited the company a lot.

- The company faced an approx 24% inflation over the same period last year. This is putting a pressure on profitability and in some cases acting as a demand dampener.

- Going forward, the management is confident about the demand environment remaining stable, while inflation and the future group channel will continue to put pressure on the company.

- The volume growth of this quarter has been 8% on a pre-covid base.

- The management is comparatively seeing softness in the raw materials currently but there is still high inflation in other raw materials and components.

- The company faced many disruptions on the raw materials front in China in Q1.

- The company states that for now it will have to continue buying finished goods on the high fashion portfolio for Caprese and backpacks.

- The company plans to add 120-150 EBOs during the year. Out of this, the company has added 21 stores in Q1 and signed up more 23 stores during the quarter.

- The management is confident of maintaining the run rate of adding approx 35 EBOs every quarter to reach the goal of adding 150 EBOs during the year.

- EBITDA margins have taken a hit compared to pre-pandemic levels mainly because of pressure on gross margins due to inflation.

- The management gives a guidance of maintaining 18-20% EBITDA margins for the year.

- The management is very optimistic and confident about the future.

- The company is facing margin dilution in some cases due to consumer demand increasing in the value segment.

- The value segment is witnessing a tailwind which the pandemic has got in with the unorganized market yielding into organized.

- The management admits that it made a mistake by delaying the launch of the new collection of backpacks. This has led to the difference in backpacks salience pre-covid to now.

- The management states that its business with domestic production is not very capex heavy with the payback period being 18-24 months. With that, the ROCE is 30%.

- For the current year, the company has a capex plan of 50 crores to use for the Bangladesh and Nashik facility.

- Currently exports stand at 5% of revenues with the company exporting to 20+ countries.

- The management is focusing on the Middle East and GCC countries for growing exports. The company had a change of channel partner in UAE and recently entered the Saudi market.

- The company has received interim payment of 15 crores for their fire insurance claim. The management expects 41-45 crore to arrive in total by Q3FY23.

- In online performance, the company has grown by 50% on a 19-20 base.

- The A&P spends for the year would be at 5%-5.5% of revenues.

- The management explains that as the market moves towards the value end as consumer spend consciously, the company will be focused on getting its costs right and play the value segment too profitably.

- The management states that compared to pre-covid, the competition has only intensified and they expect it to intensify more as penetration of the organized sector increases.

- Seasonality of demand is still there but it is over a longer horizon, this is because of changing preferences from summer vacation to mini-vacations, and marriage dates becoming more open and flexible than before.

Analyst’s View:

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. Luggage sales in all segments are picking up with the value segment growing very well. The management is also confident that there are comparatively less issues regarding the supply of raw materials. It remains to be seen how VIP continues to strengthen its internals in the meantime and develop the eCommerce channel along with headwinds in the form of inflation & future groups’ current financial health. Nonetheless, given the company’s strong brand image, leadership position in the industry and the tailwinds supporting its journey along with the resilient balance sheet of the company, VIP Industries can be a pivotal mid-cap wealth creator to watch out for.

Q4FY22 Update

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 352 | 258 | 36.4% | 398 | -11.6% | 1304 | 672 | 94.0% |

| PBT | 13 | -16 | -181.3% | 37 | -64.9% | 84 | -112 | -175.0% |

| PAT | 9 | -12 | -175.0% | 27 | -66.7% | 64 | -84 | -176.2% |

| Consolidated Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 362 | 259 | 39.8% | 407 | -11.1% | 1326 | 667 | 98.8% |

| PBT | 16 | -6 | -366.7% | 44 | -63.6% | 86 | -125 | -168.8% |

| PAT | 12 | -4 | -400.0% | 33 | -63.6% | 67 | -97 | -169.1% |

Detailed Results:

- The company saw its revenue grow by 40% YoY whereas decline by 11% QoQ.

- Hard luggage accounted for 62% of revenues while soft luggage stood at 38%.

- Gross Margin for VIP was 53%, compared to 49% in the sequential quarter & this increase was on account of higher prices, product mix in favour of VIP & Skybags & higher contribution from its Bangladesh’s manufacturing plant.

- EBITDA margin was at 10.6% for Q4.

- The company has consolidated cash & cash equivalents of Rs 61 Cr as of March 2022 whereas net debt stood at Rs.61 Cr.

- Consolidated Borrowings were at Rs.123 Cr as of March 2022.

Investor Conference Call Highlights

- The management states that the Aristocrat brand portfolio has been growing faster than the peer companies in the same segment where the brand saw almost 61% YoY growth in Q4FY22 and 140% in FY22 & the brand contribution stood at 36% of the overall business.

- The company’s current quarter saw almost 40% of its annual advertising spending.

- The management states that its manufacturing has scaled up to almost two-thirds of its total sales.

- The management foresees good demand in the coming quarter due to domestic travel coming back to pre-pandemic levels, resumption of international travels, pandemic-free weeding seasons and school/college reopening.

- The management also foresees several headwinds in the form of high inflation & high contribution of the future group to the total sales (15% of pre-pandemic sales).

- The company took a 4% price increase in November and about the same towards the end of March and one in Q1FY22 while the RM inflation if FY22 stood at 6%.

- The management states that several units were at about 83% revival in FY22 compared to FY20.

- The management states that the CAPEX outlay for the current financial year FY23 will be between ₹30 to ₹35 Cr.

- The company’s current contribution from the Future Group stands close to zero.

- The company’s online sales contribution stood at 16% of total sales in FY22 while the management expects it to taper down to 12-15% levels in the coming years.

- The company’s Skybags division is going to launch a new range targeting the younger generation of women.

- The company’s share of modern trade in CSD was at 30%.

Analyst’s View:

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. Luggage sales in all segments are picking up with the value segment bouncing back the most. The management is also confident that there are no issues regarding the supply of raw materials. It remains to be seen how VIP continues to strengthen its internals in the meantime and develop the eCommerce channel along with headwinds in the form of inflation & future groups’ current financial health. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP Industries remain a pivotal mid-cap stock to watch out for.

Q3FY22 Update

Financial Results & Highlights

| Standalone Financials (In cr) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 386.9 | 229.97 | 68.2% | 324.9 | 19.1% | 913.59 | 371.9 | 145.7% |

| PBT | 37.01 | -9.44 | 492.1% | 29.14 | 27.0% | 70.88 | -96.61 | 173.4% |

| PAT | 27.55 | -8.68 | 417.4% | 23.63 | 16.6% | 54.66 | -72.64 | 175.2% |

| Consolidated Financials (In cr) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9mFY22 | 9mFY21 | YoY% | |

| Sales | 397.34 | 232.53 | 70.9% | 330.06 | 20.4% | 933.61 | 375.56 | 148.6% |

| PBT | 43.71 | -8.01 | 645.7% | 24.56 | 78.0% | 70.12 | -118.89 | 159.0% |

| PAT | 33.47 | -7 | 578.1% | 18.54 | 80.5% | 54.54 | -93.71 | 158.2% |

Detailed Results:

- Q3 was the highest revenue quarter in the last 8 quarters, including Q4FY20.

- Revenue growth was very good with a gain of 71% You and PAT was at Rs 33 Cr vs a loss of Rs 7 Cr last year.

- The revenue breakup of hard and soft luggage was at 61:39 while the revenue breakup for brands was:

- Carlton: 5%

- VIP: 22%

- Skybags: 32%

- Aristocrat: 41%

- Gross margin climbed up to 49% in Q3 with EBITDA margin at 16%. The gross margin was up mainly due to the product mix shifting towards VIP and Skybags.

- Borrowings were reduced to Rs 68 Cr while cash and investments were at Rs 141 Cr.

Investor Conference Call Highlights

- QoQ rise in sales was 20% which was much sharper than precovid QoQ rise in Q3 in the past.

- Many travel spots saw higher traffic than before the pandemic.

- VIP is seeing severe inflation in all raw materials and logistics. RM costs have risen 13% YoY.

- The company has been concentrating on improving internal operations and manufacturing and reducing dependence on external manufacturers.

- The company has also focused more on hard luggage in the recent past with global demand trends pointing to a greater demand for hard luggage due to hygiene issues.

- VIP has invested Rs 36 Cr in increasing capacity for hard luggage in both India and Bangladesh.

- VIP saw good pent up demand in all products particularly hard luggage.

- The management does not expect any demand uncertainty going forward.

- ASP has remained at similar levels as FY20.

- The management will stay cautious on pricing increase due to competitive intensity.

- The management stated that the company aims to keep gross margins above 50%.

- The company did a price hike of 4% in Nov.

- The sales contribution from Bangladesh in Q3 was at 45%.

- The management is expecting inhouse manufacturing to rise to 65-70% of total requirement vs FY20 which was at 40%. The share of Chinese outsourcing is less than 10% now.

- The inhouse manufacturing was at 58% in the 9M period.

- Q3 saw greater ad spend than previous quarters and it is expected to rise in the future according to the management.

- 60% of the VIP’s capacity is for hard luggage while 40% is for soft luggage. All of the hard luggage sold is made inhouse. All the soft luggage made by VIP is made in Bangladesh. The rest is outsourced to Indian manufacturers.

- The management expects VIP and Skybags to rise from current levels.

- The export business has seen good demand comeback in existing markets but the company does not have any plans for further expansion in exports currently.

- A&P will be brought to 5% of revenues in time according to the management.

- The management expects demand to rise in Q4 mainly due to the opening up of schools and institutions.

- Ecommerce channel has grown 23% over FY20 numbers while the modern trade channel has stayed flat and general trade is down 5% from those levels. CSD was down 17%.

- Polypropylene is much more cost effective vs polycarbonate for making hard luggage. All the new capex for VIP is also towards polypropylene based hard luggage.

Analyst’s View:

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company saw good momentum in overall performance. Sales were up for all segments with the revenue contribution being highest for Aristocrat. VIP is also looking to spend Rs 36 cr on developing a new line for making hard luggage based on polypropylene. It remains to be seen how VIP continues to strengthen its internals in the meantime and develop the eCommerce channel which was small for them so far, and what impact will the rising RM inflation have on the company’s bounce-back plans. Given the caution in travel and travel activities at the moment, sustained demand-revival seems a little away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remain a pivotal mid-cap stock to watch out for.

Q2FY22 Update

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 341 | 118 | 188.98% | 216 | 57.87% | 557 | 176 | 216.48% |

| PBT | 29 | -30 | 196.67% | 5 | 480.00% | 34 | -87 | 139.1% |

| PAT | 24 | -22 | 209.09% | 3 | 700.00% | 27 | -64 | 142.19% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 337 | 108 | 212.04% | 221 | 52.49% | 557 | 166 | 235.54% |

| PBT | 25 | -44 | 157% | 2 | 1150.00% | 26 | -111 | 123% |

| PAT | 19 | -35 | 154% | 3 | 533.33% | 21 | -87 | 124.14% |

Detailed Results:

- Q2 was the highest revenue quarter in the last 7 quarters, including Q4FY20.

- Hard luggage accounted for 47% of revenues.

- Gross Margin for VIP was 47%, compared to 51% in the sequential quarter. The 4% fall is due to inflation in raw material costs and ocean freight.

- EBITDA margin was at 14% in Q2 vs 12% last quarter.

- The company has consolidated cash & cash equivalents of Rs 106 Cr as of 30th September 2021.

- Consolidated Borrowings were at Rs 71 Cr as of 30th September 2021.

Investor Conference Call Highlights

- Although the damage to the economy and the travel industry has been severe from the 2nd wave of COVID, the bounce-back has been sharper than last year.

- The business witnessed an impressive 80% recovery, measured against the base FY20 numbers. Air passenger traffic saw a 60% recovery, compared to Q2FY20.

- The company continued to suffer due to restrictions on international travel and the closure of schools and colleges.

- Although demand has opened, the company faced 2 key challenges:

- High raw material costs and ocean freight

- Supply chain constraints in Bangladesh till mid-August

- The company witnessed significant upscale across all its revenue channels: Ecommerce, general trade, and modern trade. However, the retail channel and institutional business were below optimum levels.

- The company is expanding its Bangladesh factory plant and increasing capacities there through an investment of Rs. 15 to 20 Cr.

- The company also has plans to invest in its India supply chain through the expansion of manufacturing capacities.

- The company plans to aggressively invest beyond creating demand and generating preference through not only promotions and advertising but also through the launch of new products.

- The management reiterated its aspiration for a sustainable 20% EBITDA margin but also highlighted the uncertainty posed due to inflationary pressures on raw materials.

- Receivables have gone up from Rs. 148 Cr to Rs. 256 Cr primarily due to upscale. On a day-wise count, receivables have come down by 6 days.

- In the backpacks category, the company has witnessed some throughput happening due to the partial opening of schools and colleges.

- The management reassured that they have enough avenues of sourcing suppliers for the expected growth in demand going forward, be it from India or the S1 supply chain of China.

- While the company is witnessing continuous growth in demand in the value segment, demand on the mass premium and premium segments are also coming back. However, the recovery rate in the value segment is higher than that in the mass premium and premium segments.

- In the medium to long term, the company has plans of growing its distribution through the general trade channel at a fast pace, both in towns covered so far and smaller towns to increase distribution.

- In the subsequent 2 quarters, the company has plans to aggressively take back its total number of retail stores for exclusive business outlets close to 2019 levels. In FY23, it plans to expand beyond the 2019 number of outlets. Out of the total 500 retail stores, management plans to reopen 460 of these stores by end of FY22.

- Going forward, the company plans to resort to a franchise model for its exclusive business outlets. The retail operations would be run by a partner who’s more suitable to do it and the company would focus on running the business of branding and creating demand.

- The management iterated its ambition to achieve close to 50% gross margins in Q3 and Q4 of FY22.

- The company has launched new products in the luggage segment. The management mentioned they had some previous inventories of backpacks, clearing which they plan to launch a new range of products in this category in FY23.

- The company saved Rs. 180 crores in the COVID year, 50% of which was sustainable, and the remaining 50% will come back as the business is back on track.

- The company will always prioritize the domestic side of the business before looking for export opportunities according to the management.

- The company’s Caprese focus is highest on e-commerce and it would like to go further deeper into the eCommerce business with Caprese before taking it across other channels.

- For the supply chain on the raw material side where the company is heavily dependent on China, they have witnessed significant challenges. As a response to the same, they got raw materials ahead of time to secure supply. Simultaneously, they are looking at alternate vendors in India and Bangladesh to accelerate the processes.

- Hard luggage sales constituted 47% of the total revenue in Q2.

Analyst’s View:

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company saw its best quarter since the start of FY21. Luggage sales in all segments are picking up with the value segment bouncing back the most. The management has stated that the company will be looking to expand aggressively in the GT channel and will reopen its stores and bring the number of stores back to 2019 levels. The management is also confident that there are no issues regarding the supply of raw materials. It remains to be seen how VIP continues to strengthen its internals in the meantime and develop the eCommerce channel which was small for them so far, and what impact will a possible 3rd wave of COVID-19 have on the company’s bounce-back plans. Given the caution in travel and travel activities at the moment, sustained demand-revival seems a little away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remain a pivotal mid-cap stock to watch out for.

Q1FY22 Update

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 218 | 59 | 269.49% | 258 | -15.50% |

| PBT | 5 | -57 | 108.77% | -16 | 131.25% |

| PAT | 3 | -42 | 107.14% | -12 | 125.00% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 221 | 58 | 281.03% | 259 | -14.67% |

| PBT | 2 | -67 | 103% | -6 | 133.33% |

| PAT | 3* | -51 | 106% | -4 | 175.00% |

*Includes Rs 87 Lac of deferred tax credit

Detailed Results:

- The results for the quarter were up YoY in standalone and consolidated revenues due to the low base in Q1FY21.

- The profits for the quarter were back in positive territory in both standalone & consolidated terms after a full year of losses.

- Gross Margin for VIP was 54%. It was mainly due to lower discounts and better product mmix with high margin products rise.

- EBITDA margin was at 12% in Q1 vs 8% last quarter.

- The company has cash & cash equivalents of Rs 196 Cr as of 30th June 2021.

- Net borrowings were at Rs 154 Cr as of 30th June 2021.

- Net debt was at 0.

Investor Conference Call Highlights

- Although the damage to the economy and the travel industry has been severe from the 2nd wave of COVID, the bounce-back has been sharper than last year.

- The management states that the company is working on improving its supply chain and focus on digital marketing and other demand-generating initiatives.

- Although physical sales were hampered due to localized lockdowns, overall sales were not as damaged as in Q1FY21 due to general trade working moderately and e-commerce playing a bigger role in overall sales as compared to a year ago.

- The company is seeing good demand in the mass market segment and thus it is looking to launch new products in the value range. These products will be sold via the eCommerce channel primarily. Around 1/3rd of the 20-25 new launches planned currently are from the value segment.

- The company will also launch in the mass premium and premium ranges slowly as demand for these segments comes back especially with the normalization of weddings, leisure, and international travel.

- There has been a lesser contribution from the liquidation of low-cost inventory in Q1 vs Q4FY21.

- The company has reduced discounts to mitigate the rise in commodity prices. The major difference in numbers from the Bangladesh operations has started to reflect from Q1 onwards according to the management.

- The company does have some exposure to the Future Retail Group but it has made a provision of Rs 3 Cr for it in Q1.

- Almost 90% of total sales come from VIP’s production from Nasik and Bangladesh.

- Hard luggage has seen better demand than soft luggage in the past few quarters.

- The management has stated that it is too early to draw reliable conclusions for the backpack segment which is very dependent on educational institutions.

- The management has stated that it will be looking to explore opportunities in the export ODM space only after it has managed to do all that it wants with the domestic business.

- Around 50% of the cost savings in FY21 should be retained in FY22 according to the management.

- The management asserts that the major driver behind gross margin expansion is the rise of the in-house share of manufacturing. The management maintains that VIP can improve upon historical margins due to improving operational efficiencies, reduced costs, and margin expansion due to a high share of own manufacturing.

- The cost inflation from raw material prices and ocean freight costs are now fully reflected in selling prices according to the management.

- The quarter was good for the Caprese brand. The focus for this brand is now to manufacture from Bangladesh and to expand in the e-commerce channel. The company will also be looking to launch more mass products under this brand by leveraging on the cost advantage of making in Bangladesh.

- The management expects an improvement in working capital days of 30-40 days from historical levels once everything gets normalized.

- The management has indicated that the shift from the unorganized to the organized sector in the luggage industry may be accelerated as the industry recovers.

- The strategy ahead for VIP will be to maximize in-house production and only import specialized products from China that it cannot make by itself.

- The company will always prioritize the domestic side of the business before looking for export opportunities according to the management.

Analyst’s View:

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company has seen a decent performance in Q1 and has managed to achieve margin expansion despite the loss in sales from the 2nd wave of COVID-19. This margin expansion was mainly on the back of the rising share of in-house production to almost 90% of total product sales. The management maintains that the development of the domestic business remains the primary concern of VIP and it will only look at export opportunities after it has normalized the domestic business. The company is also looking to introduce new mass market products for its brands given that this segment has seen greater demand than the others in recent quarters. It remains to be seen how VIP continues to strengthen its internals in the meantime and develop the ecommerce channel which was small for them so far. Given the caution in travel and travel activities at the moment and the impending 3rd wave of COVID-19, sustained demand-revival seems a little away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remains a pivotal mid-cap stock to watch out for.

Q4FY21Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 258 | 316 | -18.35% | 239 | 7.95% | 673 | 1734 | -61.19% |

| PBT | -16 | -6 | -166.67% | -9 | -77.78% | -113 | 121 | -193.4% |

| PAT | -12 | -6 | -100.00% | -9 | -33.33% | -85 | 89 | -195.51% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 259 | 316 | -18.04% | 242 | 7.02% | 667 | 1727 | -61.38% |

| PBT | -6 | 10 | -160% | -8 | 25.00% | -125 | 148 | -184% |

| PAT | -4 | 10 | -140% | -7 | 42.86% | -97 | 112 | -186.61% |

Detailed Results

- The results for the quarter were down YoY with 18% YoY decline in standalone and consolidated revenues.

- The profits for the quarter were in negative territory in both standalone & consolidated terms.

- The company saw good performance on QoQ basis in consolidated terms.

- Gross Margin for VIP after netting of other income was 47%. It was mainly due to higher discounts and liquidation of old stocks.

- EBITDA margin was at 8% vs 8% last year.

- Overall Expenses were down by 29% YoY in Q4 & 52% YoY in FY21. Employee cost was lower by 8% YoY & Other expenses were lower by 38% YoY.

- The company has cash & cash equivalents of Rs 231 Cr as of 31st Mar 2021.

- Net borrowings were at Rs 154 Cr as of 31st Mar 2021.

- Net debt was at 0.

Investor Conference Call Highlights

- The polycarbonate ABS prices were almost 2.3x to 2.5x of pre-COVID level.

- The management expects to sustain cost reductions of Rs 80-90 Cr at the annualized level.

- The post-pandemic impact on consumer behaviour has been mainly focused on safety and security with demand for hard luggage greater than that for soft luggage.

- The management has stated that margins will be dependent on the demand situation and how it comes back to pre-covid levels.

- The management expects that this time the turnaround will be faster than the last downtime.

- The management has stated that it doesn’t expect any more cuts in employee strength going forward.

- The company has not been affected by the disruption in Indo-China trade as most of the RM from China is being used in Bangladesh.

- The management assured that the reason for VIP’s gross margins being less than other listed peers is mainly on accounts of ongoing discounts and it shall come back to original levels as these discounts go away.

- VIP has done 2 price increases in March and April in selective products due to the rise in import prices.

- The company did Rs 171 Cr of cost savings in FY21 and the management states that around 50% of this savings should carry forward in normal times.

- The management is confident of delivering normal sales for Rs 600-700 Cr in normalcy despite the reduction in stores and employees.

- The value portfolio has seen a greater contribution in FY21 vs FY20. This was mainly due to pushing on the e-commerce channel and the low sales of other big brands like Skybags.

- The management is confident of getting back lost market share and it will be pursuing it once normalcy returns to get it back to previous levels.

- The E-commerce channel is showing good traction in tier 2 and 3 cities for VIP.

- Other than the rise of the e-commerce channel, the management expects all other channels for the industry to stay at normal levels once the industry revives.

- The short-term loans taken in FY21 will be repaid in July & Sep.

- The management is confident that the Bangladesh plant is technically capable enough to make all the products that were being imported from China.

- The management expects FY22 to be muted as well given that most of the Q1 (its best season) was under local lockdowns. Thus, it expects the recovery to growth by FY23 at the least.

- In FY21, 17% of sales were from the ecommerce channel. The rise of this channel has also resulted in the rise of the value segment in the product mix as mostly low-priced products are sold here for the entire industry.

- Q1 was much better than expected according to the management. This was mainly due to the stocking of enough inventory in both RM and finished goods. VIP is also looking at revamping its whole supply chain structure & inventory optimization.

- The major focus for VIP remains the recovery of domestic business. It is indeed on the lookout for export opportunities but will not be aggressively pursuing them. The Middle East is the biggest market for VIP after India.

- The company is planning capex of Rs 10-20 Cr for enhancing capacity in H2.

Analyst’s View

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company continued to see good sequential recovery in Q4 but Q1 was again hit hard with the 2nd wave of COVID-19. As per the management, it will take at least FY23 for the company and industry to come back to normalization. It remains to be seen how VIP continues to strengthen its internals in the meantime and develop the ecommerce channel which was small for them so far. Given the slowdown in travel and travel activities at the moment, demand-revival seems a distance away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remains a pivotal mid-cap stock to watch out for.

Q3FY21Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 240 | 432 | -44.44% | 116 | 106.90% | 415 | 1423 | -70.84% |

| PBT | -9 | 34 | -126.47% | -30 | 70.00% | -97 | 127 | -176.38% |

| PAT | -9 | 27 | -133.33% | -22 | 59.09% | -73 | 94 | -177.66% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 243 | 432 | -43.75% | 108 | 125.00% | 408 | 1414 | -71.15% |

| PBT | -8 | 43 | -119% | -44 | 81.82% | -119 | 138 | -186.23% |

| PAT | -7 | 34 | -121% | -35 | 80.00% | -94 | 102 | -192.16% |

Detailed Results

- The results for the quarter were down YoY with 44% YoY decline in standalone and consolidated revenues.

- The profits for the quarter were in negative territory in both standalone & consolidated terms.

- The company saw good performance on QoQ basis in both standalone and consolidated terms.

- Gross Margin for VIP after netting of other income was 41%. It was mainly due to higher discounts and a high mix of India produced goods sales rather than Bangladesh production.

- EBITDA margin was at 8% vs 16% last year.

- Overall Expenses were down by 49% YoY. Employee cost was lower by 46% YoY & Other expenses were lower by 51% YoY.

- The company has cash & cash equivalents of Rs 219 Cr as of 31st Dec 2020.

- Net borrowings were at Rs 148 Cr as of 31st Dec 2020.

- Net debt was at 0.

Investor Conference Call Highlights

- The company has appointed Mr. Anindya Dutta as Managing Director as of 1st Feb 2021.

- As mentioned above, gross margins have remained flat QoQ due to continued discounts. The management expects EBITDA margins to fully reflect production from Bangladesh entirely by FY23.

- The major comeback in demand is mainly due to air travel slowly coming back to normal. The demand will have boosted additionally in Q1 next year when wedding season comes back.

- Overall inventory is in the range of INR 300 Cr. Old inventory is expected to be cleared soon and production from both Nashik and Bangladesh plants is expected to hit markets in Q1.

- The management has stated that fixed costs will remain at current levels of Rs 25 Cr per quarter for the near future.

- The company has stopped importing finished goods from China and is only dependent on raw materials from there.

- The management has stated that the new MD’s experience in international markets should prove vital in the company’s quest to revive and expand its export presence.

- The company has a lot of inventory in backpacks and it should be able to meet any upswing in demand once all educational institutions in India open up.

- The gross margins are expected to rise slowly as competitive intensity will be there in the industry as everyone is sitting on a lot of inventory.

- The management has stated that VIP has had cost savings of Rs 180 Cr in the year so far. Around 50% of this will come back in time while 50% is permanent saving.

- The general trade channel is still going slow while all others are in line now with last year.

- Ecommerce is doing well for VIP with more than 20% revenue contribution. But this is expected to drop once the general trade channel gets back to normal.

- There will a lead time of 3-6 months for increasing capacity at the Bangladesh plant. It will be small enough to be able to be funded by internal funds.

- The bulk segment in backpacks is schools.

- The company has seen collections on its receivables from all vendors except Big Bazaar. The amount outstanding from Big Bazaar is Rs 35 Cr. VIP has started receiving some amounts from it from Jan onwards.

- RM prices have gone up in the last 9M period and are expected to come down going forward.

- The cost of the product from Bangladesh is 15% less than from China.

- The management has stated that although corporate travel is expected to go down a lot due to rise of work from home culture, the corporate gifting demand should remain intact.

- The long term borrowings are expected to mature in July and August and are expected to be paid in full.

- The company has not added any new dealers in FY21.

- The payment to the Bangladesh plant is made in dollars and thus there is some amount of forex risk here.

- The company should be back to a quarterly revenue rate of Rs 400 Cr in Q1FY22 if recovery momentum does not weaken.

Analyst’s View

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company saw good sequential recovery in Q3 and is expecting to get back to its quarterly run rate of Rs 400 Cr by Q1FY22. As per the management, the competitive scenario at the moment remains very intense as all industry players are sitting on a lot of stock and gross margins may take at least 1-1.5 years to come back to pre-covid levels. It remains to be seen how fast demand comes back to the sector and how will the company fare in the meantime. Given the slowdown in travel and travel activities at the moment, demand-revival seems a distance away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remains a pivotal mid-cap stock to watch out for.

Q2FY21Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 118 | 414 | -71.50% | 58 | 103.45% | 176 | 991 | -82.24% |

| PBT | -30 | 36 | -183.33% | -57 | 47.37% | -87 | 92 | -194.57% |

| PAT | -22 | 30 | -173.33% | -42 | 47.62% | -64 | 68 | -194.12% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 108 | 415 | -73.98% | 58 | 86.21% | 166 | 982 | -83.10% |

| PBT | -44 | 41 | -207.32% | -67 | 34.33% | -111 | 95 | -216.84% |

| PAT | -35 | 33 | -206.06% | -51 | 31.37% | -87 | 68 | -227.94% |

Detailed Results

- The results for the quarter were dismal with 72% & 74% YoY decline in standalone and consolidated revenues respectively.

- The profits for the quarter were in negative territory in both standalone & consolidated terms.

- The company saw good performance on QoQ basis in both standalone and consolidated terms.

- Gross Margin for VIP after netting of other income was 42%. It was mainly due to higher discounts and a high mix of India produced goods sales rather than Bangladesh production.

- Overall Expenses were down by 41% YoY. Employee cost was lower by 49% YoY & Other expenses were lower by 66% YoY.

- The company has cash & cash equivalents of Rs 206 Cr as of 30th Sep 2020.

- Net borrowings have risen to Rs 204 Cr from Rs 77 Cr last year.

- Net debt however was near 0 vs Rs 60 Cr last year.

Investor Conference Call Highlights

- Bangladesh operations started only with producing masks. The company is now also doing a tailoring operation in soft luggage in Bangladesh.

- VIP is selling Rs 2-3 Cr worth of masks per month now.

- The management expects the company to come back to pre-covid levels in at least 1-1.5 years. The industry should take 2-3 years to normalize.

- Bangladesh operations are key going forward. Right now only 50% of Bangladesh’s capacity is enough for domestic sales. The company is looking to start international sales from this location to reduce dependence on the domestic market.

- Ecommerce sales have come up a lot since COVID-19 and have grown 40% YoY. This channel used to account for 7-10% of sales and now it counts for 27% of total sales for the company.

- The company will be pursuing both the online market site sales from Flipkart & Amazon and its own direct to customer sales from the e-commerce mechanism.

- In the long run, this channel should account for 20-25% of sales.

- Although gross margins for e-commerce sales are expected to be lower than in-store sales, the company will specifically be looking to make products suited for the channel so that the overall margin profile is not affected too much.

- Since all companies in the industry have high inventory levels, discounting has been greater than before in order to liquidate the stock that they have built up. This has led to a fall in average selling price. This is true for VIP as well.

- The major cost initiatives for VIP have happened on the manpower and fixed EVO operations.

- The recovery for the industry will be dependent on the type of recovery model that India will follow. If it follows the Western model of repeated small lockdowns, then recovery will be slower than when compared to the Asian model of recovery.

- The mask business should provide revenues of Rs 18 Cr given the current run rate. The company is still looking to enter into other new segments but is not in any rush to do so and will do it in their own time.

- The company is also looking to replace the imported handbags which they get from China with its own manufactured products from Bangladesh. This should provide a good boost to the handbag market.

- The company will be able to get a better picture of the processing of the pending insurance claim of Rs 48 Cr in Q3.

- The fixed cost saving for the year is estimated to be at Rs 180 Cr. Around 50% of this is expected to be sustainable.

- The business demand from travel and wedding is almost at 50-50. The company expects the resurgence from wedding demand to come back next summer.

- The company has a leading market share from weddings in Northern and Eastern India both through the flagship VIP and Aristocrat brands.

- The company is also looking to set up its own manufacturing facility for soft luggage in Eastern India to reduce dependence on external vendors for soft luggage.

- The management had stated that the company will be looking to sell lower-end products on e-commerce because the majority of the business in the channel is volume-driven at the lower end. The company can gain a big market share here as the unorganized sector cannot provide the volumes required for the channel.

- Backpacks are still the fastest-growing segment for the company but its growth has slowed down as demand was driven primarily by schools and colleges. The volumes & growth for the category will all depend on how the schools open and how offices open. This category is also driven mainly in the lower end and through e-commerce sales. The company is best positioned to compete in this category due to its Bangladesh facility which has low labour cost.

- The company has closed 100 out of its 250 exclusive branded outlets. Currently, 70-75% of its stores are open.

- The company sold off the Haridwar plant as it could make the same products in its Nashik facility. The company had started running it as it was getting a tax break from it which expired in 2012 and now there isn’t much of a margin differential between this plant and Nashik plant.

- The company is only selling the land plot and building in Haridwar and it is shifting all of the machinery to the Nashik location. The company is looking to make around Rs 12 Cr of profit from the Sale of Rs 20-25 Cr.

- The basic strategy of VIP in international sales will be to sell on price leveraging the very low-cost manufacturing operations in Bangladesh.

Analyst’s View

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company is doing well to switch to Bangladesh for soft luggage procurement and is looking to enter into international operations by leveraging its low-cost manufacturing operations in Bangladesh. It has also seen good demand from the mask category and is looking to enter other adjacent segments. As per the management, the demand scenario at the moment is very uncertain and it will take at least 1-1.5 years to come back to pre-covid levels. It remains to be seen how fast demand comes back to the sector and how will the company fare in the meantime. Given the slowdown in travel and travel activities at the moment, demand-revival seems a distance away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remains a pivotal mid-cap stock to watch out for.

Q1FY21Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 59 | 577 | -89.77% | 317 | -81.39% |

| PBT | -57 | 56* | -201.79% | -6 | -850.00% |

| PAT | -42 | 38 | -210.53% | -5 | -740.00% |

| Consolidated Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 58 | 567 | -89.77% | 317 | -81.70% |

| PBT | -67 | 55* | -221.82% | 10 | -770.00% |

| PAT | -51 | 35 | -245.71% | 10 | -610.00% |

*Contains an exceptional item of loss of Rs 48.5 Cr

Detailed Results

- The results for the quarter were dismal with a 90% YoY decline in standalone and consolidated revenues respectively.

- The profits for the quarter grew into negative territory in both standalone & consolidated terms.

- The company achieved a reduction in Fixed Overheads by 35%.

- Gross Margin for VIP after netting of other income was 42%. It was mainly due to higher discounts and a high mix of India produced goods sales rather than Bangladesh production.

- Overall Expenses were down from Rs 160 Cr in Q1FY20 to Rs 75 Cr in Q1FY21.

- The company has a cash balance of Rs 159 Cr as of 30th June 2020.

- The company is looking to leverage its manufacturing capability to enter into the PPE category and is starting to make face masks.

Investor Conference Call Highlights

- The company has plans to borrow Rs 300 Cr to tide through the current tough times.

- The management stresses that the issue that the company is facing is not on the supply side but that of demand. the travel sector has been the worst hit from the pandemic and being a travel-oriented product the demand for the company’s products has dried up drastically.

- The management has refrained from providing any specific guidance for FY21.

- The PPE business is still very small and the management has stated that the company can make only Rs 5-10 Cr in FY21 on this segment.

- Even if the company pays all of its creditors immediately, it has enough cash to survive on zero revenues for 6 months.

- The management has stated that they do not have any high expectations for performance revival in Q2. The revival will solely be dependent on the developments of the virus going forward.

- The management has stated that entry into masks is short term only as everyone is getting into this space and there are very low entry barriers in place.

- The management is looking to increase the manufacturing of ladies’ handbags. At the moment most of this category is being imported. Once manufacturing starts for it either in India or Bangladesh, the company can earn much higher margins on this product.

- The employee expenses look flat QoQ mainly as Q4 also saw a reversal of the Director’s commission and performance pay for all the employees. Overall employee expenses have fallen 35% YoY.

- The company saw other income of Rs 18 Cr in Q1. Around Rs 14 Cr was from rent waivers, reductions, and closure of shops. Around Rs 2 Cr was from insurance claims and Rs 2.5 Cr was from one time recurring balance.

- The stock inventory levels have not changed much as there were no meaningful sales for the company. The company is looking at secondary sales right now and has offered some distributor & dealer schemes in June and July to try and move the pipeline inventory.

- The company has cut around 100 of its 250 exclusive retail stores as a part of its cost-cutting initiative.

- The management asserts that the company is well equipped to cater to increasing demand. It can easily set up new facilities within 4-6 months to increase the capacity to address demand. And almost all of the RM demand from China can now be addressed from Bangladesh going forward.

- Around 40-50% of sales are from the CSD channel. This channel was working at 50% capacity in Q1 and was the most earning channel for the company.

- The management has stated that the company will not be losing major revenue share as the closed 100 stores had accounted for only 10% of revenues last year.

- Currently, 35% to 40% of the stock for VIP is from Bangladesh.

- The management has stated that the pandemic has forced them to focus on cash management vs P&L and on cost savings due to the blow to the industry demand.

- The fastest-growing channel for the company remains e-commerce and the pandemic has further increased the significance of this channel. The company is now balancing its exposure among prominent e-commerce sellers like Amazon and Flipkart.

- The management has stated that demand for the luggage industry should mirror domestic air traffic and increasing footfalls in shopping centres and malls.

Analyst’s View

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. However, the company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company is doing well to switch to Bangladesh for soft luggage procurement and to reduce costs while acknowledging that the sales environment going forward will be tough in the short term. It has also ventured into PPE making and is focusing on increasing its ladies’ handbags lines. As per the management, the demand scenario at the moment is very uncertain. It remains to be seen how fast demand comes back to the sector and how will the company fare in the meantime. Given the slowdown in travel and travel activities at the moment, demand-revival seems a distance away. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remains a pivotal mid-cap stock to watch out for.

Q4FY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 316.53 | 436.75 | -27.53% | 431.81 | -26.70% | 1738 | 1793.96 | -3.12% |

| PBT | -5.55 | 28.8 | -119.27% | 34.31 | -116.18% | 121.12* | 196.6 | -38.39% |

| PAT | -5.56 | 18.36 | -130.28% | 26.55 | -120.94% | 88.73 | 128.81 | -31.12% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 316.84 | 436.95 | -27.49% | 432.25 | -26.70% | 1730.82 | 1792.98 | -3.47% |

| PBT | 10.45 | 36.19 | -71.12% | 42.5 | -75.41% | 148.41* | 214.94 | -30.95% |

| PAT | 9.52 | 25.28 | -62.34% | 34.21 | -72.17% | 111.73 | 145.27 | -23.09% |

*Contains an exceptional item of loss of Rs 48.5 Cr

Detailed Results

- The results for the quarter were dismal with a 27.5% YoY decline in standalone and consolidated revenues respectively.

- The profits for the quarter grew into negative territory in standalone terms.

- FY20 revenues were modest with a 3% YoY decline while profits fell a lot more at 31% YoY and 23% YoY in standalone and consolidated terms.

- Gross margins improved in Q4 to 58% from 48% a year ago. This was mainly due to higher procurement from Bangladesh, improvement in Hard Luggage share, and reduction in RM costs.

- COVID-19 impact in Q4 was revenue loss of Rs 126 Cr and profit loss of Rs 26 Cr.

- In FY20, the company continued to improve EBITDA margins and saw it come to 18% vs 13% in FY19.

- ROCE also improved in Q4 at 25% vs 22% a year ago.

- The company had given out a dividend of Rs 3.2 per share in Feb.

Investor Conference Call Highlights

- Despite the revenue loss in Q4 and Q1FY21, the company continues to remain resilient with enough liquidity in the books to tide over the current times.

- The company stands in a good position to rise again once the industry revives as it is the best place in the industry to reduce dependence on China and also has a fully functional alternative in the Bangladesh facility.

- The management is confident that for the current year, 100% of the company’s procurement can come from Bangladesh as they already have enough stocks.

- Since the majority of the company’s sales are from the top 8 cities in India, it will indeed take time for revenues to recover as all of these are still in red zones.

- The management admits that Q1 is going to be a washout for the company and it will depend on the rest of the year on how things will pan out.

- The management expects travel patterns to become shorter and more localized with more land travel and less air travel. It also expects business travel to go down going forward as working remotely becomes more acceptable.

- The target for the company this year is to achieving breakeven in the year despite the expected decline in revenue.

- The company saw sales of only Rs 32 Cr in March.

- The borrowings have been reduced to Rs 32 Cr from Rs 86 Cr in March last year.

- The management has clarified that the company does not face any labour shortage in any of its plants and the only variables here is supply chain and consumer demand.

- The company has more than adequate inventory with it as it had stocked up for April & May which are the bestselling months for the company. Since no sales took place in these 2 months, the company has enough stocks for the coming times until the company can get a handle on the situation.

- The company has already instituted an almost 30% reduction in costs (excluding ad spending) including a reduction in salesforce, reducing rent, and has even foregone advertisements till now.

- The management has stated that despite zero sales in April and May, there were some collections in these months and the company will not be able to provide financing help to its distributors.

- The company has already taken aside some provisions to cover and mitigate the credit risk from distributors. It is around 8-8.5 Cr.

- The management expects market share gain in the year to happen at the expense of other branded players instead of unbranded space.

- The total inventory of the company is at Rs 451 Cr in Q4 which is based on costs and should yield a higher amount on sales.

- Modern trade should have the least amount of inventory. On average all channels have around 60 days of inventory.

- The company had tripled capacity in Bangladesh and it could cover 55% of the company’s normal annual requirements.

- 90% of raw materials in the Bangladesh plant comes from China and there are no supply disruptions here.

- The management states that it would like that all of the procurement for the company comes from Bangladesh but there are still some particular product requirements that are currently only available from China and the company shall work to develop these as well in Bangladesh.

- The management expects the demand from weddings to come back in Q3 after monsoons are over.

- The claim for the warehouse from Q1 last year should be done in FY21.

- The company has already applied for the rent waiver in more than 60% of its stores for the lockdown. The company has not gotten any confirmation on this from their mall stores.

- The management does not expect any danger of inventory pileup as it will start manufacturing once orders come in after channel inventory gets cleared.

- In India, 50% of the workforce is contractual.

- The mix between soft and hard luggage has been the same at 70-30. Backpack season is expected to come back once schools and educational institutions start in a few months.

- The market share in general trade is larger than in modern trade.

- The management does not expect to make any CAPEX in the Bangladesh plant to expand capacity as the current capacity is expected to be sufficient to cover the company’s expected sales volumes in FY21.

- Another goal for the company is to achieve market leadership in the e-commerce channel.

- The new margins are sustainable in a normalized situation without any price wars.

- The company has 250 company-owned stores, all of which the company rents, and the company is expected to close 50-100 of these stores.

- Around 5-15% of industry sales are from e-commerce. The management expects this number to rise to 30% in the next few years.

Analyst’s View

VIP has been the market leader in the soft and hard luggage segment in India for a long time now. The company is one of the biggest luggage manufacturers in the world by volume. The company and the industry have been facing tough times with sales contraction due to a fall in demand and disruption from COVID-19. The company is doing well to switch to Bangladesh for soft luggage procurement and to reduce costs while acknowledging that the sales environment going forward will be tough in the short term. It remains to be seen how fast demand comes back to the sector and how will the fast-rising segment of backpacks will fare in the coming months. Nonetheless, given the company’s strong brand image and leadership position in the industry along with the resilient balance sheet of the company, VIP industries remains a pivotal mid-cap stock to watch out for.

Q3 2020 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY20 | Q3FY19 | YoY % | Q2FY20 | QoQ % | 9MFY20 | 9MFY19 | YoY% | |

| Sales | 433.94 | 432.69 | 0.29% | 414.15 | 4.78% | 1424.76 | 1357.58 | 4.95% |

| PBT | 34.31 | 30.56 | 12.27% | 36.07 | -4.88% | 126.67* | 167.8 | -24.51% |

| PAT | 26.55 | 19.56 | 35.74% | 30.21 | -12.12% | 94.29 | 110.45 | -14.63% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY20 | Q3FY19 | YoY % | Q2FY20 | QoQ % | 9MFY20 | 9MFY19 | YoY% | |

| Sales | 434.12 | 432.83 | 0.30% | 414.9 | 4.63% | 1415.76 | 1356.09 | 4.40% |

| PBT | 42.5 | 35.42 | 19.99% | 40.78 | 4.22% | 137.96* | 178.75 | -22.82% |