About the Company

Varun Beverages Ltd (VBL) is the second-largest franchisee in the world (outside the US) of carbonated soft drinks (“CSDs”) and non-carbonated beverages (“NCBs”) sold under trademarks owned by PepsiCo and a key player in the beverage industry. They produce and distribute a wide range of CSDs, as well as a large selection of NCBs, including packaged drinking water. PepsiCo CSD brands sold include Pepsi, Diet Pepsi, Seven-Up, Mirinda Orange, Mirinda Lemon, Mountain Dew, Seven-Up Nimbooz Masala Soda, Evervess Soda, Sting, and Gatorade. PepsiCo NCB brands sold by the company include Tropicana (100%, Essentials & Delight), Tropicana Slice, Tropicana Frutz, Seven-Up Nimbooz, and Quaker Oat Milk as well as packaged drinking water under the brand Aquafina.

Q1 CY23 Updates

Financial Results & Highlights

Detailed Results:

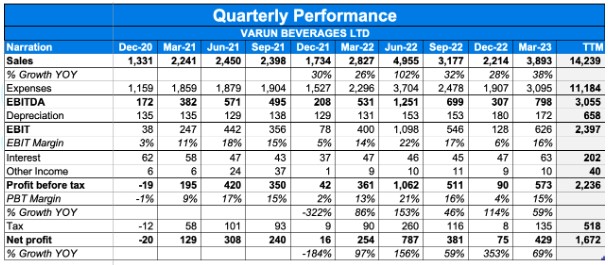

- The consolidated revenues for the current quarter increased by 37.7% YoY whereas PAT increased by 61.8% YoY.

- The company saw an EBITDA rise of 50.3% YoY and a volume rise of 24.7% YoY in the quarter.

- Net realization increased by 10.4% to Rs. 173.7 primarily due to price hike in selected SKUs taken towards the end of base quarter last year and continued improvement in mix of smaller SKUs (250ml).

- Sting is now 9.6% of total sales volumes in India.

- Depreciation increased by 31% in Q1 on account of the capitalization of assets and Finance costs increased by 33% in Q1.

- CSD constituted 71.2%, Juice 7.4%, and Packaged Drinking water 21.4% of total sales volumes in Q1 CY23.

- Gross margins improved by 89 bps to 52.4% from 51.5% in Q1CY2023 primarily driven by marginal savings in raw material prices and improved product mix.

- EBITDA increased by 50.3% to Rs. 7,980 mn and EBITDA margins improved by 172 bps to 20.5% in Q1 CY2023.

- Net debt stood at Rs. 4000 as on Mar 31, 2023, as against Rs. 3409 Cr as on Dec 31, 2022. Net debt increased on account of Greenfield expansion in Rajasthan and Madhya Pradesh and brownfield expansion at 6 plants for CY 2023 in India. Debt/Equity stood at 0.64.

- The Board of Directors recommended a final dividend of Rs. 1.00 per equity share. With this, the total dividend declared for the year ended 31st December 2022 stands at Rs. 3.50 per equity share.

- The Board recommended the split of existing equity shares of the Company from one equity share having face value of 10 each into two equity shares having face value of five rupees each which is subject to the approval of equity shareholders of the company.

- The company has commissioned a new production facility at Kota, Rajasthan, as well as expanded its capacity through brownfield expansion at six existing locations.

- In accordance to the company’s international growth plans, construction of a new production facility at DRC has already started, which is expected to be operational before the year end.

Investor Conference Call Highlights:

- The company commissioned a Greenfield Production Facility at District Bundi, Rajasthan and completed brownfield expansion in six facilities. A additional Greenfield plant in Jabalpur, MP is expected to be operational very soon.

- Sting has achieved a significant share in the overall mix and helped to establish the company as a leader in the category. Thus, the boards focus now turns toward new performance like value-added dairy, sports drink, juice segments to sustain the growth momentum.

- Sales volume has grown at a CAGR of 24% in five years, which is a testament of company’s execution capabilities. Net revenue increased significantly at a 26.7% CAGR over a period of five years.

- The company has production constraints for Tropicana and value-added dairy for which it is going to put up two plants in Maharashtra and UP in the coming year. The company is also doing a national roll-out for domestic dairy.

- The management believes that Campa and Reliance will be a formidable competition, yet as the market is very large, there will be room for everybody.

- The company usually locks-in inventory enough for six months for a season, which is why the inventory levels gave gone very high this quarter.

- The capex guidance for the year remains same at INR 1500 Cr, which has been majorly spent.

- Over 90% of the company’s transactions have moved to the dollar in Zimbabwe, which is going to result in positive currency risk from the current quarter.

- The management is confident on the outlook for Sports Drink and expect Gatorade to have a good momentum once the focus shifts towards it.

- The company is yet to finalize the debt plan for the upcoming year as it is planning to put up another plant in Orissa.

- Out of the 70,000-80,000 visi-coolers to be added, most have been added before the season.

- Earlier Gatorade was only available in 500 ml for Rs. 50, while now 200 ml for Rs. 20 has also been added.

- Sting is doing extremely well for the company due to the 400,000 distributors which were secured.

- Growth in rural for the company has bounced-back, thus rural growth is slightly ahead of urban growth.

- The ROCE for the company has been growing 200-250 basis points to 30%, the management gives a guidance of 100-225 basis points growth every year over the next few years.

- The management states that dairy, juices and sports drink command similar margins as the base category if not better.

- The management states that there has not been much volatility in sugar or in PET bottles, which are expected to stay in the similar range for the coming quarter.

- The snacks contract manufacturing for Pepsico being done by the company has already witnessed complete utilization of the plant.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher preform prices. The company is witnessing a strong performance in its Southern & western territories coupled with explosive growth in Sting. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new brands like Cream Bell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its products like Sting, Mountain dew, & Cream bell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide an adequate margin of safety given the fact that the majority of the optimism has been baked in & management believes the growth in the current year was exceptional coupled with highest ever EBITDA margins which remain to be seen- whether sustainable or not.

Q4 CY22 Updates

Financial Results & Highlights

Detailed Results:

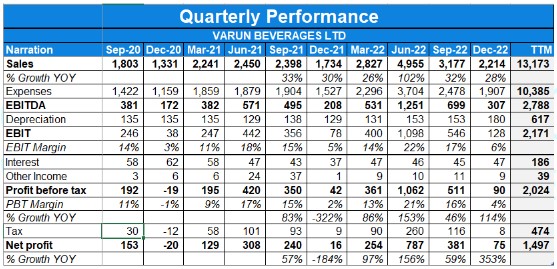

- The consolidated revenues for the current quarter increased by 27.7% YoY whereas PAT increased by 107.8% YoY.

- The company saw an EBITDA rise of 48.1% YoY and a volume rise of 17.8% YoY in the quarter.

- Net realization increased by 6% to Rs. 164 primarily due to price hikes in select SKUs, rationalized discounts/incentives, and improvement in the mix of smaller SKUs (250ml) especially the energy drink – Sting which has a higher net realization. Sting is now 9.6% of total sales volumes in India.

- Depreciation increased by 16% in CY 2022 on account of the capitalization of assets and Finance costs remained almost flat in CY 2022.

- CSD constituted 65%, Juice 5%, and Packaged Drinking water 30% of total sales volumes in Q4 CY22.

- Gross margins reduced by 180 bps to 52.5% from 54.3% in CY2022 primarily because of an increase in preform prices by over 30% during the year.

- EBITDA increased by 48.1% to Rs. 3,075.1 mn and EBITDA margins improved by 192 bps to 13.9% in Q4 CY2022.

- Net debt stood at Rs. 34,096 million as on Dec 31, 2022, as against Rs. 30,053 million as on Dec 31, 2021. Net debt increased on account of Greenfield expansion in Rajasthan and Madhya Pradesh and brownfield expansion at 6 plants for CY 2023 in India. Debt/Equity stood at 0.64.

- As on Dec 31, 2022, the CWIP of ~Rs. 6,066 mn is towards greenfield expansion in Rajasthan & Madhya Pradesh and brownfield expansion at 6 plants for CY 2023 in India. The net capex estimated for CY2023 is around Rs. 15,000 million (including CWIP).

- Working capital days have remained stable at ~ 36 days as on Dec 31, 2022, while Inventory of finished goods has increased in preparation for the next season in order to avoid any stock-out situation.

- The Board of Directors recommended a final dividend of Rs. 1.00 per equity share. With this, the total dividend declared for the year ended 31st December 2022 stands at Rs. 3.50 per equity share.

Investor Conference Call Highlights:

- The EBITDA margins improved despite the GPM decreasing owing to operational leverage.

- PAT grew by 107.8% to Rs.15,501 million driven by high revenue growth from operations, margin improvement, and transition to a lower tax rate in India.

- During CY22, the Company invested in various expansion projects including Rs. 6,300 million primarily for greenfield expansion in Bihar and Jammu and brownfield expansions in India, Rs. 2,500 million in brownfield expansion in Morocco and Zimbabwe & Rs. 3,700 million for purchasing land for future capacity expansions for the year 2024-25.

- In Morocco, it started operations in January for the distribution of the complete range of products. It wants to stabilize that business in the next 3 to 6 months and maybe once it stabilizes, it will talk to PepsiCo for India operations as well.

- The inventory days rose as Instead of starting prebuilding in January and February, the company started prebuilding in December itself. Secondly, since resin prices are always at the lowest in November and December, the company prefers to pre-stock it as much as possible and that is another reason for the increase in inventory.

- The company states that Q4 nos are much stronger YoY due to increased contributions from South & West territories.

- The company currently touched 3 million distribution outlets & is targeting 3.5 million for the coming year.

- The company is tripling its dairy unit capacity & expects a national roll-out in 2024.

- The management states that its single-serve business which has higher margins is growing at a much faster pace than the multi-serve business.

- The capital advances to equipment manufacturers stand at 450 Crs.

- The management explains that the share of energy drinks in the total market has increased to 10-15% owing to explosive growth in 5-7 years because of attractive pricing for the customers.

- The company is seeing decent growth in rural areas unlike other FMCG cos since the electricity and the power situation is getting better, its Visi Coolers are reaching leading to cold drinks being sold when they are cold, which is helping its growth in rural markets.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher preform prices. The company is witnessing a strong performance in its Southern & western territories coupled with explosive growth in Sting. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new brands like Cream Bell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its products like Sting, Mountain dew, & Cream bell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide an adequate margin of safety given the fact that the majority of the optimism has been baked in & management believes the growth in the current year was exceptional coupled with highest ever EBITDA margins which remain to be seen- whether sustainable or not.

Q3 CY22 Updates

Financial Results & Highlights

Detailed Results:

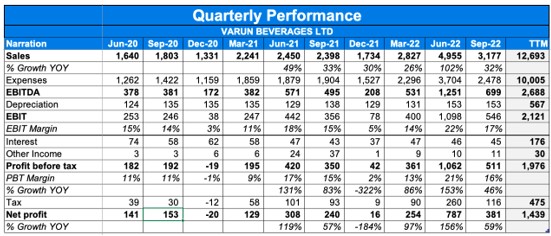

- The consolidated revenues for the current quarter increased by 32% YoY whereas PAT increased by 59% YoY.

- The company saw an EBITDA rise of 41.3% YoY and a volume rise of 24% YoY in the quarter.

- Increase in net realization is primarily driven by higher mix of smaller SKUs (250ml) especially the energy drink – Sting which has higher net realization, and its mix is increasing in the sales volumes.

- Quarterly sales volume was 190 mn cases in Q3 vs 300 mn cases the previous quarter and 153 mn cases the previous year.

- CSD constituted 70%, Juice 5%, and Packaged Drinking water 25% of total sales volumes in Q3 CY22.

- Gross margins increases by 90 bps YoY to 53.7% despite inflationary raw material environment.

- EBITDA margin improved by 138 bps to 22% in Q3 CY2022 led by higher realization and operating leverage from increased sales volume.

- The main driver of growth during the quarter was Sting which performed exceedingly well across all geographies.

- The company launched some product in the value added Dairy segment which received a good response with the management being confident of improving contribution from these new launches going ahead.

- In testimony of strong relationship between Varun Beverages Limited and PepsiCo Inc., Board of Directors approved the proposal to enter into an agreement by Varun Beverages Morocco SA (a wholly owned subsidiary of the Company) to distribute & sell “Lays, Doritos and Cheetos” for PepsiCo wholly owned subsidiaries in the territory of Morocco with effect from January 2023.

- As per the co-manufacturing agreement dated 28th February 2022, the manufacturing plant in Kosi, Uttar Pradesh commenced the trial production of Kurkure Puffcorn for PepsiCo India Holdings Private Limited.

Investor Conference Call Highlights:

- The company’s India business delivered an organic volume growth of 22% while International grew by 31%. This was mainly contributed by strong performance of Sting.

- Realization per case improved by 6.8% to Rs. 167 per case in Q3CY22 primarily driven by a higher mix of smaller SKUs .

- The morrocoy snacks business of Pepsico in which VBL has entered was an already existing business of 150 crore. VBL has acquired distribution rights for the products of Lays, Doritos and Cheetos.

- The cumulative nine months average mix of Sting is 8.5% while the mix in the last quarter was more than 12%.

- Sting is currently reaching everywhere with a distribution of 2 million plus outlets. It is currently having the highest penetration of any of the company’s products.

- Tropicana is also doing extremely well. The only constraint faced is a constraint of production due to which Pathankot facility distribution has gone up to only 15% of total outlets, which is expected to be resolved by next year.

- There is a 25%-30% difference in realization in the domestic business. This is largely contributed by Sting which has a realization higher by 65%.

- In International business, the major growth has come from Morocco, wherein not much growth has come in from CSD but from water, as water is growing much faster in Morocco.

- The company is looking at a 1200-1300 crore greenfield and brownfield capex this year which would split in half-half. This is expected to be commissioned before the season by February.

- The management maintain a EBITDA margin guidance of 21% for the year.

- The management sees resin pricing cooling down and sugar prices remaining stable for the short term.

- The net debt on the company’s books currently stands at about 2,300 crore.

- The company plans to grow in Africa by stabilizing one country at a time and the management is very positive about the company’s growth prospects in Africa.

- For the time being, VBL is only distributing and selling the 150 crore existing Lays, Doritos and Cheetos business in Morocco.

- The company has a first mover advantage in the energy drinks market with Sting and is seeing competition trying to counter it.

- Tropicana and Dairy are both done in the same plant, so the company is adding one more plant next year. That will double the capacity for Dairy as well as Tropicana.

- In the current season, the company could not supply much of dairy due to capacity constraints, which is expected to be the same during the next season too.

- The capacities for Dairy are expected to come in after the season. Currently, dairy distribution is restricted to the north region.

- The company shifted to the new tax regime in the second quarter of this year. The blended tax rate would be 22.5% which would be an advantage of 3% in the overall tax rate of the company.

- The distribution rights for the company in Morocco can pave the way for a much larger snacking business in the future.

- Zimbabwe is doing extremely well for the company. The peak season for the country is October to December which is expected to bring in huge sales.

- The company currently is not open and not looking for any private label business manufacturing.

- The company is adding 40000-50000 chilling equipments each year and has reached to three million dealers. Every year this is expected to go up by 10% and the carrying size with these dealers is also expected to go up 5%-7% every year.

- The capex being planned is for all PET and the expected capacity to be added is 20% of total capacity.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher preform prices. The company is witnessing strong performance in its exports division. VBL’s efforts in deleveraging the balance sheet are resulting in significant finance costs reduction thus improving debt profile as well as PAT. Sting has been a huge proven success for the company carrying forward growth. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new ventures like Cream Bell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the higher potential of its products like Sting, Mountain dew, & Cream bell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels provide little margin of safety.

Q2 CY22 Updates

Financial Results & Highlights

Detailed Results:

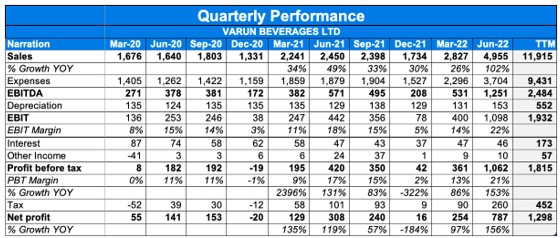

- The consolidated revenues for the current quarter increased by 102% YoY whereas PAT increased by 156% YoY.

- The company saw an EBITDA rise of 119% YoY and a volume rise of 96% YoY in the quarter.

- Realization per case improved driven by price hike in select SKUs and changes in SKU mix.

- CSD constituted 73%, Juice 9%, and Packaged Drinking water 18% of total sales volumes in Q2 CY21.

- Gross margins fell by 302 bps YoY to 50.5% due to increase in preform prices by 30%.

- EBITDA margin improved by 194 bps to 25.2% in Q2 CY2022 led by higher realization and operating leverage from increased sales volume.

- During H1CY22, the net capex included Rs 6,700 mn primarily for setting up of new greenfield production facilities in Bihar and Jammu and brownfield expansion at Sandila facility. The net capex includes capitalization of CWIP amounting ~ Rs. 5000 mn which was outstanding as of Dec’21.

- Capacity utilization in India during the peak month was close to 90% driven by best ever sales volumes.

- The board of directors have recommended a dividend of 2.5 per share. Total cash outflow would be Rs. 1624 mn.

Investor Conference Call Highlights:

- On the profitability front, despite the inflationary raw material environment, the company witnessed little impact on its gross margins during the quarter because of early stocking of key raw materials and improvement in realizations.

- VBL was recently awarded from PepsiCo as the best bottler in Africa, Middle East and South Asia(AMESA) region for the year 2021.

- Working capital days reduced to 17 from 24 the previous year.

- Out of 3 million total outlets, 2.6 mn are composite and 0.4 mn are dedicated to only Sting. The total mix includes 250k international outlets.

- The company is in the process of setting up two large greenfield plants in Madhya Pradesh and Rajasthan. It is also adding more lines in Bihar and other more territories.

- The company to add more 30% CSD/JBD PET capacity by the next year.

- The company sold 262 million cases in Indian and 37.7 mn cases in International areas in Q2.

- Sting has grown by 185% in H1 with the mix to the total volume being 7.2%

- Dairy distribution is only restricted to the north due to production happening in only a single plant in Punjab. Dairy has been doing well in its respective regions.

- The company is writing off RGB assets as and when needed, as the demand is heavily shifting from RGB to PET with the mix of glass being under 10%.

- Capex for CY22 is already done as the season is over. Whatever spending will be done, will be for CY23 and will be parked in the capital work-in-progress and will be capitalized when the assets will be put to use.

- The management believes that a lot of territories acquired by the company are still underpenetrated, leaving a huge scope of growth for the company. This makes the management confident of double-digit growth over the next few years.

- The company is distributing juices in 60% – 70% of the total outlets.

- The management expects PET raisin prices to ease down going ahead leading to better margins.

- The management believes that the beverage industry should do a double-digit volume growth over the next few years.

- In FY22, the company did 670 crore capex and plans to do 1200 crores in FY23, which will result in 30% additional capacity of CSD/JBD/PET capacity.

- HoReCa and modern trade channels contribute to 9% of the sales.

- The Sri Lankan environment and situation does not affect the company because Sri Lanks’s contribution to sales is about 2%.

- The management states that margins can be easily maintained over the next few quarters and may even improve if oil prices come down.

- The management is open to expanding to any new geography, if PepsiCo offers. They are also in discussion with PepsiCo for new products in pipeline.

- The manufacturing of Kurkure, which is a new tie-up with pepsico, will start by October-November end.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher preform prices. The company is witnessing strong performance in its exports division. VBL’s efforts in deleveraging the balance sheet are resulting in significant finance costs reduction thus improving debt profile as well as PAT. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new brands like Sting, Cream Bell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its products like Sting, Mountain dew, & Cream bell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide any margin of safety.

Q4 CY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1CY22 | Q1CY21 | YoY % | Q4CY21 | QoQ % | |

| Sales | 2204 | 1805 | 22.1% | 1134 | 94.4% |

| PBT | 275 | 175 | 57.1% | -33 | 933.3% |

| PAT | 195 | 125 | 56.0% | -20 | 1075.0% |

| Consolidated Financials (In Crs) | |||||

| Q1CY22 | Q1CY21 | YoY % | Q4CY21 | QoQ % | |

| Sales | 2876 | 2276 | 26.4% | 1766 | 62.9% |

| PBT | 361 | 195 | 85.1% | 42 | 759.5% |

| PAT | 271 | 137 | 97.8% | 33 | 721.2% |

Detailed Results:

- The consolidated revenues for the current quarter increased by 26% YoY whereas PAT increased by 98% YoY.

- The company saw an EBITDA rise of 39.1%% YoY and a volume rise of 18.7% YoY in the quarter.

- Realization per case improved by 6.3% to Rs.157.3 in Q1 CY2022 driven by price hike in select SKUs, change in SKU mix and higher realization in international markets.

- CSD constituted 70%, Juice 7%, and Packaged Drinking water 23% of total sales volumes in Q1 CY21.

- Gross margins fell by 427 bps YoY to 51.5% due to increase in preform prices by 30%.

- EBITDA margin improved by 175 bps to 18.8% in Q1 CY2022 led by higher realization and operating leverage from increased sales volume.

- Finance costs for the company reduced by 19.0% to Rs.46.96 Cr primarily because of lower average cost of borrowing.

- During Q1 CY 2022, the new beverage manufacturing plant in Bihar and the new backward integration plant in Jammu & Kashmir commenced commercial production.

- The company has written off the CSD glass and can line in its Roha plant and has shifted the packaged drinking water line from this plant to its Paithan plant.

- The Board of Directors has recommended a bonus issue of 1 equity share of Rs. 10 each for every 2 equity shares of Rs.10 each held by shareholders of the Company.

Investor Conference Call Highlights:

- The company entered into an agreement to manufacture “Kurkure Puffcorn” for PepsiCo & commercial production is expected to start from Q3 of CY22.

- The management states that the enhancement in go-to market coupled with chilling equipment is helping the company to gain market share.

- The company’s new products like Sting (contributing 6-7% of volumes) grew by 131% in this quarter, whereas other products like dairy (contributing 0.5%) & Tropicana (contributing 2%) are already being produced at full capacity.

- The management is guiding for international capex of Rs.1-1.5 Cr in CY22.

- The management doesn’t expect any major jump in profit margins except due to operating leverage.

- Since the company has enough inventory for its key ingredients like PET resin for the full season coupled with sugar prices being in the same range, it doesn’t expect any major cost escalation.

- The company did a write off Rs.14.5 Cr in its plant & machinery in Roha to consolidate the production of these products with its other larger capacities. This write off was recorded as other expenses in P&L statement.

- The management states that out of total volume of 180 million, 147 came from India & the rest 33 came from international markets.

- The company’s Net debt as on 31st March 2022 was approximately Rs. 3,100 Cr which included additional financing for inventory, which was created for PET stocking.

- The capex done in Q1 so far were for the backward integration of the Jammu plant, the brownfield expansion of the Sandila plant and for the implementation of the new Bihar plant.

- The management states that it bought most of the PET requirement till Q3CY22 at the end of last year which was at a reasonable price level.

- Home consumption: out of home consumption mix stood at 35:65 from 65:35 last year.

- The management assures that there are no problems with the Sri Lanka business.

- South-west volumes were at 1/3 of total volumes.

- The company will initially make a small investment of Rs.20-23 Cr for production of Kurkure Puffcorn.

- The management states that the 6% increase in realizations involves 1-2% coming from pricing & remaining 4% from cutting back discounts.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher preform prices. The company is witnessing strong performance in its exports division. The management expects to see EBITDA rise to 20-21% in the next few quarters. VBL’s new plants in Bihar and Jammu have online in this quarter. VBL’s efforts in deleveraging the balance sheet are resulting in significant finance costs reduction thus improving debt profile as well as PAT. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new brands like Sting, Cream Bell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its emerging products like Sting, Mountain dew, & Cream bell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide any margin of safety.

Q4 CY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4 ‘21 | Q4 ‘20 | YoY % | Q3 ‘21 | QoQ % | CY21 | CY20 | YoY% | |

| Sales | 1134 | 867 | 30.7% | 1719 | -34% | 8675 | 6653 | 30.3% |

| PBT | -33 | -66 | 50% | 205 | -116% | 66 | 681 | -90.3% |

| PAT | -19 | -51 | -62.2% | 146 | -113% | -51 | 489 | -110.4% |

| Consolidated Financials (In Crs) | ||||||||

| Q4 ’21 | Q4 ‘20 | YoY % | Q3 ‘21 | QoQ % | CY21 | CY20 | YoY% | |

| Sales | 1765 | 1356 | 30.1% | 2477 | -28.7% | 9026 | 6592 | 36.9% |

| PBT | 41 | -18 | 327.7% | 350 | -88.2% | 1006 | 362 | 177.9% |

| PAT | 32 | -7 | 557.1% | 258 | -87.5% | 746 | 357 | 108.9% |

Detailed Results:

- The current quarter was very good for the company with a 30.1% YoY rise in consolidated revenues & a PAT rise of 557% YoY.

- Yearly figures were even better with 36.9% YoY rise in revenues and 108% YoY rise in PAT due to low base last year.

- The company saw an EBITDA rise of 20.5% YoY and a volume rise of 30.3% YoY in the quarter.

- Other income has fallen to Rs 8.54 Cr from Rs 55.69 Cr last year.

- Realization per case grew 2.2% YoY due to higher realizations in international territories

partially offset by higher mix of water. - CSD constituted 61%, Juice 5%, and Packaged Drinking water 34% of total sales volumes in Q4 CY21.

- Gross margins fell by 476 bps YoY due to increase in pet prices (18%) & increase in sugar prices (2%) in India.

- EBITDA margin was stable at 18.8% in Q4 CY21 despite a fall in gross margins because of operating leverage on account of higher volume.

- Finance costs for the company declined 39.8% YoY due to the repayment of some debt and a lower average cost of borrowing.

- Net debt to equity stood at 0.72 times.

Investor Conference Call Highlights:

- The company for the first time ever reported profits in a seasonally soft quarter of December due to strong volume growth.

- The third wave did not have any significant impact on the business and the company continues to further strengthen its distribution network.

- CY2021 total sales volume grew by 33.8% to 569.1 million cases.

- Working capital days increased to 35 at the December primarily because of higher stocking of pet chips/ preforms.

- During CY2021, net CAPEX stood at Rs. 3500 million. Out of which 1300 million was towards brownfield expansion in certain plants in India and 2200 million was towards brownfield expansion in Morocco and Zimbabwe.

- As of December 2021, Capital work-in-progress stood at approximately Rs. 5000 Million primarily for setting up of new greenfield production facilities in Bihar & Jammu and brownfield expansion at Sandila facility.

- The company has announced an interim dividend of 2.5 per share with pay-out of 1082 Million.

- The management maintains that it will always keep the capex around the depreciation figure.

- Currently there is no capex planned for new geographies. The management is looking out for in-organic opportunities of growth.

- The company plans to put-out 40,000 visi-coolers in the coming year as it had done in the past year.

- The out-of-home consumption was 65% and in-home consumption was 35% for the year.

- Sting has been doing extremely well for the company with 440% YoY growth contributing to 5% of the product mix.

- The company is in a finalization stage of entering Democratic Republic of Congo and plans to distribute products for a year from the existing capacities at the Morocco and Zambia plants.

- The company will be testing the markets of Congo and optimally utilising plants in Africa as the off-season in Morocco coincides with the busy season in DRC.

- If the Congo business turns out to be promising, the company may plan a capex in the future.

- The rise in realization per case internationally to Rs 193 per case has been due to passing on PET price increase to the consumers.

- The management states that the company can look at 20% – 21% EBITDA margin range going forward.

- The current debt levels of the company stand at 3000 crore and the company plans to reduce it by 40% in CY22.

- The Tropicana volume mix for the company is 2.3% currently.

- The Bihar and Jammu plants are expected to be ready before the peak season and will be producing during the March

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher PET prices. The management expects good growth in international realizations due to passing on the increased cost of PET to customers. The management expects to see EBITDA rise to 20-21% in the next few quarters. VBL’s new plants in Bihar and Jammu are expected to come online by the time the peak summer season starts. VBL’s efforts in deleveraging the balance sheet are resulting in significant finance costs reduction thus improving debt profile as well as PAT. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new brands like Sting, Cream bell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its emerging products like Sting, Mountain dew, & Cream bell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide any margin of safety.

Q3 CY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3 ‘21 | Q3 ‘20 | YoY % | Q2 ‘21 | QoQ % | 9MCY21 | 9MCY20 | YoY% | |

| Sales | 1719 | 1315 | 30.72% | 1994 | -13.79% | 5519 | 4081 | 35.24% |

| PBT | 205 | 104 | 97.12% | 334 | -38.62% | 714 | 269* | 165.4% |

| PAT | 146 | 79 | 84.81% | 238 | -38.66% | 509 | 278 | 83.09% |

| Consolidated Financials (In Crs) | ||||||||

| Q3 ’21 | Q3 ‘20 | YoY % | Q2 ‘21 | QoQ % | 9MCY21 | 9MCY20 | YoY% | |

| Sales | 2477 | 1843 | 34.40% | 2507 | -1.20% | 7260 | 5236 | 38.66% |

| PBT | 350 | 192 | 82% | 420 | -16.67% | 965 | 448* | 115% |

| PAT | 258 | 161 | 60% | 319 | -19.12% | 713 | 365 | 95.34% |

*Contains exceptional item of Rs 66.5 Cr for impairment of certain plant & equipment

Detailed Results:

- The current quarter was very good for the company with a 34.4% YoY rise in consolidated revenues & a PAT rise of 60% YoY.

- H1 figures were even better with 39% YoY rise in revenues and 95% YoY rise in PAT due to low H1 last year.

- The company saw an EBITDA rise of 29.9% YoY and a volume rise of 28.4% YoY in the quarter.

- Other income has risen to Rs 36.9 Cr from Rs 3.5 Cr last year.

- Realization per case grew 3.6% to Rs 156.4 due to higher realizations in international territories

partially offset by higher mix of water. - CSD constituted 70%, Juice 5%, and Packaged Drinking water 25% of total sales volumes in Q3 CY21.

- Gross margins fell by 278 bps YoY due to increase in pet prices (18%) & increase in sugar prices (2%) in India.

- EBITDA margin was stable at 20.6% in Q3 CY21 despite a fall in gross margins because of operating leverage on account of higher volume.

- Finance costs for the company declined 26.4% YoY due to the repayment of some debt and a lower average cost of borrowing.

- Net debt to equity stood at 0.6 times.

Investor Conference Call Highlights:

- The company is undertaking measures to use lightweight PET preforms which will not only reduce cost in the near term but also provide structural benefit.

- An amount of about INR 200 million from the total foreign currency provision was reversed to other income due to a corresponding reduction in the total foreign currency liability in Zimbabwe.

- The company’s gross margins have decreased due to high PET prices. However, the company in consultation with Pepsi is producing light-weighted bottles, which will help in mitigating the cost increase.

- The management states that the company normally passes on any increase to the consumer.

- The management is confident about maintaining its EBIDTA margins which are one of the highest in the beverage industry.

- The company is doing capex in Bihar to increase its market penetration in the region where it had to previously meet the demand by sourcing from other states because of which the company had to incur high freight costs.

- The management states that Bihar is one of the 4 underpenetrated states i.e. Orissa, Bihar, Jharkhand, and Chhattisgarh for VBL. These states have recorded growth of 60% in the last 9 months.

- The capex in Bihar is Rs 285 Cr which will be spent in the next 6 months.

- The debt component in Varun beverages has decreased from Rs.3000 Cr to Rs.2400 Cr In the past 1 year. Further, the group companies have close to Rs.100 Cr debt since Rs.1000 Cr of debt of RJ corp was paid off.

- The company was able to grow at 37% in South & West despite missing out on the past two peak seasons due to the pandemic.

- The management states that the company always takes in a large quantity of stocks during the off-season, which is when the best pricing of raw material is available because of which inventory levels appear optically higher at the end of December.

- The growth in Tropicana has been close to 40% whereas dairy beverage has grown at 57%.

- Since the out-of-home sales are back to the pre-COVID level and the in-home has sustained, it has led to 11% CAGR in the last 2 years.

- The company’s new portfolios have grown very well with sting growing faster than the market and the portfolio itself & Gatorade growing by 53%.

- The company’s capex in Bihar will involve a CSD line with a capacity of 720 bottles per minute, a juice line would be 300 bottles a minute, a water line will be 300 bottles a minute and a glass line will be 600 bottles a minute. This capacity will help cater to Bihar & West Bengal markets.

- The revenue to capex ratio that the company expects from its Bihar capex is roughly 2.5 times.

- The customer facility that the company is putting up for the plastic preform and closures will involve a capex of Rs.190 Cr which will get completed within the next 6 months. This capex will help in backward integration for all the new acquisitions of the company.

- The average borrowing costs have been reduced by 100 bps from 6.5% to 5.5% in the last 1 year while the marginal costs were at 4.2%.

- The company’s international realizations increased by 10% in the last 9 months due to improved performance from its Morocco unit.

- The growth in non-carbonated drinks in the last 2 years was lower than expected due to the pandemic, however, the management expects the segment to rebound quickly.

- The management is focused on top-line growth as its EBIDTA margins of 21% are the best in the industry so there isn’t much room for margin appreciation.

- The management is targeting to increase the number of outlets by 10% to 15%, which would be close to about 300,000 outlets.

- The company’s e-commerce plus modern trade contribution of sales was at 5.6%.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite falling gross margins due to higher PET prices. The management expects good growth in 3 key categories of Tropicana, Sting, and Mountain Dew Ice which have already led to higher realizations. The company has also done well to shield itself from commodity price pressures by procuring PET resin earlier on and stocking a lot in the off-season. VBL is planning to set up a unit in Bihar to address the underpenetrated markets of Bihar and make inroads into its neighboring states. VBL’s efforts in deleveraging the balance sheet are resulting in significant finance costs reduction thus improving debt profile as well as PAT. It remains to be seen what challenges the company will face in trying to maintain its growth momentum while setting up the new facility and how long will it take for the new brands like Sting, Creambell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its emerging products like Sting, Mountain dew, & Creambell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide any margin of safety.

Q2 CY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Jun-21 | Jun-20 | YoY % | Mar-21 | QoQ % | H1CY21 | H1CY20 | YoY% | |

| Sales | 1994 | 1421 | 40.32% | 1805 | 10.47% | 3800 | 2766 | 37.38% |

| PBT | 334 | 159 | 110.06% | 175 | 90.86% | 509 | 165* | 208.5% |

| PAT | 238 | 122 | 95.08% | 125 | 90.40% | 363 | 199 | 82.41% |

| Consolidated Financials (In Crs) | ||||||||

| Jun-21 | Jun-20 | YoY % | Mar-21 | QoQ % | H1CY21 | H1CY20 | YoY% | |

| Sales | 2507 | 1668 | 50.30% | 2276 | 10.15% | 4783 | 3393 | 40.97% |

| PBT | 420 | 182 | 131% | 195 | 115.38% | 614 | 190* | 223% |

| PAT | 319 | 143 | 123% | 137 | 132.85% | 456 | 203 | 124.63% |

*Contains exceptional item of Rs 66.5 Cr for impairment of certain plant & equipment

Detailed Results:

- The current quarter was up for the company with a 50% YoY rise in consolidated revenues & a PAT of Rs 319 Cr vs Rs 143 Cr last year.

- The company saw an EBITDA rise of 51.1% YoY and a volume rise of 45.4% YoY in the quarter.

- Other income has risen to Rs 244 Cr from Rs 27 Cr last year.

- Realization per case grew 2.8% to Rs 160.8 due to higher realizations in international territories

partially offset by higher mix of water. - CSD constituted 78%, Juice 7%, and Packaged Drinking water 15% of total sales volumes in Q2 CY21.

- Gross margins fell by 128 bps YoY to 55.8% in Q1 due to change in product mix and marginal increase in raw material prices.

- EBITDA margin improved by 30 bps YoY to 23.3% in Q2 CY21 despite a fall in gross margins.

- Finance costs for the company declined 36.9% YoY due to the repayment of some debt and a lower average cost of borrowing.

- Net debt to equity stood at 0.63 times and net debt to TTM EBITDA stood at 1.69 times.

- Working capital days increased to 24 days from 20 days in June 2020 due to higher stocking of pet resin due to low prices earlier in 2020.

- The company announced a dividend of Rs 2.5 per share.

Investor Conference Call Highlights:

- The company has delivered high revenue growth of 49% on account of the lower base of the previous year and marginal increase in realizations.

- The management states that its EBIDTA margins remained stable on account of the cost optimization measures that it took last year.

- Other income rose by 816% in the current year due to an amount of Rs.114.4 million from the total foreign currency provision was reversed to other income, due to a corresponding reduction in the total foreign currency liability in Zimbabwe.

- The Company has done a capex of Rs 190 Cr for organic expansion in Zimbabwe, Morocco, and India in H1.

- Working capital days marginally increased to around 24 days from 20 days on account of higher stock of PET to take benefit of lower prices

- Realization per case in international territories is Rs180 and that in local markets Rs156

- Gross margins were down due to higher sugar prices, change in product mix, and higher freight costs

- The management states that the growth in realizations despite no price hikes was led by growth in higher realization products like Sting, Mountain Dew Ice, and Juices and by the higher share of international sales. International realizations were at Rs 180+ while Indian realizations were at Rs 156+ per case.

- The drop in gross margins was mainly due to a change in product mix and the rise in sugar prices.

- The rise in resin stock was mainly due to loss of sales and production in May from local lockdowns and to take benefit of lower prices earlier in the year.

- Sting has already crossed the 10 million cases mark in H1 and is expected to be a big brand in the future considering its price point in comparison to RedBull according to the management.

- The management expects the capex for VBL to be close to depreciation for the next 2 years.

- The total debt repayment in H1 so far was at Rs 466 Cr. VBL is expected to reduce another Rs 200 Cr of long-term debt in the next 6 months.

- The management states that it is focusing only on the North Zone for the sales and brand development of Creambell dairy beverages.

- The management states that it will not have any store additions this year due to the pandemic.

- Most of the improvement in international operations was driven by growth in Zimbabwe and Morocco.

- The company did sales volumes of 127 million in India and 25.3 million abroad. Around 2/3rds of the volumes were sold in the North & East zones while 1/3rd was sold in the West & South zones.

- The management highlights that due to consolidating of plants, its transportation costs which are a part of other expenses have decreased sequentially.

- The management states that the major growth in 2020 had come from rural areas while in the current year the rural-urban break up is balanced. The in-home consumption is going steady & large packs doing much better than small packs.

Analyst Views:

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen good YoY growth in the quarter with a sustained EBITDA margin despite local lockdowns in May and falling gross margins. The management expects good growth in 3 key categories of Tropicana, Sting, and Mountain Dew Ice which have already led to higher realizations. The company has also done well to shield itself from commodity price pressures by procuring PET resin earlier on and stocking enough requirement to last till Oct. VBL’s efforts in deleveraging the balance sheet is resulting in significant finance costs reduction thus improving debt profile as well as PAT. It remains to be seen what challenges the company will face in trying to maintain its growth momentum without the addition of new stores and how long will it take for the new brands like Sting, Creambell & others to start contributing meaningfully to the company’s sales. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the good potential of its emerging products like Sting, Mountain dew, & Creambell beverages, Varun Beverages is a good consumption stock to watch out for at present. However, the valuation at current levels does not provide any margin of safety.

Q1 CY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Mar CY21 | Mar CY21 | YoY % | Dec CY20 | QoQ % | |

| Sales | 1805 | 1344 | 34.30% | 868 | 107.95% |

| PBT | 175 | 5*** | 143.06% | -66 | -365.15% |

| PAT | 125 | 77** | 62.34% | -52 | -340.38% |

| Consolidated Financials (In Crs) | |||||

| Mar CY21 | Mar CY21 | YoY % | Dec CY20 | QoQ % | |

| Sales | 2276 | 1725 | 31.94% | 1357 | 67.72% |

| PBT | 195 | 8 | 2338% | -19 | -1126.3% |

| PAT | 137 | 60* | 128% | -7 | -2057.14% |

*contains negative tax expense of Rs 52 Cr

**Contains negative tax expense of Rs 72 Cr

***contains exceptional item of Rs 66.5 Cr for impairment of certain plant & equipment

Detailed Results

- The current quarter was up for the company with a 32% YoY rise in consolidated revenues & a PAT of Rs 137 Cr.

- The company saw an EBITDA rise of 40.7% YoY and a volume rise of 32.8% YoY in the quarter. CY20 EBITDA fell 17% YoY.

- Other income in Q1 fell 77.3% YoY.

- Organic sales volumes grew 24.7% YoY. Realization per case was flat at Rs 148.

- CSD constituted 70%, Juice 7.2%, and Packaged Drinking water 22.8% of total sales volumes in Q1 CY21.

- EBITDA margin improved by 86 bps YoY in Q1 CY21.

- Gross margins fell by 294 bps YoY to 55.8% in Q1 due to change in product mix and lower realization in international operations.

- Finance costs for the company declined 33.4% YoY due to the repayment of some debt and a lower average cost of borrowing.

- The company announced a bonus share issue of 1 share for every 2 existing shares.

Investor Conference Call Highlights

- The management maintains that VBL has adequately stocked its supply chain and has not seen any issues from the local lockdowns so far. The situation is much better than last year as VBL has some stores to supply rather than no supply like last year.

- The rural segment is doing much better than the urban segment according to the management as the lockdowns are less severe. It has grown >50% in 1 year.

- The company is not facing any input price pressures. Sugar prices are running normally. PET resin prices have gone up in the last 2 months, but the company is adequately stocked beforehand to last till Sept or Oct and this price increase is expected to normalize by then.

- The expected tax rate for CY21 is expected to be 25%.

- The 3 categories that are doing very well currently for the company are the energy drink Sting (which has grown almost 10 times in volumes in 2 years), the newly launched Mountain Dew Ice (as a competitor to Limca), and Tropicana (which is the only juice in the country available in PET format).

- The company has reduced Rs 600 Cr of debt in the last 1 year.

- The North is the best performing zone for VBL. It had invested a lot for expansion in the South and the East but the improvements have been slow since the start of the pandemic.

- The company will stick to its existing capex plans and will keep it lower than the depreciation for the year.

- The management admits that there isn’t clear evidence of VBL outpacing the market as the entire industry has done well in the past 1 year.

- The peak season for the industry has again been affected due to the pandemic although not as severe as last year according to the management.

- Sting has grown 2.5 times in the past 1 year for VBL.

- The management clarifies that although out of home consumption has gone down a lot, once the situation normalizes, it will not be adding too much to organic growth as it will just be substituting the current in-home consumption to some extent since all of this growth has come from the same outlets and visi-coolers that are present in the market.

- The management has stated that it has already put all the planned visi-coolers for the year before the peak season and will not be adding any more for the year.

- The management has stated that the rise in standalone other expenses is mainly variable expenses which have risen with volume growth. Other contributing factors to it are asset write-offs that the company has done like for a glass line in Bazpur of Rs 15 Cr.

- The management hopes to see the start of the currency reserve reversal in Zimbabwe soon.

- There should not be any raw material factors weighing down the margin for CY21 according to the management. But the exact margins ultimately will depend on volumes sold and product mix.

- The North and East Zones have grown 38% in the past year.

- Tropicana is still small for the company, accounting for 3-4% of volumes.

- The biggest competitor for Tropicana is Real by Dabur. But the distribution reach of VBL is much bigger than the competition especially in the rural regions and thus the management is confident of high growth in this product category.

- The management feels that it will take 2 or more years for the South & West zones to start showing performance because of the addition of visi-coolers and other measures done by the company.

- The management states that the penetration in the rural areas in the East zone remains low due to the low power situation and the penetration should improve as the power situation improves.

- Although the energy drink Sting is assumed to be part of the urban portfolio, its pricing helps it sell well in all regions according to the management.

- There isn’t any significant demand impact from the local lockdowns since in-home consumption is steady and procurement has not stopped totally.

- The Tropicana production capacity is running at close to full utilization.

- There isn’t any price differential as compared to the competitor Coca-Cola in soft drinks right now.

- In terms of pricing action, the company is seeing good demand for the 1.25L pack which is sold for Rs 50 as home consumers are showing more interest in this compared to the 2L pack.

Analyst’s View

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen a good YoY recovery in the quarter with sustained margins. Although the local lockdowns have dampened out of home consumption, the broad demand looks to be steady at the moment. VBL has also seen good growth in 3 key categories of Tropicana, Sting and Mountain Dew Ice, which are expected to be big growth drivers once they scale up in the future. The company has also done well to shield itself from commodity price pressures by procuring PET resin earlier on and stocking enough requirement to last till Oct. It remains to be seen whether there is a further economic disruption in the future from the resurgence of COVID-19 cases in the peak season of April to June which may have severe second-order effects on the company’s performance and. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the arrival of the peak season for the beverages industry, Varun Beverages is a good consumption stock to watch out for at present. However, as it is a capital-intensive business, the current pandemic can put a strain on the Balance Sheet which is already laden with debt. The valuation at current levels does not provide any margin of safety.

Q4 CY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Dec CY20 | Dec CY19 | YoY % | Sep CY20 | QoQ % | CY20 | CY19 | YoY% | |

| Sales | 868 | 895 | -3.02% | 1315 | -33.99% | 4948 | 5714 | -13.41% |

| PBT | -66 | -79 | 16.46% | 104 | -163.46% | 203* | 634 | -67.98% |

| PAT | -52 | -54 | 3.70% | 79 | -165.82% | 226 | 449 | -49.67% |

| Consolidated Financials (In Crs) | ||||||||

| Dec CY20 | Dec CY19 | YoY % | Sep CY20 | QoQ % | CY20 | CY19 | YoY% | |

| Sales | 1357 | 1276 | 6.35% | 1843 | -26.37% | 6593 | 7291 | -9.57% |

| PBT | -19 | -64 | 70% | 192 | -109.90% | 363* | 696 | -47.84% |

| PAT | -7 | -54 | 87% | 161 | -104.35% | 357 | 472 | -24.36% |

*contains an exceptional item of Rs 66.5 Cr for impairment of certain plant & equipment

Detailed Results

- The current quarter was down for the company with a 6.4% YoY rise in consolidated revenues & a PAT loss of Rs 7 Cr.

- CY20 numbers were dismal with a 9.6% YoY revenue decline and a 24.4% YoY PAT decline.

- The company saw an EBITDA rise of 48.8% YoY and a volume decline of 5.7% YoY in the quarter. CY20 EBITDA fell 17% YoY.

- Other income in Q4 fell 84.5% YoY.

- Sales volumes in CY20 fell 13.7% YoY and organic sales volumes fell 20.8% YoY.

- CSD constituted 63%, Juice 5%, and Packaged Drinking water 32% of total sales volumes in Q4 2020.

- EBITDA margin improved by 346 bps in Q4 2020 as compared to Q4 2019.

- Gross margins improved by 472 bps YoY during Q4 2020 & 231 bps in CY20 primarily due to favourable PET chips prices and a higher mix of CSD.

- Finance costs for the company declined 21.6% YoY due to the repayment of some debt and a lower average cost of borrowing.

- Debt to Equity ratio stood at 0.84x and Debt to EBITDA ratio stood at 2.51x as of Dec 31, 2020.

- Working capital days increased marginally to ~ 31 days as of Dec 31, 2020, due to lower sales volumes.

- The company announced a dividend of Rs 2.5 per share.

Investor Conference Call Highlights

- For CY 2020, total sales volumes stood at 425.3 million cases.

- VBL recently introduced a new product variance under the Mountain Dew brand which is a lemon juice based drink called Mountain Dew Ice.

- Realization per case has improved by 4.8% in CY20. This was essentially on account of favourable mix and improvement in realization in the international markets.

- CSD constituted 72.6%, juice constituted 6.3%, and packaged drinking water constitute 21.1% of the total sales volume mix in CY20.

- The management stated that the rise in water sales in Q3 & Q4 was due to the resumption of people consuming drinking water outside as compared to Q2 when all outside activities and consumption were suspended.

- In-home consumption was mostly in CSD and was geared towards large packs.

- On the go consumption reduced to 44% in CY20 from 60% in CY19.

- Glass volumes have declined a lot and all of the growth in CSD is coming from PET bottles.

- The company is planning to add a plant in Bihar in CY21. This expansion will be greenfield.

- The dairy segment is doing well so far. The management has stated that it will continue to monitor the response to it to see the results from the market before expanding into other territories.

- The company doesn’t have any plans to make any large investments into the dairy segment currently.

- Nepal has seen 25% volume growth in Q4. Sri Lanka has seen volume decline due to lockdowns. Morocco has stayed flat due to lockdown while Zimbabwe and Zambia volumes have grown 40% and 17% respectively.

- In CY21, any excess cash will be used for the reduction of debt only according to the management.

- Tax rate for CY21 should be close to 24%.

- Annual volumes for Nepal were close to 16 million; Sri Lanka was about 10.5 million; Morocco was about 18 million; Zimbabwe was 34 million; Zambia was 9.2 million.

- The management has stated that PET prices for VBL will not be affected by rising oil prices as VBL is reasonably covered for the major portion of its year.

- The company is open to international acquisition opportunities as the potential for market growth in India is limited. It is looking at areas in South East Asia and Africa primarily.

- The management reports that VBL has seen market share gains in CY20.

- Contrary to popular belief, VBL does not have 100% of India for Pepsi. It is operating in 85% of Indian territories for Pepsi only.

- There has been no change in territory from 2020 to 2021.

- The management has stated that it expects growth and expansion of the market to continue in 2021 for the recently acquired territories.

- The go-to-market was very weak before when PepsiCo is running it. VBL is improving on it by expanding routes, increasing outlets, and expanding on the number of visi coolers.

Analyst’s View

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen a good YoY recovery in the quarter with sustained margins. Post lockdown demand has remained resilient and water volumes have risen dramatically as on-the-go consumption comes back to normalcy. VBL has also seen good growth in African territories except for Morocco. The company has also done well to shield itself from rising oil prices by covering for PET earlier on. It remains to be seen whether there is a further economic disruption in the future from the resurgence of COVID-19 cases which may have severe second-order effects on the company’s performance. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the arrival of the peak season for the beverages industry, Varun Beverages is a good consumption stock to watch out for at present. However, as it is a capital-intensive business, the current pandemic can put a strain on the Balance Sheet which is already laden with debt. The valuation at current levels does not provide any margin of safety.

Q3 CY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Sep-20 | Sep-19 | YoY % | Jun-20 | QoQ % | 9MSep20 | 9MSep19 | YoY | |

| Sales | 1315 | 1350 | -2.59% | 1421 | -7.46% | 4081 | 4819 | -15.31% |

| PBT | 104 | 99 | 5.05% | 159 | -34.59% | 335 | 713 | -53.02% |

| PAT | 79 | 65 | 21.54% | 122 | -35.25% | 278 | 503 | -44.73% |

| Consolidated Financials (In Crs) | ||||||||

| Sep-20 | Sep-19 | YoY % | Jun-20 | QoQ % | 9MSep20 | 9MSep19 | YoY | |

| Sales | 1843 | 1779 | 3.60% | 1668 | 10.49% | 5236 | 6015 | -12.95% |

| PBT | 192 | 116 | 65.52% | 182* | 5.49% | 381* | 760 | -49.87% |

| PAT | 161 | 81 | 98.77% | 143 | 12.59% | 365 | 526 | -30.61% |

*contains an exceptional item of Rs 66.5 Cr for impairment of certain plant & equipment

Detailed Results

- The current quarter was mixed for the company with a 3.6% YoY rise in consolidated revenues.

- Consolidated Profits were up with over 98% YoY rise.

- 9M numbers were dismal with 13% YoY revenue decline and 31% YoY PAT decline.

- The company saw an EBITDA rise of 17% YoY and a volume decline of 4% YoY in the quarter. 9-Month EBITDA fell 22.7% YoY.

- Other income in Q3 grew 93% YoY.

- Sales volumes in India fell 6.7% YoY while in international territories it grew 5.8% YoY.

- CSD constituted 74%, Juice 6%, and Packaged Drinking water 20% of total sales volumes in Q3 2020.

- Gross margins declined by 149 bps during Q3 2020 primarily due to an increase in the mix of promotional packs like Pepsi PET1, 250ml, Sting PET 250ml, etc.

- Finance costs for the company declined 33.2% YoY due to the repayment of some debt from the funds from the QIP.

Investor Conference Call Highlights

- A rise in demand is expected for the company with the reopening of theatres, restaurants, mass transportation, and outdoor facilities.

- The major factor in the big jump in PAT YoY is the big reduction in finance expenses.

- The management has stated that margins near about 21% are healthy margins for the company in the long term.

- The key focus for the company has remained in-home consumption. The company’s launch of the 1.25 ltr pack at Rs 50 has been very well received. Although go-to-market is expected to rise going forward, the in-home consumption seems to be sustainable.

- In-home consumption has gone up by 20% to 25% YoY.

- Large PET bottle consumption has grown more than 10% YoY.

- The present inventory level is at Rs 848 Cr. It is elevated due to the offseason currently.

- In terms of monthly YoY recovery, the company finally saw positive growth in September with 12% YoY growth.

- The management has stated that it is difficult to provide any specific guidance on margins and RM costs going forward.

- The management expects the company to maintain its pace of adding visi-coolers of less 40,000 units each year.

- The current debt is at Rs 2830-2840 Cr.

- Institutional sales have been very low at only 2-3% of sales.

- Rural & semi-urban sales were at almost 30% each.

- The company has spent around Rs 400 Cr in Capex in the year and this figure represents the majority Capex for the year.

- The management has stated that VBL is among the most profitable soft drink companies in the world. It also stated that the main commodities that affect the company are oil and sugar.

- The company is indeed looking for ways to reduce seasonality in the beverages business but the management acknowledges that this is a deeply embedded and structural characteristic of this industry everywhere. The company sees main newcomer additions in peak summer season and it is looking to reduce seasonality by increasing volumes for these same customers in the rest of the year.

- The management is aiming to maintain >10% growth in the next 3-5 years.

- The company saw a good response to its dairy-based products but had to almost withdraw these products due to the pandemic. The company is now looking to relaunch this segment in Jan or Feb next year.

- The company has stopped making the fizzy Slice juice-based product as it didn’t get a good response in its pilot locations.

- The company is indeed looking at much larger plants and scaling down the smaller plants as operating these smaller plants is much costlier and it is more feasible to either convert into a large plant or shut it down.

- The company has enough plants in South & West and is not looking to add any plants in these zones.

- Tropicana is the only space where the company is running out of capacity and is looking to open a new plant. The Capex required would be at least Rs 200 Cr but this will not happen in the next at least.

- The juice business has grown by 19% in Q3. The main advantages of Tropicana over market rivals is VBL’s distribution reach which is much larger than rivals and the huge volume number of Visi-coolers in the market which the big competitors like Real & B-Natural do not have.

- The compensate pricing with Pepsi has been fixed for 20 years and will not be renegotiated.

Analyst’s View

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen a good recovery in the quarter with a big rise in margins. Post lockdown demand seems to have stayed resilient as in-home consumption has risen along with juice consumption as on-the-go consumption slowly comes back to normalcy. It remains to be seen whether there is a further economic disruption in the future from COVID-19 which may have severe second-order effects on the company’s performance. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the arrival of the peak season for the beverages industry, Varun Beverages is a good consumption stock to watch out for at present. However, as it is a capital intensive business, the current pandemic can put a strain on the Balance Sheet which is already laden with debt. The valuation at current levels does not provide any margin of safety.

Q2 CY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Jun-FY21 | Jun-FY20 | YoY % | Mar-FY21 | QoQ % | 6MFY21 | 6MFY20 | YoY% | |

| Sales | 1421 | 2469 | -42.45% | 1344 | 5.73% | 2766 | 3469 | -20.27% |

| PBT | 159 | 537 | -70.39% | 5* | 3080.00% | 165* | 614 | -73.13% |

| PAT | 122 | 382 | -68.06% | 77** | 58.44% | 199 | 438 | -54.57% |

| Consolidated Financials (In Crs) | ||||||||

| Jun-FY21 | Jun-FY20 | YoY % | Mar-FY21 | QoQ % | 6MFY21 | 6MFY20 | YoY% | |

| Sales | 1669 | 2855 | -41.54% | 1725 | -3.25% | 3393 | 4237 | -19.92% |

| PBT | 182 | 582 | -68.73% | 8* | 2175.00% | 190* | 645 | -70.54% |

| PAT | 143 | 405 | -64.69% | 60*** | 138.33% | 203 | 445 | -54.38% |

*contains an exceptional item of Rs 66.5 Cr for impairment of certain plant & equipment

**Contains negative tax expenses of Rs 71.8 Cr

*** Contains negative tax expenses of Rs 52.2 Cr

Detailed Results

-

- The current quarter was dismal for the company with a 42% YoY fall in consolidated revenues.

- Consolidated Profits were down with over 65% YoY decline.

- The company saw an EBITDA decline of 52% YoY and volume decline of 66% YoY in the quarter.

- Organic volume growth in India declined by 50% due to disruption caused by COVID-19. The same declined by 33% in international territories and 48% on a consolidated basis.

- EBITDA margins declined 501 bps YoY and increased 685 bps QoQ. The EBITDA margin in the current quarter was 23%.

- Sales volumes started picking up gradually from about 25% in April to about 75% in June.

- CSD accounted for 85%, Juices 7%, and packaged water was 8% of total sales volumes.

- Finance costs for the company declined 12.5% YoY due to the repayment of some debt from the funds from the QIP.

- Net debt stood at Rs 2939 Cr as of 30th June 2020 vs Rs 3246 Cr 6 months ago.

- Net capex in the last 6 months was at Rs 243 Cr. Capacity utilization in the peak month was at around 60%.

- Working capital days increased to 20 days vs 14 days last year due to lower sales.

- The company announced an interim dividend of Rs 2.5 per share.

Investor Conference Call Highlights

- The capex mentioned above was primarily towards commitments made prior to March for brownfield expansion at certain plants for new tetra lines for Slice and backward integration.

- The company has not availed moratorium for its debt repayments and has been timely servicing all its debt obligations.

- The management has stated that the company’s go-to-market sales have dropped along with sales in public spaces like theatres. But in-home consumption has increased drastically.

- The management has admitted that Rs 10 is a very competitive price point for juices and the company already has a presence at this price point.

- The company is not looking to change its product mix and add new products. It will instead be focussing on promoting its juices particularly Tropicana brand.

- The management has stated that at least 50% of the current cost savings are sustainable for the long term for the company.

- The company does not see any need to approach PepsiCo for any support currently.

- The main reason for realizations going up is the decline in sales of water in public spaces.

- The company has close to 25% market share but increasing penetration or market share for the current year is still uncertain due to COVID-19.

- The company has indeed gained some market share from local competitors which didn’t open up in time due to COVID-19 at the start of the peak season after Holi.

- The management has stated that the company will aim to keep capex at lower than 50% of depreciation from next year.

- The company has not faced any repayment issues in Zimbabwe in the quarter.

- More in-home consumption has led to an increase in sales of medium and large bottles vs single-serve bottles for the company.

- The company is working on digital and e-commerce channels as per its media strategy.

- The management has stated that as lockdowns are being lifted, the company is slowly coming back to its normal sales levels.

- The management expects performance from international regions to be better than last year as the peak season for the African regions starts from November.

- Realizations have grown 8-9% QoQ in the current quarter.

- The management expects the current volume share to persist as long as public spaces like hotels, theatres, etc come back to normalcy.

- The management expects to run out of capacity for Tropicana by the end of 2021 as the same equipment is used for ambient temperature value-added products under the brand of Cream Bell.

- On-the-go consumption including water was close to 70% pre-covid for the company. Now it is less than 50%.

- The company is not looking to do any capex on juices in the next year so far.

- The company does not need any capacity expansions for at least 20-25% rise in volumes.

- Going forward, discounts or promotions will be dependent only on market demand and competition.

- Around 84.6% of volumes sold in the quarter were domestic and the rest was international.

- Urban areas have been negative or neutral for the company while rural areas have been the fastest-growing segment. The revenue share of rural has gone up by 5-10%.

- The company has held back on the launch of the dairy product due to the COVID-19 outbreak and is looking to launch it again next year.

- Currently, less than 50% of outlets are open for the company. At the domestic level, UP is the largest selling state for the company.

- The company is now looking to focus its marketing efforts towards home consumption and larger pack size.

- The company has shut down a small unprofitable plant in Bargarh Odisha.

Analyst’s View

Varun Beverages have been one of the biggest bottlers in India and has been quite proactive in international expansion for some time now. The company has seen a major decline in the quarter with a massive fall in on-the-go consumption. The lockdown has hit the company’s sales hard but demand seems to have stayed resilient as in-home consumption has risen along with juice consumption. It remains to be seen whether there is a further economic disruption in the future from COVID-19 which may have severe second-order effects on the company’s performance. Nonetheless, given the resilient sales network, the rising demand for the company’s products, and the arrival of the peak season for the beverages industry, Varun Beverages is a good consumption stock to watch out for at present. However, as it is a capital intensive business, the current pandemic can put a strain on the Balance Sheet which is already laden with debt. The valuation at current levels does not give any margin of safety at the moment.

Q1 CY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Mar CY21 | Mar CY20 | YoY % | Dec CY20 | QoQ % | |

| Sales | 1344.2 | 1000 | 34.42% | 894.7 | 50.24% |

| PBT | 5 | 77 | -93.51% | -78.8 | 106.35% |

| PAT | 76.9 | 55.4 | 38.81% | -54 | 242.41% |

| Consolidated Financials (In Crs) | |||||

| Mar CY21 | Mar CY20 | YoY % | Dec CY20 | QoQ % | |

| Sales | 1724.5 | 1382 | 24.78% | 1275.5 | 35.20% |

| PBT | 7.8 | 62.5 | -87.52% | -64.2 | 112.15% |

| PAT | 60 | 40 | 50.00% | -53.95 | 211.21% |

Detailed Results

-

- The current quarter was very good for the company with 25% YoY growth in consolidated revenues.

- Consolidated Profits were excellent with over 50% YoY growth.

- The company saw an EBITDA growth of 24% YoY and volume growth of 26% YoY in the quarter.

- Organic volume growth in India declined by 13.7% due to disruption caused by COVID-19 in the last 10 days of March. The company saw organic volume growth 14% and 42% in Jan and Feb respectively.

- A consolidated organic volume decline of 9.3%. Realization per case came down 2.3% due to lower sales realization in Zimbabwe in USD terms.

- CSD accounted for 67%, Juices 7%, and packaged water was 26% of total sales volumes.

- EBITDA margins improved by 11 bps YoY as savings in material costs were offset by higher fixed costs amid low sales in the last 10 days of March.

- Depreciation increased 36.4% YoY due to the consolidation of the South and West India sub-territories.

- Finance costs also rose 47.3% YoY as the acquisition of the South and West India territories was funded through debt.

- The company reported exceptional items of Rs 66.5 Cr which represents provision for impairment in the value of certain plant and equipment, glass bottles & plastic shells.

Investor Conference Call Highlights

- The management has stated that the company is focusing on preserving the interests of all stakeholders and shoring up cash flows for the disruptive times ahead.

- The company has built up an additional stock of inventory in March in anticipation of disruption in industrial and manufacturing activities.

- The management is confident of good growth post the lockdown period.

- The management has mentioned that the plant shutdown was only till 20th April and operations with reduced shifts have started in all manufacturing facilities for the company.

- The company is witnessing good demand as sales are going up for the company in April.

- The company has less than 10% of sales from institutional clients, all of which have gone to 0.

- The management has stated that margins should suffer in the coming quarter mainly due to high fixed costs and low volumes on account of the lockdown.