About the Company

Security & Intelligence Serv.(India)is directly and indirectly engaged in rendering security and related services consisting of manned guarding, training, and indirectly engaged in paramedic and emergency response services; loss prevention, asset protection and mobile patrols; facility management services consisting of cleaning, housekeeping and pest control management services in the areas of facility management; cash logistics services consisting of cash-in-transit, ATM cash replenishment activities and secure transportation of precious items and bullion; and alarm monitoring and response services consisting of trading and installation of electronic security devices and systems through its subsidiaries, joint ventures and associates.

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results

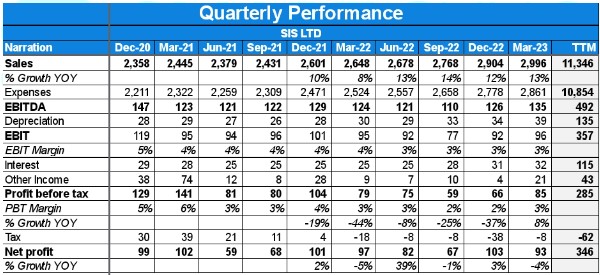

- SIS Limited reported strong revenue growth, with consolidated revenues growing by almost 13% in FY ’23.

- EBITDA margins increased by 50 basis points over the last two quarters, and earnings per share for FY ’23 were 7.1% higher than FY ’22.

- The company generated strong cash flow and reduced net debt-to-EBITDA ratio from 2.06x to 1.75x.

- International business was flat, but compensated for one-time COVID-related contracts falling off

- Consolidated OCF-to-EBITDA for the quarter at 144%, allowing the company to repay INR 83 crore of debt subsequent to the quarter end

Investor Conference Call Highlights

- India Security segment grew by almost 20%, facility management grew by 36%, and the cash logistics joint venture grew by 38% over the previous year.

- The focus is on increasing margins, and the trend of margin improvement is expected to continue.

- The company aims to increase market share to 10% in India through organic development over several years and strategic M&A

- Company has a target of 20% YoY growth, 20% return on equity, and >50% OCF EBITDA

- SIS Limited has seen good client additions and increased business from existing clients across all segments.

- The average contract duration is around three years, but the company has long-standing clients who have been with them for 10-20 years.

- SIS Limited aims to increase its market share, currently below 5%, through organic development and strategic acquisitions to achieve a 10% market share in India.

- The security market has grown by around 12-14% in the past year, and SIS has outperformed the market with 20% growth.

- The company benefits from tax advantages under Section 80 JJA of the Income Tax Act, as explained in the earnings note.

- Cash logistics business already delivers 14-15% EBITDA margin.

- The company decided to stay away from the ATM side of the business, focusing on cash logistics in North and East India.

- By operating in low-competition territories, the company has higher market share and greater density on each cash van route, leading to more margins per route per day.

- The international security services business experienced a drop in margins due to the absence of COVID-related contracts.

- Pre-COVID, the international business had 4-4.5% EBITDA margin, and it is expected to stabilize around that level.

- The share of international business in overall revenues and EBITDA is decreasing, which may increase the blended margin of the SIS group.

- The India Security business and India Facility management business are capable of delivering 6%+ EBITDA margin.

- Around 85% of SIS operates in the services sector, with a 5-7% EBITDA margin.

- The Solutions layer includes additional technology and can have EBITDA margins of up to 15%.

- The VProtect business currently has a small monthly invoice value but delivers a 15%+ EBITDA margin.

- The company aims to build up the alarm business to 50,000 connections in the near term.

- The company has acquired a large contract from Vedanta, which includes manpower, drones, mobile app, CCTV-based video surveillance, and AI-based video analytics. This contract is expected to deliver an EBITDA margin of close to 10%.

- The company operates in three layers: solutions, guarding business, and route-based solutions. Route-based solutions, such as cash logistics and pest control, have high gross margins (35-45%) and deliver 20%+ EBITDA margins.

- The company is receiving income tax refunds from the income tax department, as reflected in the positive taxes number in the Q4 cashflow statement.

- Receivables grew by 20% compared to revenue growth of 13%. The increase in receivables includes a GST component, and the delay in payment by certain clients contributed to a higher DSO (Days Sales Outstanding) in March, which decreased in April.

- The company had more than AUD80 million of COVID-related contracts in the previous year, which were not present this year. The aim is to cover the drop-off in COVID revenue through growth in other areas.

- The subsidiary in Singapore, Henderson, has implemented a turnaround strategy and has shown improvement in the bottom line over consecutive quarters. It may take a few more quarters to reach a profitable state.

- FY’23 has been a year of significant growth for SIS. The India security business grew 20%, the FM business grew 36%, and the cash business grew 38% year-on-year. Despite a 10% revenue shrinkage due to lost COVID work in the international business, the overall growth rate was 0.7%.

- SIS has achieved a strong year-end cash position. Despite rising interest rates in Australia, Singapore, and India, the company has recorded record collections. Debt repayment of AUD15 million in Australia was made after 31st March to control interest costs and strengthen the cash position.

- SIS had a debt position of 2x EV/EBITDA, which was considered a red flag. However, the company has successfully reduced it to 1.7 times net-debt EBITDA. The aim is to keep the debt position in check, with a comfort zone around 1, avoiding under-utilization of the balance sheet or crossing the red threshold of over 2.

- While the margins are not at the desired level of 6%, there has been a steady improvement in the last three quarters. Although the incremental improvement may not be significant, it is moving in the right direction. If the growth momentum continues and disruptions are minimal, operating leverage is expected to kick in, stabilizing SG&A and reflecting positively on the EBITDA margin.

Analyst’s View

Overall, FY’23 has been a successful year for SIS, marked by significant growth, strong cash generation, debt reduction, and improving margins. The company is optimistic about future prospects if the growth trajectory continues and disruptions are minimized. The company will be focusing on margins in future and aims to increase market share to 10% in India through organic development over several years and strategic M&A. Given the market leader status of the company in its operating segments of facilities management and security and the promise of an ever-increasing market opportunity due to the infra boom in India, SIS is a critical stock to look for in the security and facility management space.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

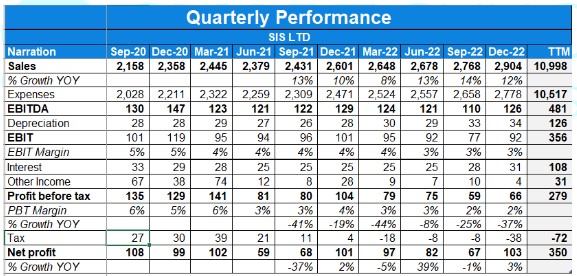

- Consolidated sales grew by 12% YoY & whereas PAT remained flat with 3% growth.

- Security Solutions – India, had a q-o-q increase over Q2 FY23 of 4.6% and a y-o-y increase of 21.0% over Q3 FY22; b. Security Solutions – International, had a q-o-q increase over Q2 FY23 of 5.0% and a y-o-y decrease of 2.2% over Q3 FY22 (6.1 % and -1.2% growth respectively on a constant currency basis); and c. Facility Management Solutions had a q-o-q increase of over Q2 FY23 of 5.5% and a y-o-y increase of 35.2% over Q3 FY22.

- a. Security Solutions – India reported EBITDA of 4.9% which was a q-o-q increase of 50 bps. b. Security Solutions – International reported EBITDA of 4.0% which was a q-o-q increase of 70 bps; and c. Facility Management Solutions reported EBITDA of 4.0% which was a q-o-q decrease of 40 bps.

- EBITDA margins for the quarter were 4.4%.

- OCF to EBIDTA was 1.1%

- Net debt to EBITDA was at 2.06 times in Q3.

- EBITDA for the quarter saw a 2.6% decline YoY.

- The return on Equity for the period is 16.7%.

- The Contribution towards group revenues & EBITDA –

- Security solutions India – 41.4% & 46.2% (EBITDA% @4.9%)

- Security solutions International – 42% & 38.2% (EBITDA% @ 4%)

- Facility management solutions – 17.1% & 15.6% (EBITDA% @ 4%)

- Cash logistics EBITDA% @ 15.2%

Investor Conference Call Highlights

- Currently, only 6% of the company’s customers who are in Security use Facility Management services & the company is taking efforts to increase cross-sell opportunities through a monthly lead exchange program.

- The company’s VProtect business, which does alarm monitoring, has roughly 13,000-plus connections now & has secured another 7,000 connections from banks which will have an EBITDA of 20% plus.

- The management explains that all its contracts have an automatic price escalation clause on a pro-rata basis, although there’s always a time lag as it starts paying first, and then puts up invoices to customers.

- The management when asked about the moat for the biz stated “ this industry does not have barriers to entry. It’s fairly easy for somebody to set up a security company or a facility management company. But the barrier is to scale. And I’ll give you the statistics. There are more than 15,000 licensed private security businesses in India, but only two of them have revenues of more than ₹2,000 crores. Less than 200 of them have revenues of more than ₹200 crores.”

- The company’s moat can be summarized as A) a network of branches serving across 650 districts of the country, B) a very robust supply chain with 14 residential training academies to supply trained manpower across the country at short notice & C) Automated systems to handle 250,000 employees.

- The company’s India security biz has seen a turnaround in performance with EBITDA improving from 3.8% to 4.9% in 3 quarters & the management is confident of clocking 6% in coming quarters.

- No single client contributes more than 1% of total revenues.

- The management states that the company’s past record shows that the company in recession free, & will be able to grow at 2X GDP growth in FY23.

- The company’s bottom line got the benefit of 80JJAA where a deduction is available for hiring new employees.

- The company’s margins in Facility management decreased owing to one-off costs in the current quarter.

- The company expects the net Tax Rate to be Zero owing to deductions.

- The management states that international biz will deliver a low single-digit growth in FY22 which is very decent considering the temporary 50 million worth of temp contracts that exited the system in April making the base very high for FY21.

- The Hendersen biz is reporting losses however, the biz is steadily picking up.

- The lower OCF/EBITDA was a one-off event due to payroll cycle changes.

- The company’s brand operates separately as they cater to the specialized service requirement.

- The company’s cash biz is the second largest in the company & is growing faster than the market leader. The management also sees an opportunity of spinning this segment in the future to create value for shareholders.

- The management maintains that growth is coming despite any major price revisions, & it also expects price revisions to take place which is evident from Gujarat’s latest judgment of a 30% wage hike after a gap of 8 years.

Analyst’s View

SIS is India’s market leader in security, cash logistics, and facilities management. The company saw a mixed quarter with revenues rising almost 13% YoY while profit was almost flat. The management states that it was mainly due to start-up costs undertaken. The company is reporting strong numbers & is expected to clock pre covid margins in the coming quarter. The management is expecting significant market expansion in the future for SIS from the anticipated demand for surveillance in upcoming infra projects and the ongoing construction boom. The company is also looking to expand its target market segments to include IT parks, and malls. The new business line of surveillance setup and maintenance only is also expected to do well in the future. It remains to be seen what obstacles SIS will face during expansion into new segments and whether international growth will come about as expected. Given the market leader status of the company in its operating segments of facilities management and security and the promise of an ever-increasing market opportunity due to the infra boom in India, SIS is a critical stock to look for in the security and facility management space.

Q2 FY23 Updates

Financial Results & Highlights

Detailed Results:

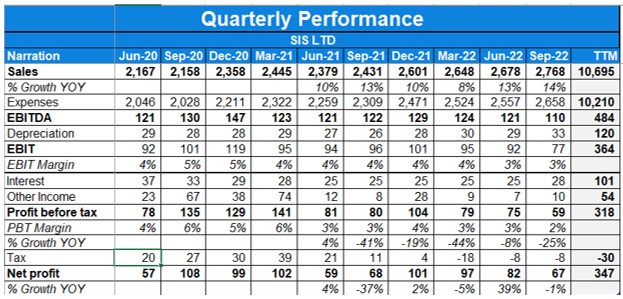

- Consolidated sales grew by 14% YoY & 3.3% QoQ whereas PAT remained flat.

- India business revenue posted organic growth of 21.7% YoY and 8.8% QoQ, Facility Management Solutions business revenue grew by 40.1% YoY and 10.1% QoQ organically, and Cash Logistics Solutions revenue grew by 41.5% YoY and 4.2% QoQ.

- EBIDTA margins for the quarter were 4%.

- OCF to EBIDTA was -27.8%

- Net debt to EBITDA was at 1.7 times in Q2.

- EBITDA for the quarter saw a 10.8% decline YoY.

- Return on Equity for the period is 18%.

- The Contribution towards group revenues & EBIDTA –

- Security solutions India – 41.6% & 46.5% (EBIDTA% @4.4%)

- Security solutions International – 42% & 34.5% (EBIDTA% @ 3.3%)

- Facility management solutions – 17% & 19% (EBIDTA% @ 4.4%)

- Cash logistics EBIDTA% @ 17.2%

Investor Conference Call Highlights:

- The management states that international biz margins were depressed due to reversion back to pre covid levels coupled with an unusually high minimum wage increase of 4.6% in Australia.. However, this impact is a temporary phenomenon as the wage increase gets passed on to clients with a time lag.

- The management further explains that this large wage hike is actually better for the company as it will help boost absolute revenues and earnings when it gets passed out to the client.

- The company is experiencing a sharp growth in facility management biz posts covid due to increased awareness of sanitation & hygiene.

- The margins in the facility management division were lower in the current quarter due to the onboarding of new clients which involves incurring upfront startup costs. The company expects the margins to revert back to 6% EBIDTA post 2-3 quarters from current levels of 4.5%.

- The management states that the opening up of the aviation sector in Australia for private security will be a mega opportunity for the company. It is currently waiting for the regulations to be clarified and additional roles beyond just boarding pass checking to be handed over to private securities before making a formal entry into this segment.

- The management explains that SDS is a strategic acquisition where the company is involved in higher-end services like paramedics and other such health and safety-related services, which are in high demand now in evolved markets like Australia. The company currently has EBIDTA margins of 5% & the management expects this to increase post-integration with SIS.

- In terms of valuations, SDS was acquired at less than 5 times EV/EBIDTA & is currently profitable.

- The company expects that in the Australian division, the new development of a 4.6% wage hike and incremental price hike on select customers, which are relatively lower margins will more than adequately cover up for the revenue gap, which exit of COVID-related contracts have resulted.

- The management states that the company has a very sticky business where the majority of the contract is long-term in nature & gets rolled over ensuring a consistent annuity-like revenue stream.

- The company internally targets OCF/EBIDTA of 50%, ROE of 20% & revenue growth of 20%.

- The company has Rs.20 Crs software & development asset which is used to provide more visibility in terms of cost structure, site profit structure & aid decision-making.

- The management believes that the Indian market will see a wage hike in the coming period due to subdued wage hikes during the covid period, which will affect one quarter negatively but then increase the revenues & earnings positively & also lead to value migration towards organized segments.

- The management states that man-tech solutions are a high-margin business for the company where there is no requirement for manpower. Tender-based contracts have double-digit EBIDTA while negotiated direct contracts have mid-high teen EBIDTA.

- The company’s Hendersen acquisition failed as Covid disrupted its post-acquisition integration plans coupled with the loss of contracts leading to losses. However, the company has 27 million dollars in its purse (which was received from Govt. of Singapore) to rebuild the biz.

Analyst’s View:

SIS is the market leader in security, cash logistics, and facilities management in India. The company saw a mixed quarter with revenues rising almost 14% YoY while profit was almost flat. The management states that it was mainly due to start-up costs undertaken in Q2. The management is expecting significant market expansion in the future for SIS from the anticipated demand for surveillance in upcoming infra projects and the ongoing construction boom. The company is also looking to expand its target market segments to include IT parks, and malls. The new business line of surveillance setup and maintenance only is also expected to do well in the future. It remains to be seen what obstacles SIS will face during expansion into new segments and whether international growth will come about as expected. Given the market leader status of the company in its operating segments of facilities management and security and the promise of an ever-increasing market opportunity due to the infra boom in India, SIS is a critical stock to look for in the security and facility management space.

Q1 FY23 Updates

Financial Results & Highlights

Detailed Results:

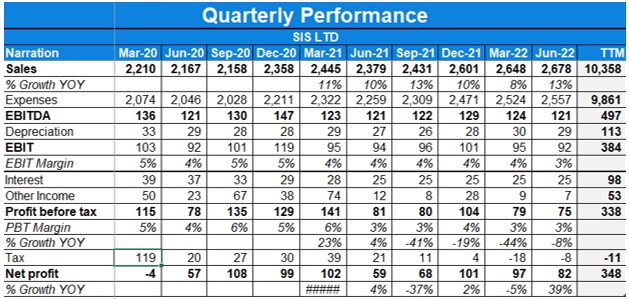

- Consolidated sales grew by 12.6% YoY & 1.1% QoQ whereas PAT remained flat.

- EBIDTA margins for the quarter were 4.5%.

- OCF to EBIDTA was 4.2%

- Net debt to EBITDA was at 1.5 times in Q1.

- EBITDA for the quarter saw a 3% decline QoQ and flat growth on YoY basis.

- Return on Equity for the period is 17.7%.

- The Contribution towards group revenues & EBIDTA –

- Security solutions India – 39.5% & 34.6% (EBIDTA% @4%)

- Security solutions International – 45% & 49.2% (EBIDTA% @ 4.9%)

- Facility management solutions – 15.9% & 16% (EBIDTA% @ 4.5%)

- Cash logistics EBIDTA% @ 14.4% (Highest Ever)

Investor Conference Call Highlights:

- The management states that margins expanded by only 20 Bps due to higher start-up costs.

- The management expects the gross margins to revert to 5.5-6%.

- The management explains that OCF/EBIDTA of 50% is the firm’s target and unlike other companies, the company shouldn’t have a 100% rate otherwise that would mean fewer organic growth opportunities.

- The management is guiding to maintain net debt/ EBIDTA of 1.5× even in coming years since that is beneficial for its ROE metric.

- The company saw 8% QoQ growth in its cash biz & expects this year to be exciting for that segment in terms of revenue growth & margins.

- The management believes that FY23 will be the best year of growth for FM segment in the company’s history.

- The management expects margins in international biz to go back to 4.5% while revenues to stabilize citing the low contribution of covid-related revenue being set off by regular business revival.

- The Australian labor Govt. Have come up with a 4.5% wage hike which will be beneficial to the company’s yield & revenue after 2-3 quarters.

- The company avoids bodyguard services and others such as premium services because of lack of scalability and the personalization requirement being fairly high there.

- The management states that the company is investing in the future of security through various means and also looking to enhance value-added to customers through the use of technology.

- The management doesn’t believe that the manpower element of security will fade despite the growth in security-related technology.

- The company’s acquisition of Hendersen didn’t turn fruitful since it was bought just before covid where the reported margins were very high Vs recent times coupled with the fact that the company is loss-making. However, Management expects to turn around the biz using $25 million surplus cash in the books of hendersen.

Analyst’s View:

SIS is the market leader in security, cash logistics, and facilities management in India. The company saw a mixed quarter with revenues rising almost 12.6% YoY while profit was almost flat. The management states that it was mainly due to start-up costs undertaken in Q1. The management is expecting significant market expansion in the future for SIS from the anticipated demand for surveillance in upcoming infra projects and the ongoing construction boom. The company is also looking to expand its target market segments to include IT parks, and malls. The new business line of surveillance setup and maintenance only is also expected to do well in the future. It remains to be seen what obstacles SIS will face during expansion into new segments and whether international growth will come about as expected. Given the market leader status of the company in its operating segments of facilities management and security and the promise of an ever-increasing market opportunity due to the infra boom in India, SIS is a critical stock to look for in the security and facility management space.

Q4 FY22 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 899 | 780 | 15.3% | 854 | 5.3% | 3381 | 3030 | 11.6% |

| PBT | 13 | 16 | -18.8% | 18 | -27.8% | 115 | 85 | 35.3% |

| PAT | 27 | 7 | 285.7% | 28 | -3.6% | 134 | 57 | 135.1% |

| Consolidated Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 2653 | 2795 | -5.1% | 2628 | 1.0% | 10112 | 9605 | 5.3% |

| PBT | 75 | 416 | -82.0% | 105 | -28.6% | 341 | 758 | -55.0% |

| PAT | 97 | 102 | -4.9% | 100 | -3.0% | 326 | 367 | -11.2% |

Detailed Results:

- Consolidated sales de-grew by 5% YoY & whereas PAT was down 5% YoY (due to impact of deferred tax credit).

- EBIDTA margins for the quarter were 4.7% while operating PAT stood at 3.7%.

- OCF to EBIDTA was 46.9% for FY22.

- Net debt to EBITDA was at 1.4 times in Q4.

- The Australia business saw new deal wins of AUD 25M of annualized value during the quarter.

- The Contribution towards group revenues & EBIDTA –

- Security solutions India – 39.1% & 32% (EBIDTA% @3.8%)

- Security solutions International – 46.7% & 53.9% (EBIDTA% @ 5.8%)

- Facility management solutions – 14.6% & 14% (EBIDTA% @ 4.5%)

- Cash logistics EBIDTA% @ 20% (Highest Ever)

Investor Conference Call Highlights:

- The management states that it is seeing strong volume growth due to the opening up of economies but it is yet to see the rationalization of prices.

- The company won a multi-year contract for the Mahanadi coal field worth Rs.220 Cr.

- The company has created a fund incubator strategy with funds of Rs.75 Cr to invest in new-age startups in security services who are finding valuable & innovative uses of AI.

- The management states that since the average contribution from sectors like IT, hospital etc. range close to 10%, it is not dependent on the growth of any single sector for strong operational performance which can be demonstrated by the growth of 7% even in the Covid-struck year.

- The management states that there is a delta of 12% between EBIDTA & NPM of cash logistics business due to higher depreciation & financing costs being a capex-heavy business.

- The management expects to increase Vprotect’s market share to 2-5% of India’s security market, clock revenue of more than Rs.100 Cr within 2 years & increase connection marks from 10,000 to 15,000.

- The management expects the Facility management business to maintain the highest growth rate in the coming 3 years.

- The management states that FY21 was a completely exceptional year for international business where revenue grew by 20% & EBIDTA margins were close to 6%, however, it expects this segment to taper down to pre-covid levels with single-digit revenue growth & EBIDTA margins closer to 5%.

- The company expects consolidated revenue growth of 20% in FY23.

- The company expects the margin to taper down temporarily in the coming quarter due to high start-up costs for its new Coal project which is the nature of the business.

Analyst’s View:

SIS is the market leader in security, cash logistics, and facilities management in India. The company saw a mixed quarter with revenues decreasing by almost 5% YoY while profit decreased by 5%. The management is expecting significant market expansion in the future for SIS from the anticipated demand for surveillance in upcoming infra projects and the ongoing construction boom. The company is also looking to expand its target market segments to include IT parks, and malls. The new business line of surveillance setup and maintenance only is also expected to do well in the future. It remains to be seen what obstacles SIS will face during expansion into new segments and whether international growth will come about as expected, further high inflation especially in the employee costs can dampen the company’s profitability. Given the market leader status of the company in its operating segments of facilities management and security and the promise of an ever-increasing market opportunity due to the infra boom in India, SIS is a critical stock to look for in the security and facility management space.

Q3 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 854 | 773 | 10.5% | 816 | 4.7% | 2482 | 2250 | 10.3% |

| PBT | 18 | 24 | -25.0% | 13 | 38.5% | 102 | 69 | 47.8% |

| PAT | 28 | 19 | 47.4% | 15 | 86.7% | 107 | 49 | 118.4% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 2629 | 2396 | 9.7% | 2439 | 7.8% | 7459 | 6810 | 9.5% |

| PBT | 104 | 129 | -19.4% | 79 | 31.6% | 265 | 341 | -22.3% |

| PAT | 100 | 99 | 1.0% | 68 | 47.1% | 228 | 265 | -14.0% |

Detailed Results:

- Consolidated sales grew by 10% YoY & 7% QoQ whereas PAT remained flat.

- EBIDTA margins for the quarter were 5.0% (due to one off costs of Rs 5.1 Cr.

- OCF to EBIDTA was 31.6%

- Net debt to EBITDA was at 1.4 times in Q3.

- The Australia business saw new deal wins with monthly revenues of Rs 10 Cr.

- The Contribution towards group revenues & EBIDTA –

- Security solutions India – 38.2% & 32.8% (EBIDTA% @4.3%)

- Security solutions International – 47.9% & 53.6% (EBIDTA% @ 5.6%

- Facility management solutions – 14.1% & 13.6% (EBIDTA% @ 4.8%)

- Cash logistics EBIDTA% @ 12.4% (Highest Ever)

Investor Conference Call Highlights:

- The management states that due to one-off expenses margins of the Facility management business have been below pre-covid however Gross margins are stable & it expects to recover back to 6% margins in the coming quarters.

- The one-off costs in the current quarter were for payment to higher salaried back-office employees who didn’t get any increment in the previous year.

- The management states that the company is the fastest-growing in the industry. Further, since the business is considered as a part of essential services therefore its demand resilience is extremely high, and the company continues to grow in crisis periods just like they grow in growth years albeit at a lower rate.

- Due to a good customer satisfaction rate, the management believes that consolidation will happen which will lead to a shift from unorganized players who have 65% market share towards organized players.

- Ad Hoc business related to covid related quarantine will reduce in Australia which might impact the topline for a few quarters, however, the management believes that due to strong pent up demand from aviation and other sectors which were affected by covid, the revenue will remain stable for the FY23.

- The management believes the tapering down of revenues from the international segment will be covered from recovery in the Indian segment due to demand coming back from railways, IT, IIT & IIM’s & the likes.

- The management states that despite a 6% EBITDA margin this industry can deliver more than 20% return on capital employed and more than 20% return on equity.

- The company is focused to double its market share in security, Facility management & cash logistics in the next three to four years.

- The company’s latest business involves products to protect like an alarm monitoring company, but it does not provide security guards, it provides alarms and does monitoring of customer sites remotely using CCTV footage & that business has crossed 5000 connections this and it is working more to build new technology-based products in its FM business.

- The company closed the P4G New Zealand transaction they acquired the remaining shareholding there where they had a majority shareholding previously & transformed the business from a very small $8 million business to $25- $30 million over a cycle of three years.

- The management states that the company’s guided growth rate of 20% is broken down into three components roughly 7%-8% of roundabout came from minimum wage inflation and the remainder 12% came from existing customer new business and new customer acquisition since in the last two years the minimum wage escalation has completely stalled leading to optically lower growth rate despite increasing customer acquisitions. However, management is confident that wage hikes of 8.5-9% might happen in the future due to pressure on Government leading to better growth.

- SIS is primarily targeting segments like manufacturing, healthcare, and commercial establishments like an I.T park or a mall.

- The management is bullish about the Budget because India’s commitment to spend 5 lakh Crores last year and 7.5 lakh Crores in the current year towards infrastructure creation is a massive opportunity creation because whether it is building a metro or a healthcare establishment or educational establishment or a railway platform everything any kind of infrastructure any kind of square footage that is added is going to need CCTV cameras, security staff, and hygiene and sanitation staff.

Analyst’s View:

SIS is the market leader in security, cash logistics, and facilities management in India. The company saw a mixed quarter with revenues rising almost 10% YoY while profit was almost flat at 1% up YoY. The management states that it was mainly due to one-off costs undertaken in Q3. The management is expecting significant market expansion in the future for SIS from the anticipated demand for surveillance in upcoming infra projects and the ongoing construction boom. The company is also looking to expand its target market segments to include IT parks, and malls. The new business line of surveillance setup and maintenance only is also expected to well in the future. It remains to be seen what obstacles SIS will face during expansion into new segments and whether international growth will come about as expected. Given the market leader status of the company in its operating segments of facilities management and security and the promise of an ever-increasing market opportunity due to the infra boom in India, SIS is a critical stock to look for in the security and facility management space.

Disclaimer

This is not a piece of investment advice. Please read our terms and conditions.