About the Company

Piramal Enterprises Limited (PEL) is one of India’s large diversified companies, with a presence in Healthcare, Healthcare Insights & Analytics business and Financial Services. In Pharmaceuticals, through end-to-end manufacturing capabilities across its manufacturing facilities and a large global distribution network, the company sells a portfolio of niche differentiated pharma products and provides an entire pool of pharma services. In Financial Services, PEL provides comprehensive financing solutions to real estate companies. Healthcare Insights & Analytics business, Decision Resources Group, is the premier provider of healthcare analytics, data & insight products and services to the world’s leading pharma, biotech, and medical technology companies and enables them to make informed business decisions.

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results:

- PAT for the quarter was a loss of INR 196 crores, mainly due to MTM loss on Shriram Investments.

- Profit after tax (PAT) for FY ’23 grew 5% YoY to INR 1,902 crores, excluding exceptional gains from the demerger of the pharma business.

- Capital Adequacy Ratio of 31% on the consolidated balance sheet

- Cash and liquid investments of INR 7,430 Cr (9% of Total Assets)

Investor Conference Call Highlights

- Total assets under management (AUM) for Piramal Enterprises stood at approximately INR 64,000 crores.

- Improved retail and wholesale mix to 50-50 from 33% retail and 67% wholesale in FY ’22.

- Retail AUM grew by 49% YoY to INR 32,144 crores.

- Quarterly disbursements in the retail business grew by 34% QoQ and 361% YoY to INR 6,828 crores.

- Wholesale 1.0 AUM reduced by 33% YoY to INR 29,000 crores.

- Stage 2 and Stage 3 wholesale assets were reduced by 39% QoQ to INR 6,374 crores.

- GNPA ratio reduced to 3.8% in the last quarter of FY ’23 from 4% in the third quarter.

- The company stated that Net interest income for FY ’23 grew 21% YoY to INR 4,176 crores.

- The company stated that the average borrowing cost reduced to 8.6% in FY ’23 from 9.6% in FY ’22.

- Board recommended a dividend of INR 31 per share, subject to shareholders’ approval.

- The retail business focuses on housing loans, secured MSME loans, used car loans, and unsecured loans. Retail lending expansion with 95 new disbursement active branches, serving 515 districts across 26 states.

- The wholesale business focuses on the resolution of Stage 2 and Stage 3 assets through monetization, settlements, enforcement, and portfolio sales.

- The company stated that in the near term, the cost to assets may stay around 3.5% to 4% before gradually decreasing.

- An analyst raises a question about the rationale behind growing wholesale book two while trying to reduce wholesale book one. The chairman explains that the wholesale book consists of different parts. Stage one represents assets with no stress and is seeing organic runoff. The focus is on resolving issues in stage two and stage three, while simultaneously building a more granular and diversified book in the wholesale business.

- Credit cost for the quarter is INR300 crores, with 50-50 split between retail and wholesale segments.

- There was a net loss of INR2,900 crores on recognition, provision reversal of INR2,500 crores, and a gain of INR130 crores on bond buyback.

- SRs (investment instruments) worth INR3,600 crores are held, with no outstanding provisions. 63% haircut and 11% cash recovery have already been achieved.

- The wholesale portfolio under Stage 3 is predominantly focused on real estate (RE), and a significant portion is for under-construction projects.

- The company stated that margins are expected to stay around the current levels, with a potential increase in the cost of funds in Q1 due to repo rate increases. However, rates are expected to stabilize and potentially decline toward the end of the financial year.

- The company stated that the operating margins have been relatively stable around 6.3%.

- The company stated that while there might be a slight upward trajectory in the cost of funds, there is also a slight upward trajectory in yields. Overall, there is no significant concern in this regard.

- The company stated that the credit cost in Q4 was around 1.9%. It is expected that the provisioning cycle for phase one wholesale is completed. Any provisions seen in the future will depend on the growth of the businesses rather than asset quality.

Analyst’s View

Piramal Enterprises Ltd is one of India’s largest diversified companies. Digital loan offerings have powered the company to significantly expand its customer franchise to ~2.6 million with an active customer base of over 1 million, providing it with substantial cross-sell opportunities. As the company continues to make investments in the retail business and continue to expand its branches and staff size, etc., which should continue for another year or so, the OPEX to assets is expected to go up a little. The company continues to get recoveries from old DHFL NPAs. It remains to see how the company performs in the future given the steady rise in inflation.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

- Retail AUM grew 29% year-on-year to Rs. 27,896 crores

- Wholesale 1.0 AUM reduced 20% year-on-year to Rs. 35,101 crores.

- Net profit of Rs. 3,545 crores during the quarter as compared with the net profit of Rs. 888 crores in the same quarter of last year

- Net debt to equity stands at 1.3x with consolidated capital adequacy ratio of 31%.

- Disbursements grew by 593% on a year-on-year basis and 29% on a quarter-on-quarter basis to Rs. 5,111 crores

- Average cost of borrowings improved to 8.4% for the quarter as against 9.1% in Q3 FY22 and 8.8% in the Q2 FY23, despite a rising interest rate environment.

- Cash and cash equivalent is Rs. 6,032 crores at the end of this quarter

- 3% annualized OPEX to assets.

Investor Conference Call Highlights

- The company created a one-time additional provisioning buffer of Rs. 1,073 crores on Stage-1 and Stage-2 assets of the Wholesale 1.0 AUM. With this provision, they have adequately provided toward Wholesale 1.0 AUM, and are in the process of reducing their Wholesale 1.0 AUM in line with their strategy through a combination of various means such as accelerated repayments, settlements, etc.

- The company continued to deliver on its strategic priority of achieving an AUM mix of two-thirds of retail and one-third of wholesale.

- Retail AUM now accounts for 43% of the overall AUM as compared with 33% in the Q3 FY22.

- The company is close to achieving its near-term target of having 50% retail composition of total AUM.

- The key transactions leading to the gains were: 1) Rs. 3,328 crores on account of reversal of an income tax provision, 2) Rs. 1,106 crores on account of restructuring our Shriram Capital Group and bond buyback.

- The company is in the process of reducing its Wholesale 1.0 AUM in line with its strategy through a combination of various means such as accelerated repayments, settlements, etc.

- The company has added 74 new disbursement active branches.

- The company’s target is to serve 1,000 locations through 500 to 600 branches over the next 5 years

- The management states that Nearly 67% of their branches are now selling products beyond just the home loans.

- The management states that the housing and secured MSME loan disbursements grew 387% in the last 12 months and disbursements under the unsecured loan category grew by 46% from the previous quarter and stood at Rs. 2,215 crores during the quarter.

- The company launched 2 new products – Budget Housing in the housing loan category and LAP Plus in the MSME loan category. As there is focus on the Bharat market, they also launched a maiden brand campaign to build the brand – Piramal Finance – in their target segment.

- Digital-embedded finance disbursements grew to Rs. 1,238 crores, contributing to 6% of the AUM in retail.

- The company has received cross-sell disbursements of Rs. 1,862 crores in the last 1 year.

- The company has launched a new innovation hub in Bengaluru to accelerate the development of next-generation lending solutions and analytics.

- The management states that because they changed their stance towards the asset resolution last quarter and sort of consistently executed their resolution strategy, they have seen a significant reduction in the wholesale book.

- The management states that within the new real estate lending business, they have deals worth Rs. 697 crores outstanding as of December 2022. Within the corporate mid-market lending business, they have already built a book of Rs. 1,174 crores diversified across industries.

- The management states that because of the additional buffer that they are taking in Stage-1 and Stage2 assets as well as overall provisioning, our coverage ratio is going up quite significantly across these stages.

- The management states that since it is not a business that is about AUM building this business will always be single-digit percentages of AUM.

- The management states its aim to exit the Shriram Group.

- The interest reversal of the company was Rs. 58 crores during the quarter.

- From 2 years the investors have been experiencing a downhill in returns

- The management states that on the home loan side, on the retail business, over the last 4 to 5 quarters the company has raised interest rates of about 50 basis points on the portfolio and 30 basis points in terms of new originations.

- the management states that their Stage-2 and Stage-3 assets are today lower than what they were in the previous quarter

- the company stated that there is one specific non-real estate sector asset that had moved during the quarter to Stage-3, which had been credit impaired and which has been provided for significantly to the extent of 75-odd percent, which has caused the change in the numbers, as you see, between Stage-2 and Stage-3.

- The management states that About 50% of this business is at roughly Rs. 1 lakh ticket size and greater than 1-year duration. The rest of the business is short-duration small-ticket business.

- The management states that the only increase would be in the form of one resolution that they have done and that too related to some security-related increase.

- The company thinks that the best way to resolve an asset is to actually sell it, and they might get the right opportunity to do that

- The management states that OPEX is very limited to their internal staff, etc. Apart from that, the rest of it is all acquisition costs that we share with the partner. also the company gives the partner a revenue share in the form of origination fee or a skim on the interest based on risk performance of the tranche, etc

Analyst’s View

Piramal Enterprises Ltd is one of India’s largest diversified companies.Digital loan offerings have powered the company to significantly expand their customer franchise to ~2.6 million with an active customer base of over 1 million, providing us with substantial cross-sell opportunities. The business, in the go-to state will likely have run rate credit costs in the 1% to 2% range. Credit cost metrics might look more suppressed because of the heavy level of provisioning that’s there right now and the fact that the wholesale book is degrowing.. The way the economics of this business work is that on a net-net basis, that makes an ROA of upwards of 4% on this business and so it’s a small part of the AUM pie but it makes a very strong ROAs and also gives the company a massive customer base. The company has increased the provisions combined for the stage categories to Rs. 4,600-odd crores from Rs. 4,400-odd crores, which the management believes it adequate for the underlying assets for the time being. There is no expectation for any further provisions or losses to come beyond what they already have provided for, for this category of asset

As the company continues to make investments in the retail business, and continues to expand its branches and staff size, etc., which should continue for another year or so, the OPEX to assets is expected to go up a little. The company continues to get recoveries from old DHFL NPAs.

Q2 FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | |||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | |

| Sales | 476 | 620 | -23.23% | 476 | -0.09% |

| PBT | -200 | 190 | -205.09% | 11,571 | -101.73% |

| PAT | -51 | 150 | -133.62% | 11,549 | -100.44% |

| Consolidated Financials (in Crs) | |||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | |

| Sales | 1,956 | 1,601 | 22.20% | 2,121 | -7.76% |

| PBT | -2,230 | 493 | -552.47% | 8,300 | -126.87% |

| PAT | -1,536 | 426 | -460.25% | 8,155 | -118.84% |

Detailed Results:

- The company’s consolidated revenue grew by 22% and profits fall by around 460% on the YoY basis.

- Wholesale AUM reduced by 13% to Rs. 38,908 crore

- Total AUM has grown 35% from the prior year due to the DHFL merger, and it is now Rs. 63,780 crores

- Retail loans are now 43% of the overall loan book as compared with 12% pre-merger.

- Total provisions as a percentage of wholesale AUM increased to 13.1% from 8.8% last quarter

- There was a net loss of Rs. 1,536 crores during the quarter as compared with Rs. 395 crore of recomputed net profit for the 2nd Quarter of FY’22 for the demerged financial services entity.

- Capital Adequacy Ratio of 23% & Net Debt to Equity ratio of 2 times

- Average cost of borrowings stood at 8.8% for the quarter. 78% of liabilities are fixed in nature.

- This previous quarter the company raised about Rs. 1,000 at about 8.55% average.

- Rs. 360 crores of prudential write-offs was done during the quarter.

- Provision coverage ratio in Stage-3 is 60% at an overall level, and at about 74% to 75% at the wholesale level.

- Retail Business

-

- Retail now already at 43% of the overall loan book, the company is now much closer to stated target of having 50% of total loan book as retail in the near term.

- Average ticket size of nearly 12 lakhs

- Quarterly disbursements grew across all the product categories by eight times year-on-year and 62% quarter-on-quarter to reach Rs. 3,973 crores; ahead of earlier stated guidance of Rs. 2,500 crores to Rs. 3,000 crores by the 3 rd Quarter of FY’23.

- 12% retail AUM growth

- In the one year since the DHFL acquisition, opened 64 new branches and shut down 22 branches resulting in branch network growing to 343 branches.

- Present PAN India across 293 cities and towns in 27 states of India. The company aim to be present at 1,000 locations through 500 to 600 branches over the next five years.

- NonMortgage Loans had a 42% share in our overall retail disbursements.

- Wholesale business

- . 5,888 crores worth of assets moved from Stage-1 to Stage-2

- Exposure to the Top 10 accounts is 33% and reduced since March 19th by Rs. 6,050 crores. And no account exceeds 10% of net worth as of September 2022

- Wholesale AUM has reduced by 13% in the last one year to Rs. 38,908 crores

- Stage-1 loan book is much more granular as the average ticket size of the Stage-1 wholesale book is lower at Rs. 187 crores per loan.

- Over 90% of the Stage-1 wholesale book is into asset backed SPV OPCO loans in real estate.

- Stage-1 book largely excludes Promoter HoldCo. Corporate Lending Transactions. Over 78% of the Stage-1 real estate book is with large and medium developers. And over 60% of the Stage-1 real estate book has limited on low completion risks.

Investor Conference Call Highlights

- Given that this was the first quarter post demerger Rs. 5,888 crores worth of assets were moved from Stage-1 to Stage-2, largely completing the asset recognition cycle. The management believes that the company is now largely well-provided for Stage-2 and Stage-3 assets. An additional provision was created of Rs. 2,255 crores and a fair value loss were taken of Rs. 1,076 crores on our wholesale book during the quarter. The moved assets are largly real estate assets.

- The management stated performance in retail AUM has been driven by various endeavors they took in the last few quarters:

- Addition of new branches

- Adding multiple new products to diversify our retail portfolio

- Activation of branches to sell multiple products.

- Growth in the customer base through the Digital Lending business enabling in cross sell opportunities

- Retail business

- . The company launched multiple new products, now offering 11 retail products

- During the quarter the company has also launched branch led personal loans to salaried individuals in Tier-2 and Tier-3 towns.

- Nearly 82% of our branches are selling products beyond just the Home Loans.

- Hence, not only Housing and Secured MSME loans disbursements grew 5x in the last 12 months. But also, the disbursements under the Non-Mortgage Loan categories have seen much higher traction, though from a low base to Rs. 1,677 during the quarter.

- 20 live partnerships with FinTech, OEMs and aggregators under digital embedded finance business.

- Digital offerings have enabled to significantly expand our customer franchise to 2.2 million, giving the company substantial cross-sell opportunity.

- The company achieved cross sell disbursement of Rs. 945 crores over the last year. The asset quality of the acquired DHFL book remains in line with expectations. The company continues to make recoveries from the POCI book.

- Wholesale business

- . The company will be increasing its focus on recoveries, monetization of the Stage-2 and Stage-3 loans, which will further moderate the wholesale book size in the short term.

- The management believe that this is an opportune time to build the real estate book. Real estate lending is a large market of Rs. 4.5 lakh crores, with supply of credit significantly lower than the demand, offering significant growth potential.

- The management stated From a cyclical perspective, we believe it’s a good time to build up the real estate book as the developer consolidation has resulted in a better-quality ecosystem.

- Within the corporate mid-market lending book, the company has already built a book of Rs. 804 crore with an average ticket size of Rs. 50 crores.

- The management continues to remain committed to FY2027 aspirations, doubling the AUM from FY2022 levels with strong growth in retail disbursement, keeping the net debt to equity 3.5 to 4.5 times.

- Stage-1 part of book is roughly Rs. 27,000 crore in size. The management stated this is very high-quality book. Stage-1 assets are 130 plus odd loans. This is really a granularpart of wholesale portfolio. These assets are well secured in terms of the underlying loan structure and security structures.

- There are three buckets of issues that are there when it comes to moving 5900 crores of assets from Stage-1 to Stage-2. One is where the parent entities of these companies where the group essentially is in some sort of financial distress, while the particular specific project might not be.

- Second category of issues is where a resolution is possible, either through sale or through some sort of other resolution mechanism. But that will come with a little bit of a haircut.

- The third category is where genuinely there have been some amount of movement of the market against the borrower, though they have not really kind of defaulted on payments yet, but their cash flow seem weak.

- The management stated other efforts that are going on is to consolidate and reduce the size of the wholesale book overall over the next few quarters. So, between now and March, certainly the overall books will reduce they expect some of the reduction to come from Stage-2, a little bit from Stage-1 as well.

- Rs. 11,000 crore portfolio in wholesale that is sitting in Stage-2 and Stage-3, and about Rs. 4,400 crores of provision. So, 40% is, the company has covered on that Stage-2 and Stage-3 book.

- Net Rs. 100 crores POCI gains in the quarter.

- The management stated gross yields are not materially different between the accounts on Stage-1 and Stage-2.

- The interest reversal this quarter on account of the movement to Stage2 is around 230 crores.

- Tthe steady state retail book credit cost that the company has is around 1.5% to 2%.

- There two broad sort of connecting themes on retail front

- . Serving what the company call the budget customer of Bharat, that’s the core underlying theme, which says the budget customer of Bharat, what are the various products that the customer might need

- The second, connecting theme is that from a capability standpoint, where the management believe the company is differentiated versus many other competitors are, is on tech and analytics, where the company has a world class team. And given the company’s ability to set up a particular kind of tech architecture and a particular kind of analytic workbenches is significantly different from what even the most tech advanced banks and NBFCs out there are able to do, because they have legacy problems, which Piramal don’t have.

- The management explained for microfinance, in microfinance, a credit person of Piramal sitting in a central location can see a video that the sales RM on the ground is taking of the village or of the hut of the borrower. And as the video is streaming, an AI engine is here, which is reading every image that is coming through and identifying assets that the potential client owns, running it through in ML model, and instantly figuring out what the potential credit rating of that client is and giving that as advice to the credit person sitting in the central office.

Analyst’s View

Piramal Enterprises had a poor Q2 with a 22% YoY rise in revenues however profitability took a deep dive. The company completed a demerger of its pharma business from the financial services business. The company sees real estate financing a segment to watch for the coming future. Moreover, the company is well placed to reduce its wholesale business and make it 50-50 between wholesale and retail in near future. It remains to be seen how long it will take for the new business segments in financial services to scale up for PEL and how it manages their weak assets and their aim to focus on retail business.

Q1 FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY21 | FY22 | YoY% | |

| Sales | 513 | 513 | – | 574 | -10% | 1,825 | 2,226 | 21.9% |

| PBT | 32 | 59 | -45.76% | 361 | -91% | 91 | 641 | 604% |

| PAT | 28 | 53 | -47.16% | 316 | -91% | 40 | 572 | 1330% |

| Consolidated Financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY21 | FY22 | YoY% | |

| Sales | 3,548 | 2,909 | 22% | 4,163 | -14.77% | 12,809 | 13,993 | 9.24% |

| PBT | 644 | 669 | -0.74% | 174 | 270% | 3,456 | 2,510 | -27.3% |

| PAT | 496 | 539 | -7.97% | 109 | 394% | 1,332 | 1,923 | 44.36% |

Detailed Results:

- Revenues have grown by 22% over the previous year in the same quarter and now stand at Rs.3,548 crores. In this, Financial Services grew by 33% year-on-year and Pharma revenues have grown by 9%.

- Net profit stands at Rs.486 crores for this quarter.

- Financial service- AUM grew 37% year-on-year to INR 64,590 crores with retail AUM growing 4.3x year on-year to a high of INR 22,267 crores. The share of retail loans has also increased to 37% from 12% as of June 2021.

- The Pharma business grew 9% delivering revenues of INR 1,485 crores- India Consumer Healthcare and Complex Hospital Generics businesses grew 17% and 10% year-on year, the CDMO business delivered a moderate growth of 8% year-on-year.

- EBITDA margin at 11% during the first quarter versus 12% in the same quarter last year.

Investor Conference Call Highlights

- Management stated that as part of the transformation journey, they have also hired key top-quality senior talent to ensure that they have a best-in-class team to help them build a large diversified Financial Services Company.

- CDMO business had seen subdued growth due to some execution related challenges and changes in order delivery schedules.

- Despite moderate growth in CDMO business, an increase in the raw materials, packaging materials and operating costs.

- The nature of the Pharma business is such that it generates a significant part of profits in the second half of the financial year. Last year, the second half contributed nearly 70% to our profitability.

- Investment that has been done in their CDMO facility at Canada, has given the company about 35% additional capacity and they have got about 1.8 billion tablet capacity at the facility in Pithampur. Management expects that over the next couple of years, they should be able to adequately utilize these capacities.

- Desflurane doesn’t have approval from USFDA yet.

- For non-real estate exposures, only one account valued -INR 100 crores has moved to Stage-3 during the course of this quarter.

- Management is targeting a portfolio composition of ~45% housing, 20-25% MSME, about ~20% unsecured and whatever is left will be the other secured lending products.

- Overall, at an FS-level management believe the kind of business that they are building two-thirds retail, one-thirds wholesale, multiproduct retail with the composition mentioned in point 8. They believe they should be able to deliver a high-2s to low-3s (%) kind of ROA.

- CDMO injectable space over the couple of years CAPEX investments plan for FY23 and FY24 is about $200 million per annum. This would help in creating capacity. This includes expansion of antibody drug conjugate capacities at Grangemouth, high-potent API capacities at Riverview, and they are also looking at increasing capacities for their API facilities in India and for potent injectables at Lexington.

- Management wants to build a diversified book. They are still at the stage where they will experiment with a lot of different products like gold loan, loan against securities etc.

- The wholesale portfolio this quarter from DHFL, all the big lumpy stuff is going to go through a big long process of litigation etc. So, we will keep watching the space.

- In FS, management clarified that they are committed to microfinance business, it’s no longer in experimental mode.

- Being an extremely well-capitalized company with a lot of spare capital available and as a group, they have had a rich tradition of successful M&A. Management would be open to something which is a good product fit and it checks the box on values and valuation.

- POCI book is all retail books where markdown has been done by 65-odd percent to about INR 3,500 crores or thereabouts. If recoveries are greater than the mark, then you get P&L flow. If it’s less than the mark, then you get a P&L hit.

- Incremental embedded yield 12.6% is all disbursements ex of embedded finance and including embedded finance into it, the yield increases to 13.1%.

- At the portfolio level, the average cost of borrowing is 8.8%.

- Capital adequacy is at just over 25%.

- Post the DHFL acquisition mix of retail has gone up from 12% to 37%.

- There is a little bit of seasonality with the Q1 low and the Q4 high, right. But otherwise, our stabilization cost of DHFL etc., fully baked in and settled in this year.

Analyst’s View:

PEL is the flagship company of the Piramal group. The group has presence in diversified businesses like financial services, pharma (CDMO, Critical Care, OTC) and real estate development and consulting (through a separate company). The Board of Directors has eminent persons from the industry providing their experience and governance to the group. Company has experience of lending in the real estate industry for over a decade and forayed into mortgage lending around five years back. Mr. Jairam Sridharan as the Managing Director has been appointed to scale retail finance business in the medium term and is in the process of building team, systems and process to undertake retail book expansion. While DHFL acquisitions have aided their retail book goal. There has been substantial reduction in exposure to the real estate segment in overall loan book and single group exposure of consolidated tangible net worth on a sustained basis which has led to improvement in asset quality. While demerger on track, it would bring in focus in their business. PEL would be an interesting company to keep a track off and look for upcoming updates hereon.

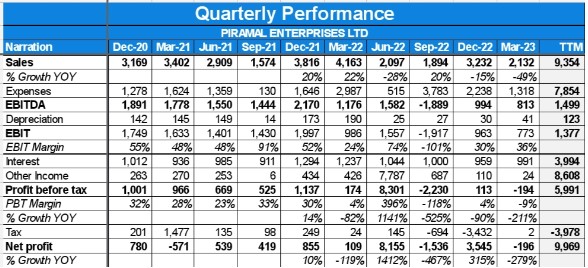

Q4 FY22 Updates

Financial Results & Highlights

| Standalone financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 876 | 517 | 69.4% | 702 | 24.8% | 2693 | 1920 | 40.3% |

| PBT | 360 | 129 | 179.1% | 192 | 87.5% | 651 | 189 | 244.4% |

| PAT | 316 | 78 | 305.1% | 168 | 88.1% | 572 | 40 | 1330.0% |

| Consolidated financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 4401 | 3565 | 23.5% | 4067 | 8.2% | 14713 | 13173 | 11.7% |

| PBT | 174 | 966 | -82.0% | 1137 | -84.7% | 2677 | 3397 | -21.2% |

| PAT | 150 | -510 | -129.4% | 888 | -83.1% | 1999 | 1413 | 41.5% |

Detailed Results

- The company had a very poor quarter with consolidated Revenues for Q4 rising 23% YoY & PAT decreasing by 83% YoY.

- The overall loan book grew by 33% year-on-year to Rs. 65,185 Cr and retail AUM grew four times YoY to AUM of Rs. 21,552 Cr.

- Average cost of borrowings stood at 9.2% while average maturity of borrowings stood at 3.7 years.

- GNPA and NNPA post the merger were at 3.4% and 1.6% respectively with provisioning at 5.7% of AUM.

- Capital adequacy ratio stood at 21%.

- Wholesale: retail loan mix stood at 64:36.

- The loan book breakup after the demerger is:

- Affordable Housing: 68%

- MSME Secured:29%

- Used car loans:0.4%

- Digital unsecured:1.4%

- MSME unsecured:0.7%

- Net debt to equity of the financial services division is now at 2.7 times.

- Cumulative ALM mismatch was positive & stood at Rs.12,237 Cr.

- Self-employed: salaried customers stood at 56:44

- The yield on disbursements was 12.5% while the average cost of funds was at 9.1% in Q4. ROA and ROE were at 1.3% and 4.1% respectively.

- Pharma revenues grew 16% YoY for FY22 7 11% YoY for Q4. EBITDA margins stood at 18% for FY22.

- The breakup of pharma revenues was:

- Pharma CDMO: Up 8% YoY in Q4

- Complex Generics: Up 8% YoY in Q4

- India Consumer Healthcare: Up 55% YoY in Q4

- PEL launched 40 new products in the India Consumer Healthcare division in FY22.

- Demerger is expected to be completed by Q3 FY23.

- The Pharma division contributed to 48% of total sales for FY22.

Investor Conference Call Highlights

- The company has increased its presence with 1 million life-to-date customers and 309 branches across 24 states and union territories.

- The management is aiming to increase its debt to equity to 3.5-4.5X & increase its branch count by 100 in FY23.

- The company invested in EarlySalary (a fintech startup) for a 10% equity stake.

- Through the DHFL acquisition, the company acquired a 50% stake in Pramerica Life Insurance JV with Prudential U.S.

- The management states that the company has $157 million of growth-oriented Capex investments committed across various multiple sites.

- The management states that in the medium to the long term, it expects about 15% revenue growth across the businesses and expects the EBITDA margin to be 25% to 28% in the 3-5 year time frame.

- The company had to make extra provisions because its expected realisation from the sale of a few companies which it had lent in the past was sold at a lower rate.

- Since the take-over of DHFL, the company has recovered Rs.715 Cr worth of loans from the POCI book out of which roughly Rs.425-odd Cr has come in Q4.

- The management is targeting a doubling of AUM post 5 years & shift the loan mix between wholesale: and retail from 65:35 to 35:65.

Analyst’s Views

Piramal Enterprises has seen the continuation of the recovery in the financial division and good growth in the pharma division. PEL had a poor Q4 with a 23% YoY rise in revenues however profitability took a deep dive due to higher provisioning. The company announced a demerger of its pharma business from the financial services business earlier in Q2FY22. This event is expected to take place in Q3 FY2023. PEL continues to invest in adding on to its pharma business. It has acquired a minority stake in Yapan Bio which is expected to help Piramal pharma foray into biologics. It remains to be seen how long it will take for the new business segments in financial services to scale up for PEL and what challenges it will face in the integration of DHFL and the growth path of the pharma business. However, given their past track record, management capability, and surplus unallocated capital which can be deployed to support any of the conglomerate’s various businesses, Piramal Enterprises continues to be a good conglomerate stock to watch out for, particularly in the real-estate lending space.

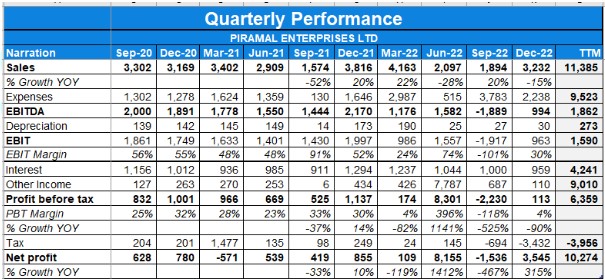

Q3 FY22 Updates

Financial Results & Highlights

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 4067 | 3265 | 24.6% | 3233 | 25.8% | 10312 | 9607 | 7.3% |

| PBT | 954 | 834 | 14.4% | 566 | 68.6% | 2038 | 2198 | -7.3% |

| PAT | 1137 | 1000 | 13.7% | 529 | 114.9% | 2335 | 2489 | -6.2% |

| standalone financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 702 | 586 | 19.8% | 566 | 24.0% | 1817 | 1403 | 29.5% |

| PBT | 192 | 100 | 92.0% | 39 | 392.3% | 291 | 60 | 385.0% |

| PAT | 168 | -164 | -202.4% | 34 | 394.1% | 256 | -38 | -773.7% |

Detailed Results

- The company had a good quarter with consolidated Revenues for Q3 rising 25% YoY & PAT rising 14% YoY.

- The demerger of the pharma and financial services business was approved in Oct.

- PEL acquired a minority stake in Yapan Bio in Q3.

- Shareholders of PEL will get 4 shares of Piramal Pharma post demerger.

- The overall loan book grew by 31% year-on-year to Rs. 60,600 Cr and retail AUM grew four times YoY to AUM of Rs. 21,500 Cr

- The share of retail loans has gone up to 36% post the merger with DHFL. The Aum has increased 42% YoY post the merger. The company now has 301 branches in 24 states and UTs.

- GNPA and NNPA post the merger were at 3.3% and 1.8% respectively with provisioning at 4% of AUM.

- Capital adequacy ratio stood at 26%.

- The loan book breakup after the demerger is:

- Affordable Housing: 46%

- MSME Secured:28%

- Used car loans:2%

- Digital unsecured:21%

- MSME unsecured:3%

- Net debt to equity of the financial services division is now at 2.5 times.

- The yield of DHFL is 11% on disbursements and cost of borrowing being 7%.

- Disbursements in retail book increased 5 times YoY to 735 Cr while disbursement yield stood at 12%.

- The yield on disbursements was 11.4% while the average cost of funds was at 9.1% in Q3. NIM was at 3.5% while the cost to income was at 32% in Q3. ROA and ROE were at 2.6% and 9.5% respectively.

- ROA stood at 2.6% while ROE at 9.5%. Cost to Income ratio stood at 32%

- Pharma revenues grew 15% YoY in Q3 & 18% YoY in 9M. EBITDA increased by 18% YoY and EBITDA margins stood at 22.1%.

- The breakup of pharma revenues was:

- Pharma CDMO: Up 10% YoY in Q3

- Complex Generics: Up 25% YoY in Q3

- India Consumer Healthcare: Up 45% YoY in Q3

- PEL launched 20 new products in the India Consumer Healthcare division in 9M.

- Demerger is expected to be completed by Q3 FY23.

- The Pharma division contributed to 41% of total sales for Q3.

Investor Conference Call Highlights

- The management is expecting a 20% growth in pharma division in FY22 , 15% across the business in coming years with margins reaching to 25-28% levels.

- The management believes covid didn’t impact CDMO biz and the key challenges are in terms of execution.

- The company believes that excluding USA market, ROW is very volatile.

- The CDMO order book increased by 30%.

- Investment in Yapan will help in PEL’s foray in biologics, develop synergies with its existing sites & be a complementary business to CDMO according to the managemen

- Overall collection efficiencies for the retail business have been in the high 90’s.

- Company expects to add 100 new branches in the next 12 months.

- Ebitda margins for the current quarter were higher as compared to H1 due to higher margin business being invoiced in H2 of this FY

- The company is doing significant capex in DIgwal capacity in India which will be the company’s largest facility.

- Logistics, distribution and manpower constraints have affected the execution in CDMO business leading to flat business.

- The company earns 1.6% annualized fees on Rs.20,000 Cr of assets of DHFL which are being managed by the Piramal team for the public sector banks who bought these assets.

- Overall Opex hasn’t changed despite the consolidation with DHFL due to change in manpower to a separate manpower company & cost base of DHFL being lower before merger.

- Incremental cost of funding for the current quarter stood at 8.5%

- The yield in mass affluent space is 10.5-10.75% while affordable housing segment being 12% thus the weighted average being 11.25%

- Tax rate is between 24-25%.

- The margin in the JV with Allergen for Ophthalmology was at 30%.

- The management expects ROA to be in the range of5-3% in future.

Analyst’s Views

Piramal Enterprises has seen the continuation of recovery in the financial division and good growth in the pharma division. PEL had a decent Q3 with 25% YoY rise in revenues. The company announced a demerger of its pharma business from the financial services business. This event is expected to take place in 2022. PEL continues to invest in adding on to its pharma business. It has acquired a minority stake in Yapan Bio which is expected to help Piramal pharma foray into biologics. It remains to be seen how long it will take for the new business segments in financial services to scale up for PEL and what challenges it will face in the integration of DHFL and in the growth path of the pharma business. However, given their past track record, management capability, and surplus unallocated capital which can be deployed to support any of the conglomerate’s various businesses, Piramal Enterprises continues to be a good conglomerate stock to watch out for, particularly in the real-estate lending space.

Q2 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 566 | 434 | 30.4% | 549 | 3.1% | 1115 | 818 | 36.3% |

| PBT | 29 | -31 | -193.5% | 59 | -50.8% | 88 | -40 | -320.0% |

| PAT | 34 | 103 | -67.0% | 53 | -35.8% | 87 | 126 | -31.0% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 3234 | 3339 | -3.1% | 3012 | 7.4% | 6245 | 6342 | -1.5% |

| PBT | 529* | 832 | -36.4% | 669 | -20.9% | 1198* | 1489 | -19.5% |

| PAT | 426 | 628 | -32.2% | 534 | -20.2% | 960 | 1124 | -14.6% |

*Contains exceptional item of loss of Rs 153 Cr

**Contains exceptional item of loss of Rs 168 Cr

Detailed Results

- The company had a down quarter with consolidated Revenues for Q2 falling 3% YoY and PAT was down 32% YoY. Normalized PAT in H1 was almost flat YoY at Rs 1090 Cr.

- The demerger of the pharma and financial services business was approved in Oct.

- The acquisition of DHFL and merger with PCHFL completed in Sep.

- Shareholders of PEL will get 4 shares of Piramal Pharma post demerger.

- Net debt to equity is at 1.3 times currently. Post demerger, PEL (NBFC) will have 1.5 times and PPL will have 0.5 times net debt to equity ratio.

- The share of retail loans has gone up to 33% post the merger with DHFL. The Aum has increased 42% YoY post the merger. The company now has 301 branches in 24 states and UTs.

- GNPA and NNPA post the merger were at 2.9% and 1.5% respectively with provisioning at 4% of AUM.

- The loan book breakup after the merger is:

- Affordable Housing: 43%

- Mass Affluent Housing: 32%

- Loan Against Property: 15%

- SME: 9%

- Secured Business Loan: 1%

- Others: 2%

- 51% of retail customers are self-employed while the rest 49% are salaried. The retail loan book had an average ticket size of Rs 16 Lacs in Q2.

- Net debt to equity of financial services division is now at 2.7 times.

- Retail Lending Portfolio expanded to 9 products.

- The fresh disbursement yield in Q2 was at 11.7%.

- The revenue drop in Financial Services was at 20% YoY in Q2 & 19% YoY in H1. This division accounted for 48% of total revenues in Q2 and 50% in H1.

- The average yield on loans was at 13.6% while the average cost of funds was at 9.5% in Q2. NIM was at 4.3% while the cost to income was at 35% in Q2. ROA and ROE were at 2.7% and 7.1% respectively.

- Pharma revenues grew 13% YoY in Q2 & 20% YoY in H1. This division accounted for 52% of total revenues in Q2 and 50% in H1.

- The breakup of pharma revenues was:

- Pharma CDMO: Up 7% YoY in Q2 & 11% YoY in H1

- Complex Generics: Up 14% YoY in Q2 & 26% YoY in H1

- India Consumer Healthcare: Up 40% YoY in Q2 & 54% YoY in H1

- PEL added 3 large orders for >$10 million each in H1.

- PEL launched 6 new products in the India Consumer Products division in H1. It also launched a new brand CIR in the Geriatric Care segment.

Investor Conference Call Highlights

- The gross loan book of DHFL was at Rs 44,000 Cr excluding any fraudulent assets and PEL was able to get it for a net outlay of Rs 20,000 Cr.

- Organic retail lending disbursements grew 2.6 times QoQ.

- The management expects the EBITDA margin of the pharma business to improve going forward as historically H2 has had better margins than H1.

- The CDMO order book grew 50% YoY.

- Of the Rs 20,000 Cr DHFL net loan book, Rs 18,500 Cr are from retail assets while the rest is from wholesale assets.

- The management states that AUM growth will slow down probably as the whole loan book of the merged entity will be put through the company risk management and other policies for complete amalgamation.

- The overall restructuring in the book will at 2% only.

- The company is not in any hurry to sell off the Shriram stake and it will do so only at desirable levels.

- The rise in goodwill in the balance sheet is from the Hemmo acquisition.

- The transition costs reported on the PL statement is including both DHFL and Hemmo transactions.

- The management has firm belief that disbursements will rise fast in the near future given the network that the company has gotten from DHFL.

- The company will maintain unsecured lending at around no more than 20% of the overall portfolio according to the management.

- The management states that it will take a few months for disbursements to over come the new level of repayments.

- In complex hospital generics in USA, the company is seeing good recovery in the inhalation anaesthesia portfolio.

- The average yield of the DHFL book is at 11%.

- The management expects Pharma business margin in FY22 to be close to FY21 level at near 20%.

- In the CDMO business, 75% of business is in the commercial and manufacturing side while 25% is in the development side including 3% from drug discovery.

- Of the commercial side, 55% is from generics and 45% is from innovator molecules.

- FY22 margin for the pharma business should be a little lower than last year margins due to rise in input materials, logistics and distribution costs.

Analyst’s Views

Piramal Enterprises has seen the continuation of recovery in the financial division and good growth in the pharma division. PEL had a mildly down Q2 with the decline in the financial services business mitigated by the rise in the pharma business while costs rose due to transition charges for the merger with DHFL and Hemmo acquisition. The company’s DHFL merger is complete and has resulted in 42% rise in AUM. The management aims to grow disbursement a lot from current levels with the help of the expanded network gotten from DHFL. The management maintains an optimistic stance on the retail lending platform and the pharma business. The pharma business has seen EBITDA margins fall in H1 but the management is confident that overall margins for the year will be close to last year levels of 20%. The company has also announced that it will be demerging the pharma and financial services business within the next 12 months. It remains to be seen how long this slow period for financial services will last for the company and what challenges will it face in establishing its retail lending platform and the integration of DHFL. However, given their past track record, management capability, and surplus unallocated capital which can be deployed to support any of the conglomerate’s various businesses, Piramal Enterprises continues to be a good conglomerate stock to watch out for, particularly in the real-estate lending space.

Q1 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 549 | 384 | 42.97% | 517 | 6.19% |

| PBT | 59 | -9 | 755.56% | 129 | -54.26% |

| PAT | 53 | -8 | 762.50% | 79 | -32.91% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 3012 | 3003 | 0.30% | 3566 | -15.54% |

| PBT | 669 | 657 | 2% | 966 | -30.75% |

| PAT | 534 | 496 | 8% | -510* | -204.71% |

*Contains tax adjustment of Rs 1258 Cr for earlier years

Detailed Results

- The company had a flat quarter with consolidated Revenues for Q1 rising 0.3% YoY and PAT was up 8% YoY.

- The NCLT approval for DHFL acquisition was done in June.

- Net debt to equity has fallen to 0.8 times.

- The company has unallocated equity of Rs 11,350 Cr which is 32% of overall equity.

- The wholesale loan book in the Financial Services segment accounted for 88% of total loan AUM. It went down to Rs 37,597 Cr in Q1. Now PEL has no single borrower exposure >15% of AUM.

- Retail Lending Portfolio expanded to 7 products and to 40 locations.

- The fresh disbursement yield in Q1 was at 11.9%.

- GNPA at 4.3% with provisioning at 5.8% of the total loan book. NNPA was at 2.2%.

- CAR was at 39% in Q1 vs 34% in Q4FY21.

- The revenue drop in Financial Services was at 19% YoY in Q1. This division accounted for 53% of total revenues in Q1.

- The average yield on loans was at 13.4% while the average cost of funds was at 10.1% in Q1. NIM was at 4.5% while the cost to income was at 33% in Q1. ROA and ROE were at 2.6% and 6.7% respectively.

- Pharma revenues grew 31% YoY in Q1. This division accounted for 47% of total revenues in Q1.

- The breakup of pharma revenues was:

- Pharma CDMO: Up 17% YoY in Q1

- Complex Generics: Up 43% YoY in Q1

- India Consumer Healthcare: Up 73% YoY in Q1

- PEL added 2 large orders for >$10 million each in Q1. It also completed the acquisition of Hemmo Pharma.

- PEL gained market share in complex health generics in major markets.

- PEL launched 4 new products in the India Consumer Products division. It also launched a COVID home detection kit in July.

Investor Conference Call Highlights

- The company raised Rs 804 Cr from its first public bond issue in July.

- The DHFL acquisition is expected to help the retail AUM grow 5x after the transaction.

- The average ticket size for secured loans has come down to Rs 20 Lacs from Rs 75 Lacs before due to the addition of new products. Digital unsecured lending accounts for only 6% of new originations.

- After the DHFL transaction is completed, the leverage in the financial services business will rise to 2.5 times from the current 1.6.

- Developer collections remained at an average level of 85-90%.

- Retail loan collections were affected in April and May but they bounced back to 96% in June.

- The company is planning to do a few more acquisitions in the next 2-3 years.

- The Piramal Capital & Housing Finance Company will be merging with DHFL and become a subsidiary of PEL.

- The assets of DHFL will be recorded at fair value of around Rs 60,000-70,000 Cr no matter what the carrying value.

- The company does not have any exclusive partnerships with fintech players, and it is mostly using the tech-based APIs for seamless integration and experience for the end customer.

- The company will be looking to merge Hemmo Pharma with Piramal Pharma in the future.

- Of the 2 large orders won in Q1, 1 will be fully delivered in FY22 and while the other will be delivered in part in FY22 and FY23.

- The deposit-taking license of DHFL is still existing and PEL will get back to the RBI on how to start taking deposits on this license once the acquisition is done.

- The company does have plans to cross-sell its other products to the customer base of DHFL. The management is confident of selling some of the small ticket unsecured loans to DHFL customers as early as Q1 post-integration.

- After the integration, the loan is expected to become heavily dependent on home loans with an 80% share of the loan book. The digital unsecured lending will be at the remaining 20%.

- The company has also tied up with 2 used car online platforms for its newest used car financing loan product.

- NIMs should be maintained at current levels going forward according to the management.

- The cost of borrowing is expected to drop to 9.2-9.3% after the DHFL transaction.

- The margin seasonality in the pharma business arises from seasonality in the CDMO business which has more projects or orders in the second half of the year.

- The company is aiming to expand to nearly 1000 centers in the next 3-4 years even after getting 300+ from DHFL post-acquisition. The expansion will be mostly in Tier 2, 3 & 4 cities with Tier 1 cities having the least share.

- The company had done restructuring of 2 accounts. One was in real estate with a consideration of Rs 158 Cr and the other was Mytrah Energy which was around Rs 1062 Cr.

- The overall margin profile of Hemmo Pharma will be greater than the overall pharma margin.

- In the case of a separate listing of Piramal Pharma, existing shareholders of PEL will also get shares of Piramal Pharma.

- The digital unsecured lending business has an average ticket size of Rs 17,000 with a duration of 6-12 months.

- The company is looking to concentrate on the 2 main businesses of secured home loans and unsecured digital lending.

- The non-compete agreement with Abbott was over in 2018 and the company is evaluating opportunities to enter the domestic formulations space.

Analyst’s Views

Piramal Enterprises has seen the continuation of recovery in the financial division and good growth in the pharma division. PEL had a flat growth in Q1 with the decline in the financial services business mitigated by the rise in the pharma business. The company’s DHFL bid has gotten NCLT approval in Q1. It has also brought the net debt to equity for overall business to 0.8 but this is expected to rise after the DHFL acquisition is completed. The management maintains an optimistic stance on the retail lending platform and the pharma business. The pharma business has seen EBITDA margins fall due to seasonality factor in the CDMO business. The company is also looking to do a few more acquisitions in the pharma space. It remains to be seen how long this slow period for financial services will last for the company and what challenges will it face in establishing its retail lending platform and the integration of DHFL. However, given their past track record, management capability, and surplus unallocated capital which can be deployed to support any of the conglomerate’s various businesses, Piramal Enterprises continues to be a good conglomerate stock to watch out for, particularly in the real-estate lending space.

Q4 FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 517 | 569 | -9.14% | 586 | -11.77% | 1920 | 2678 | -28.30% |

| PBT | 129 | -237 | 154.43% | -158 | -181.65% | -69 | 276 | -125.00% |

| PAT | 79 | -605 | 113.06% | -165 | -147.88% | -120 | -115 | -4.35% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 3566 | 3581 | -0.42% | 3265 | 9.22% | 13173 | 13559 | -2.85% |

| PBT | 966 | -1101 | 188% | 1001 | -3.50% | 3456 | 1407 | 145.63% |

| PAT | -510* | -2361** | 78% | 799 | -163.83% | 1413* | -553** | 355.52% |

*Contains tax adjustment of Rs 1258 Cr for earlier years

**Contains tax adjustment of Rs 1758 Cr for earlier years

Detailed Results

- The company had a flat quarter with consolidated Revenues for Q4 falling 0.4% YoY and PAT turning negative due to tax adjustment. Normalized net profit for FY21 was at Rs 2627 Cr which was flat YoY in terms of normalized profit.

- The DHFL acquisition has gotten RBI & CCI approvals already and is awaiting IRDAI approval & NCLT resolution.

- Net debt to equity has fallen to 0.9 times.

- The company has unallocated equity of Rs 11,029 Cr which is 31% of overall equity.

- The wholesale loan book in the Financial Services segment was at Rs 39365 Cr vs Rs 41060 Cr last year.

- Sales of developer clients are now at 115% of Q4 last year.

- GNPA at 4.5% with provisioning at 6.3% of the total loan book. NNPA was at 2.4%.

- CAR was at 37% in Q4 vs 31% last year.

- Net debt to equity for this business was improved to 1.8 times from 2.3 times last year.

- The revenue drop in Financial Services was at 14% YoY in Q4 & 8% YoY in FY21. This division accounted for 55% of total revenues in FY21.

- The company’s multi-product retail lending platform made disbursements of Rs 9270 Cr in Q4 with fresh disbursement yield at 11.9%.

- The average yield on loans was at 14.1% while the average cost of funds was at 8.5% in FY21. NIM was at 5.6% while the cost to income was at 22% in FY21. ROA and ROE were at 3.4% and 10% respectively.

- Pharma revenues grew 19% YoY in Q4 & 7% YoY in FY21. This division accounted for 45% of total revenues in FY21.

- The breakup of pharma revenues was:

- Pharma CDMO: Up 23% YoY in Q4 & 15% in FY21

- Complex Generics: Up 1% YoY in Q4 & Down 10% in FY21

- India Consumer Healthcare: Up 55% YoY in Q4 & 20% in FY21

- EBITDA margin in the Pharma division was at 22% in FY21.

- Pharma revenues were in the ratio of 62% B2B & 38% B2C.

- Added 50+ customers in FY21 in CDMO business.

- Gained market share in complex health generics in major markets.

- Launched 15+ products and 35+ SKUs in FY21 in the India Consumer Products division.

- Announced Hemmo acquisition for INR 775 Cr which is One of the few pure play peptide API manufacturers globally with 75% export sales.

- The Board announced a dividend of Rs 33 per share.

Investor Conference Call Highlights

- PEL holds around Rs 7,000 Cr of cash and cash equivalents as of March 31st, 2021.

- The company is aiming to become a 50% retail lending NBFC from the current level of 12% in retail lending contribution.

- PEL is now the largest Sevoflurane supplier in the U.S. for the third and fourth quarter of FY ’21.

- The new acquisition Hemmo has a higher EBITDA margin than PEL’s 22% and is expected to grow 3x or more in the next few years according to the company projections.

- PEL is now getting ready for demerging into 2 large listed entities in the financial sense and pharma sector.

- NIM has come down due to the rise of the retail book as retail NIMs are lower than Wholesale NIMs at present.

- The management expects the proceedings in NCLT for the DHFL acquisition to be over in the next 2 months.

- The management has stated that the company has enough capital to grow at 25% for the next 4-5 years.

- The company made a reversal of Rs 75 Cr of interest on interest which was also another factor that contributed to lower NIM.

- In the case of the Omkar transaction, PEL has taken over the development rights of 67 lakh square feet. It has yet to decide on doing either the joint development or selling of the development rights.

- In partnering with fintechs, the company only allows the partners to apply a gating criterion to filter the applicants and does the underwriting for these filtered applicants by itself.

- The collections from customers in April were at Rs 750 Cr which was in line with normal COVID levels. Out of this Rs 75 Cr only Rs 25 Cr was from new sales and the rest was from old sales locked up in receivables.

- May is expected to see a dip in construction activity of 20-25%.

- The management maintains that the current provisions are adequate to ride out the 2nd wave of COVID-19.

- The management has provided long-term guidance of a 15% growth rate in the pharma business. It believes that the immediate growth in the business will be greater than the long-term rate.

- EBITDA margin in Q4 was at 285 and the management believe that it can continue to stay high as operating leverage comes into play with the rise in sales of the India Consumer Products division. It can even go higher when the Complex Generics business starts growing again.

- The management expects a capex of $ 90-100 mn per year in the pharma business in the next 2 years. This capex is mainly for the facilities in Canada at Riverview and Grangemouth.

- The management states that it doesn’t need any additional capital to grow both Financial Services & Pharma businesses but the unallocated equity can be used at a later date for any acquisitions in both businesses if the need arises.

- The CDMO business is expected to grow faster than overall pharma business due to the additions of the Sellersvile & Hemmo which should add to growth.

- The Lodha exposure as of March ’21 is at Rs 2637 Cr, of which Rs 1593 Cr is now in SPV with a one-time 1.5x cover of fully ready inventory of apartments. The balance of Rs 1058 Cr is in macro tech developers. Rs 431 Cr has already been prepaid and only Rs 620 Cr of exposure is pending now. The total pending exposure adding to the SPV comes to Rs 2150 Cr which is less than 15% of the total book.

- The total exposure to Omkar was Rs 1300 Cr and the management believes that the value of the underlying land is far greater than the loan amount due.

- In CDMO, commercial revenues are 65% of sales while the rest 35% is from development. The management has pointed out that development used to account for only 10% of revenues and as it is rising, it is also providing new avenues for commercial production.

- The company saw a lot of synergies rising from Hemmo which spurred them to this acquisition. For example, a lot of peptides are injectables, and the company already has a client that gets its APIs from Hemmo and gets it filled at PEL’s Lexington plant.

- The main issue with Hemmo was its limited capacity. PEL came to know that many customers didn’t put orders with Hemmo as it didn’t have enough capacity to service these orders. Once the capacity expansion is completed here, PEL is confident of bagging many orders from existing customers.

Analyst’s View

Piramal Enterprises has seen the continuation of recovery in the financial division and good growth in the pharma division. The company DHFL bid has already gotten CCI & RBI approval & is expected to get NCLT approval soon. It has also brought the net debt to equity for overall business to 0.9 and for Financial Services business to 1.8 times which is exceptional for a predominantly NBFC company. The management maintains that the company has enough capital for organic growth of 20-25% per year for both financial services & pharma divisions. The pharma business has good runway in all 3 segments, especially in the CDMO division with the addition of capacities here throughout the year. It is also expected to see additional demand coming back in the complex generics business which has been subdued due to the postponement of most surgeries due to COVID-19. It remains to be seen how long this slow period for financial services will last for the company and what challenges will it face in establishing its retail lending platform and the integration of DHFL from the ongoing 2nd wave of COVID-19. However, given their past track record, management capability, and surplus unallocated capital which can be deployed to support any of the conglomerate’s various businesses, Piramal Enterprises continues to be a good conglomerate stock to watch out for, particularly in the real-estate lending space.

Q3 FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 586 | 532 | 10.15% | 434 | 35.02% | 1404 | 2109 | -33.43% |

| PBT | -158* | 53 | -398.11% | -31 | -409.68% | -198* | 513 | -138.60% |

| PAT | -165 | -9 | -1733.33% | -26 | -534.62% | -199 | 490 | -140.61% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 3265 | 3411 | -4.28% | 3339 | -2.22% | 9607 | 9979 | -3.73% |

| PBT | 1001 | 898 | 11% | 832 | 20.31% | 2489 | 2509 | -0.80% |

| PAT | 799 | 671 | 19% | 628 | 27.23% | 1923 | 1808 | 6.36% |

*Contains exceptional item of Rs 258 Cr which is transaction cost on transfer of pharma business

Detailed Results

- The company had a mixed quarter with consolidated Revenues for Q3 falling 4% YoY and PAT rising 19% YoY. Similarly, 9M revenues fell 3.7% YoY while PAT rose 6.4% YoY.

- The DHFL acquisition has total consideration of INR 34,250 Cr. –upfront cash component of INR 14,700 Cr. (incl. cash on DHFL’s B/S) and a deferred component (NCDs) of INR 19,550 Cr.

- Net debt to equity has fallen to 0.9 times.

- The company has unallocated equity of Rs 12,375 Cr which is 35% of overall equity.

- The wholesale loan book in the Financial Services segment was at Rs 41060 Cr vs Rs 51436 Cr last year a reduction of 20% YoY.

- Sales of developer clients are now at 82% of Q3 last year.

- GNPA at 3.7% with provisioning at 6.3% of the total loan book. NNPA was at 1.8%.

- CAR was at 37% in Q3 vs 29% last year.

- Net debt to equity for this business was improved to 1.9 times from 2.5 times last year.

- The revenue drop in Financial Services was at 9% YoY. This division accounted for 59% of total revenues.

- The company’s multi-product retail lending platform made disbursements of Rs 3122 Cr since soft launch in Oct.

- The average yield on loans was at 14.6% while the average cost of funds was at 8.4%. NIM was at 6.2% while the cost to income was at 18%. ROA and ROE were at 3.8% and 11.5% respectively.

- Pharma revenues grew 5% YoY. This division accounted for 43% of total revenues.

- The breakup of pharma revenues was:

- Pharma CDMO: Rs 846 Cr (Up 16% YoY)

- Complex Generics: Rs 399 Cr (Down 13% YoY)

- India Consumer Healthcare: Rs 130 Cr (Up 14% YoY)

- EBITDA margin in the Pharma division was at 22%.

- The company passed 17 successful regulatory inspections during 9MFY21.

- Launched 15+ products and 35+ SKUs in 9M in the India Consumer Products division.

- Announced expansion of $32 million in Riverview, Michigan facility.

- PEL also announced acquisition of 49% remaining stake in Convergence Chemicals.

Investor Conference Call Highlights

- The company is aiming to create a lending portfolio where retail will be 50% of the lending book in the near term.

- The company launched 6 new products in the retail lending platform in Q3.

- It is now live in 40 locations.

- The company has gradually pivoted the retail lending business towards mass-affluent and affordable housing with no fresh disbursement in the affluent housing finance business. This is expected to improve profitability.

- The DHFL retail loan portfolio should help in jump-starting the organic retail business and expansion in presence with additional branches and customer reach.

- PEL’s top 10 exposures have reduced 27% since March 2019 from INR 18,400 crores to INR 13,400 crores.

- Only 1 account at 15% of net worth with only 3 accounts greater than 7% of net worth.

- The next aim for transformation for PEL is moving from short-term liabilities to stable long-term borrowings. Around Rs 12,800 Cr of long term, debt was raised in 9MFY21 while CP exposure remains low at Rs 1000 Cr. Thus ALM profile has improved with significant positive gaps in all the buckets.

- In Q3, PEL invoked onetime restructuring for loans worth Rs 1741 Cr accounting for 3.8% of the loan book.

- The fall in complex hospital generics business was due to volatility in the demand of products used in surgeries globally but this is expected to normalize shortly.

- The expansion in the Riverview facility is for additional capacity in potent and non-potent API development and manufacturing.

- The company is successfully moving towards the demerger of the Financial Services and Pharma businesses.

- The management has stated that it does see some upside in the wholesale book of DHFL and is yet to decide on its approach in this area.

- Now that the non-compete clause with Abbott is over, the company is looking to expand its portfolio through the OTC space.

- In the complex generics space, the company has won a few large contracts and 1 very large contract. This business division has seen a W-shaped recovery.

- The management expects that once vaccinations are going full way and things normalize, demand will come back to this business due to the big backlog of surgeries that got delayed due to COVID-19.

- The infra book has been reduced to Rs 2375 Cr as of Dec 2020. The majority of exposures are now 3-5% in the wholesale book.

- The Lodha exposure has come down from Rs 3300 Cr to Rs 2671 Cr. The company has split the deal with Lodha into 2 and has moved all finished inventory into an SPV. By March the total exposure will be near Rs 2500 Cr of which Rs 1000 Cr or less will be Lodha exposure while the rest will be in the SPV.

- The management has stated that the cost of funds has remained high due to high wholesale exposure but it will go down significantly as the DHFL portfolio will get added which has only 6.75% cost of funds.

- The personal loans exercise is still in the experiment phase. The company is looking at a target market with a monthly salary of Rs 25000-50000 for this business.

- The merger with DHFL should be complete by May or June 2021.

- The 4 main business lines in the retail lending side will be mass-affluent housing with margins just under 11%, loan against property with a margin between 11.5-12%, affordable housing with a margin above 12%, and small business secured lending with a margin above 13%. Overall the margin from the new business is expected to be above 11% at the least.

- The company went live with ZestMoney as a partner and has 3 more fintech partnerships lined up.

- The management has clarified that it will be doing floating economics with all partners with the front end of the partners and the back end from PEL.

- The 4 large exposure that the company has restructured are in real estate, hospitality, auto components, and infra.

- The company had 1 large exposure in the auto ancillary space that it let go from Stage 2 to Stage 3. This was done as the management saw that liquidating and selling the assets of the company was a better way to get back money than restructuring it. The company recovered around Rs 436 Cr from this exposure.

- The management expects the ongoing acquisition and expansion in the pharma business to drive margin expansion in the future for the company.

- The outstanding retail loan book is at Rs 5300 Cr currently.

Analyst’s View

Piramal Enterprises is facing the heat of the challenging economic environment and downturn in the real estate sector. The company has seen a good bounce back in the financial division and good growth in the pharma division. The company has managed to make a successful acquisition bid for DHFL which is a shot in the arm for the nascent retail lending business. It has brought the net debt to equity for overall business to 0.9 and for Financial Services business to 1.9 times which is exceptional for a predominantly NBFC company. The company is doing well since the launch of the retail lending platform in Nov. PEL’s pharma business is also expected to see additional demand coming back in the complex generics business which has been subdued due to the postponement of most surgeries due to COVID-19. It remains to be seen how long will this slow period for financial services lasts for the company and what challenges will it face in establishing its retail lending platform and the integration of DHFL. However, given their past track record, management capability, and surplus unallocated capital which can be deployed to support any of the conglomerate’s various businesses, Piramal Enterprises continues to be a good conglomerate stock to watch out for, particularly in the real-estate lending space.

Q2 FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 1119 | 1632 | -31.43% | 856 | 30.72% | 1975 | 2572 | -23.21% |

| PBT | 121 | 646 | -81.27% | 27 | 348.15% | 148 | 546 | -72.89% |

| PAT | 103 | 633 | -83.73% | 23 | 347.83% | 126 | 592 | -78.72% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 3339 | 3316 | 0.69% | 3003 | 11.19% | 6342 | 6568 | -3.44% |

| PBT | 832 | 866 | -3.93% | 657 | 26.64% | 1489 | 1610 | -7.52% |

| PAT | 628 | 551 | 13.97% | 496 | 26.61% | 1124 | 1000 | 12.40% |

Detailed Results

- The company had a good quarter which saw a bounce back from Q1 lows. Consolidated Revenues for Q2 were flat YoY and reported a rise in PAT of 14% YoY.

- The company raised Long-Term Borrowings of Rs 11,500 Cr. during H1.

- Net debt to equity has fallen below 1.

- The overall loan book in the Financial Services segment was at Rs 51522 Cr vs Rs 53055 Cr last year.

- Sales of developer clients are now at 100% of the pre-covid level.

- GNPA at 2.5% with provisioning at 5.9% of the total loan book. NNPA was at 1.6%.

- CAR was at 34% in Q2 vs 27% last year.

- Net debt to equity for this business was improved to 2.1 times from 2.8 times in last year.

- The revenue drop in Financial Services was at 5% YoY. This division accounted for 56% of total revenues.

- The company’s multi-product retail lending platform is to be launched in Nov ’20 and will largely be doing secured lending in FY21. It will start by operating in 4 product categories and 7 variants (Affordable, Mass Affluent Housing, Secured Business loans & LAP)

- The average yield on loans was at 14.8% while the average cost of borrowings was at 10.8%. NIM was at 6.3% while the cost to income was at 17.4%. ROA and ROE were at 3.8% and 12% respectively.

- The company completed the deal with Carlyle Group in Oct ’20.

- Pharma revenues grew 9% YoY. This division accounted for 44% of total revenues.

- The breakup of pharma revenues was:

- Pharma CDMO: Rs 866 Cr (Up 20% YoY)

- Complex Generics: Rs 438 Cr (Down 8% YoY)

- India Consumer Healthcare: Rs 140 Cr (Up 25% YoY)

- EBITDA margin in the Pharma division was at 23%.

- The company passed 4 successful regulatory inspections during Q2FY21.

- Launched 15 products and 38 SKUs in H1 in the Consumer Healthcare division.

- Alternative AUM as of Sep ’20 was at Rs 11,230 bn.

Investor Conference Call Highlights

- The company raised long-term debt of Rs 24,800 Cr in H1.

- The company aims to live with its retail lending platform in Diwali with 4 product categories in 26 towns.

- 93% of pharma revenues come from global clients. The company is always on the lookout for acquisitions that may add strategic value and fit for the company in both the pharma and financial divisions.

- The debt in the pharma division after the Carlyle deal is at Rs 2200-2500 Cr.

- The average yield from the retail finance segment is expected to be lower than the current yield of the financial division and is expected to be at 10-12%. The company has decided to stay out of unsecured lending as long as COVID uncertainties still remain.

- The company had built up cash covers on the overly cautious assumption that there will be zero sales & collections in H1 and Q3 will have 20-30% while Q4 will have 40-50% collections. But in reality, the bounce-back has been much better than expected with sales back at 100% and collections at 82%.

- The company still needs 1 quarter to see whether this bounce back is sustainable or it is just pent up demand that is temporary.

- Prices have not really come down in RE space and collections are lagging sales as builders are giving buyers more time in the payment schedule.

- The average cost of borrowing for the company is expected to continue to go down slowly. The management is hopeful that with the company’s strong balance sheet and the mix changing in favor of retail, it will get the rating to upgrade.

- The company has indeed seen the incremental cost of borrowing come down and it was at 8.5-9.5% in the last 6 months.

- The long term funding of Rs 12,000 Cr raised in H1 is in the range of 3-7 years. The company has also done rollovers of Rs 3000-4000 Cr in the same period.

- There isn’t any particular player that the company considers its direct competitor in all spaces. It sees competition from AU or Aavas and other small finance lenders in the affordable housing business and the small business lending spaces. While in the fintech space, it sees Bajaj Finance as competition.

- The company doesn’t want to compete for head to head with these players and is instead focusing on finding pockets in terms of products, customer segments, and properties where banks are not focused and where it can compete a little bit better on given its cost of the fund structure.

- The company is indeed on the lookout for inorganic opportunities in the fintech space but it is unlikely to acquire in fintech purely for specific core platform capabilities of the targets.

- The management has stated that from a liquidity standpoint, the hospitality and hotel sector might stay under some pressure for the foreseeable future and the company may have to consider restructuring in some cases in these segments. The company will take a call on it in January.

- Around 95-97% of outstanding loans in the standalone balance sheet have been transferred to HFC or to NBFC. The company only has around Rs 1500-1600 Cr of loans left in the standalone balance sheet.

- The management has clarified that it had not taken the decision to exit Shriram to increase liquidity or strengthen its balance sheet. They had taken the decision as they are moving into retail lending which may have direct competition with Shriram. The company is in no urgency to sell this stake and it will let it go only for the right price.

- Stage 3 loans for the company were at Rs 1200 Cr while Stage 2 was at Rs 1200-1300 Cr.

- The company is looking to wait till Q4 at least before considering the reversal of COVID provisions.

- The company has reduced its renewable sector exposure from Rs 3900 Cr to Rs 2800 Cr from June to Sep. This exposure is expected to come even further down as 2 large exposures of ACME and ReNew have gotten refinanced at par with Brookfield in Oct. The management expects that by March ’21, all renewable exposure except Mytrah will be refinanced.

- The refinance deal with Brookfield has given the company additional liquidity of Rs 1500 Cr.

- No fresh lending was done in the wholesale business in Q2.

Analyst’s View