About the Company

PI Industries is in the field of AgriSciences having a strong presence in both the Domestic and Export markets. Founded in 1946, they work with a unique business model across the Agchem value chain from R&D to distribution providing innovative solutions by partnering with the best. Known for the technological capabilities in Chemistry/ Engineering related services and on the other hand, have built leading brands over the last 72 years and connected with more than 84,000 retail points pan India.

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results:

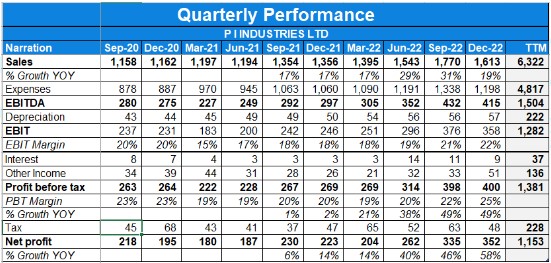

- The company witnessed good revenue growth of 12% YoY in consolidated terms in Q4.

- The profits for the company were up for Q4 with a rise of 37%.

- The EBITDA for the company grew 13% YoY in Q4 and the EBITDA margin rose 7 bps to 22%.

- Gross margins rose by 74 bps to 45% in Q4.

- Overheads increased by 13% YoY in Q4.

- Exports saw a growth of 15% YoY in Q4 while domestic sales increased 1% YoY in the same period.

- The Surplus cash net of debt is Rs. 32,343 million.

- Its order book is at $1.8 billion.

- The Board of Directors has considered a final dividend of Rs. 5.50 per share for FY22-23.

- Improved working capital cycle decreased to 79 days Vs 103 days YoY.

Investor Conference Call Highlights:

- The company’s net working capital management improved significantly with the cash flow from operating activities rising to 3x of FY22 while the trade working capital in terms of number of days of sales reduced to 79 days vis-a-vis 103 days as on 31st March FY22.

- The management talking about its recent acquisition in pharma CDMO & CRO space said “unique ability to build concrete offerings from abstract situations and leveraging our capabilities across the complex chemistries in the value chain and business processes will continue again to create a differentiated value proposition to our stakeholders”.

- In FY23, the domestic business grew at 12% with 8% volume growth and 4% price increase, respectively.

- The Specialty chemical exports from India are slated to scale 10x between 2023 to 2030 in line with the growing consumption in the consumer, agri, and industrial space.

- As per CRISIL, Indian Ag-Chem is slated to grow 10% to 12% in FY24 with exports accounting for 50%

- Talking about the industry prospects, it also said that the China+1 phenomenon and the decline of the EU as a chemical industry powerhouse will support growth for India.

- The management explains that the lower agrochemicals demand in the EU and China as well, but all this is more relevant to the generics and more matured products in the market.

- The company insulates itself from this demand shock as PI is mainly engaged in the early-stage molecules & the demand scenario for such products largely remained unaffected given the inherent nature of its model. It regularly works with partners for the global requirement for their new molecules.

- The management states that “PI’s competitive advantage lies in technological edge, world-class infrastructure ensuring sustainable operations, and enduring relationships with global innovators/large MNCs”.

- The Company is confident to deliver an 18% to 20% growth momentum with better margins in FY24.

- Total capex for FY23 stood at Rs.338.5 Crs.

- The management explains that volume decline in Q4 was a part of the plan as more orders were disbursed in Q1 & Q3, while it has delivered above its guidance for the full year.

- The company is currently not seeing any margin erosion.

- The company’s gross margin was lower by 2.5% due to the change in product mix coupled with higher provisions & one-off charges which are taken at the end of the year.

- The management expects to do capex of close to Rs. 850 crore to Rs. 900 crore in the Ag-Chem business areas in the coming two years, while it is still evaluating the numbers for Pharma business and expects around Rs.10-12Mn capex.

- The management explains that 60% of domestic biz happens in the first half of the financial year while the exports business is evenly skewed.

- The expected tax rate for the coming two years Is 15-16%.

- The company is looking for near-shoring opportunities to get strategic projects coupled with overall supply chain efficiency.

- The nature of capex involves major part towards capacity expansion where it will put two more multi-product plants. The other part of this CAPEX is towards automation, qualitative improvement of these sites, R&D, and other technological upgradation of these plants

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a good performance in Q4 on the back of sustained sales momentum in export markets. It had another decent quarter with 12% sales growth & PAT growth of 37%. It remains to be seen how the company will scale-up its new Pharma acquisitions, what challenges it will face in the 2 new segments of biochemicals and electronic chemicals, and whether the company will be able to match its guidance for growth of 18-20% in all segments despite the turbulent global economic climate. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

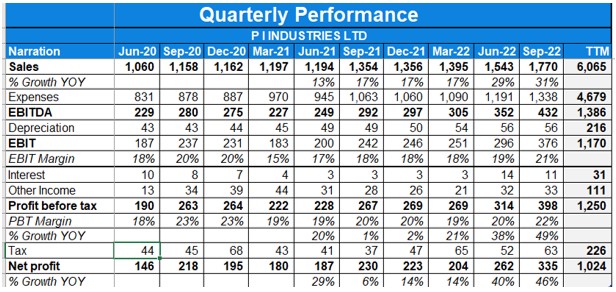

- The company witnessed good revenue growth of 19% YoY in consolidated terms in Q3.

- The profits for the company were up for Q3 with a rise of 58%.

- The EBITDA for the company grew 40% YoY in Q3 and the EBITDA margin rose 400 bps to 26%.

- Gross margins rose by 73 bps to 47% in Q3.

- Overheads increased by 4% YoY in Q3.

- Exports saw a growth of 23% YoY in Q3 while domestic sales increased 2% YoY in the same period.

- The Surplus cash net of debt is Rs. 28,966 million.

- Its order book is at $1.8 billion.

- The Board of Directors has considered an interim dividend of Rs. 4.50 per share for FY22-23.

Investor Conference Call Highlights:

- The institutional sale remained subdued during the quarter due to higher channel inventory and hence reflected in the overall domestic revenue growth.

- Its Branded products for crops including Cotton, Rice, Chili, Horticulture, and Wheat, have performed well coupled with a strong response for its new brands.

- The management states that the company’s ability to engage with global customers on a long-term relationship basis and understanding of complex chemistries are core advantages for the Company and its Customers.

- The share of non-ag chem enquires rose to 25% of the total.

- The company aims to commercialize up to 4 to 5 new molecules each year.

- Exports revenue growth of 23% was driven by volume growth of around 9% and price and currency of around 14%. New innovative Agri brands launched recently also contributed to the growth.

- The gross margin increased by 73 basis points to 47% partially due to cost pass-through and favorable product mix.

- The Trade working capital in terms of Days of Sales was reduced to 90 days vs. 103 days on 31-Mar-22.

- Total CAPEX for 9M FY23 stood at Rs. 2,585 million and the estimated CAPEX for the current year stands at around Rs. 5,000 million.

- The expected Capex for FY24 is Rs. 8,000 million.

- The company expects to maintain its current margins.

- The company’s 12% plus capacity debottlenecking of the existing assets by looking at various engineering and technological solutions helped its growth trajectory.

- The company’s concentration in the Innovators product portfolio has helped it grow despite various headwinds in the generics portfolio across the industry.

- The expected tax rate on a full-year basis should be less than 15%.

- The company has more than 60% of its products under the green category wherein the product under the green category is the one with green Ecoscale and low level of wastage.

- The company plans to commercialize 2-3 non-ag-chem products in the coming FY.

- In terms of growth, the management is still guiding for a 20% plus growth rate on a sustainable basis.

- The other expenses were reduced owing to lower freight costs.

- The company improved its throughput by 10-12% In the current year through technological improvements without doing any major capex leading to better capital efficiency.

- The company has aspirations of getting non-ag chem contribution to close to 20-odd percent in the next 4-5 years.

- The company is in an advanced stage of negotiations for acquiring a pharma company.

- The management while screening molecules chooses only those that have the ability to become sizable by targeting multi-crop pest segments and wider geographies.

- Out of the 15 plants, 3-4 are dedicated plants for which the company has long-term contracts & volumes are pretty high.

- The company expects inventory issues in the coming year from a logistic & channel point of view.

- The management intends to start its Pharma biz with the service in the CRO/CDMO model.

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a good performance in Q3 on the back of sustained sales momentum in export markets. It had another fantastic quarter with 19% sales growth & PAT growth of 58%. It remains to be seen whether PI will be able to find a pharma acquisition opportunity in time to aid the commercialization of products in its new pharma segment, what challenges will it face in the 2 new segments of biochemicals and electronic chemicals, and whether the company will be able to match its medium-term guidance for growth of 20% in all segments despite the turbulent global economic climate. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q2 FY23 Updates

Financial Results & Highlights

Detailed Results:

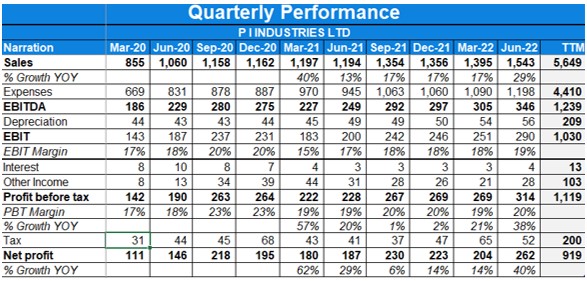

- The company witnessed good revenue growth of 31% YoY in consolidated terms in Q2.

- The profits for the company were up for Q2 with a rise of 46%.

- The EBITDA for the company grew 49% YoY in Q2 and EBITDA margin rose 295 bps to 24%.

- Gross margins rose by 18 bps to 45% in Q2.

- Overheads increased by 16% YoY in Q2.

- Exports saw a growth of 29% YoY in Q2 while domestic sales increased 36% YoY in the same period.

- The Surplus cash net of debt is Rs. 23,211 million.

- Its order book is at $1.8 billion.

Investor Conference Call Highlights:

- The company commercialized one new molecule in non-agro-chem space.

- The export revenue growth of 29% was driven by volume growth of around 25%, coupled with favorable price and currency of around 4%.

- The Domestic revenue growth of 36% was mainly driven by volume growth of approximately 31% and a price increase of around 5%

- The company’s gross margin increased by 18 basis points to 45%, partially due to the cost pass-through and favorable product mix.

- The Total Capex for the half year stood at INR 1,204 million meanwhile the budgeted CAPEX for FY23 is estimated at around INR 6,500 to INR 7,000 million.

- Commercialized products in the last 3 years contribute 16-18% of CSM exports on an annualized basis.

- The management explains that Capex is dependent on technology, efficiency and capacity enhancements, process disruption, and product and chemistries.

- The company doesn’t deal in spot orders.

- The company has 2 SEZ units & it will continue to get the benefits of a low tax rate for at least the next 5 years.

- The management expects to book the current order book revenue in the next 3-4 years timeframe.

- The company is making healthy progress in terms of innovation & IP index, ESG initiatives, increased investments in more complex areas in chemistry & foray into the pharma segment.

- The management states that 4 out of its 11 plants are working on a single product.

- The company launched 5 new products which include- 2 products for horticulture, 1 for wheat, cotton & soyabean each.

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a good performance in Q2 on the back of sustained sales momentum in export markets. PI is already in talks about expanding into biochemical and electronic chemicals spaces. The company is also looking to start a new backward integration project which should help enhance capacity and operational efficiency for PI. It remains to be seen whether PI will be able to find a pharma acquisition opportunity in time to aid the commercialization of products in its new pharma segment, what challenges will it face in the 2 new segments of biochemicals and electronic chemicals, and whether the company will be able to match its medium-term guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q1 FY23 Updates

Financial Results & Highlights

Detailed Results:

- The company witnessed good revenue growth of 29% YoY in consolidated terms in Q1.

- The profits for the company were up for Q1 with a rise of 40%.

- The EBITDA for the company grew 39% YoY in Q1 and EBITDA margin fell 185 bps to 22%.

- Gross margins rose by 8 bps to 44% in Q1.

- Overheads increased by 21% YoY in Q1. This was mainly due to a sharp increase in fuel and related utilities & shipping costs.

- Exports saw a growth of 42% YoY in Q1 while domestic sales increased 4% YoY in the same period.

- The surplus cash net of debt is Rs. 23,116 million. QIP funds remained invested into deposits and debt mutual funds with SLR philosophy while final deployment aligned with PI’s longer-term growth strategy is underway.

- 5 new products are scheduled to be launched in FY23 in the domestic biz while the Commercialization of 7 new molecules is planned in CSM exports.

- During Q1, the company received regulatory approval for 1 insecticide while 1 new product was commercialized for CSM Exports.

- The company has received 13 inquiries received in different stages. Its order book is at $1.4 billion.

Investor Conference Call Highlights:

- The management is confident of delivering revenue growth of 20% with a positive trend in margins.

- The export revenues growth of 42% was driven by volume growth of around 30%, coupled with favorable price and currency of around 12% while the domestic growth of 4% was mainly led by price.

- The company’s change in product mix & partial pass-through helped in increasing GPM by 8 Bps despite the inflationary trends.

- The Inventory levels increased by Rs.1,523 million compared to the previous quarter due to supply chain disruption and to meet customer supply schedules. However, days per sale remain flat at 103 days.

- The management states that in the light of increasing growth visibility, the company has decided to increase its CAPEX plan to Rs.600-650 Crs.

- The company is confident about its growth due to the scale-up of its CSM export products coupled with the launch of new molecules.

- The management states that it won’t be majorly affected by the euro crisis since it is not very dependent on the region for raw materials.

- The management while talking about PI says that “If you were to talk to me 10 years ago, the innovation was not the core idea. Today’s innovation is becoming a Culture at PI, tomorrow it will be led by innovation.”

- The company expects growth in the domestic segment to come from Q2 due to the domestic biz being more reliant on new products for growth & the company is planning to add 6 new products from the second quarter.

- The management states that the three tailwinds are the China Plus One factor, global challenges in manufacturing in the European segment & the cost at which innovation is happening, leading to looking at the return on capital coming from outsourcing.

- The management further explains that While the front end is only growing at a single-digit i.e. the agrochemical industry, the value chain, i.e. manufacturing outsourcing has gone up at twice the rate leading to the confidence of doubling revenues in the next 3-5 years easily.

- The company appointed Mr. Anil Jain who has joined as the Managing Director of Pl Health Sciences and was previously CEO of the global API division of Sun Pharma.

- The management is looking at an effective tax rate of 17.5% in the current fiscal.

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a good performance in Q1 on the back of sustained sales momentum in export markets. PI is already in talks about expanding into biochemical and electronic chemicals spaces. The company is also looking to start a new backward integration project which should help enhance capacity and operational efficiency for PI. It remains to be seen whether PI will be able to find a pharma acquisition opportunity in time to aid the commercialization of products in its new pharma segment, what challenges will it face in the 2 new segments of biochemicals and electronic chemicals, and whether the company will be able to match its medium-term guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q3 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 1327 | 1172 | 13.2% | 1323 | 0.3% | 3807 | 3286 | 15.8% |

| PBT | 258 | 261 | -1.1% | 255 | 1.1% | 732 | 679 | 7.8% |

| PAT | 214 | 194 | 10.3% | 221 | -3.1% | 615 | 530 | 16% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 1382 | 1201 | 15% | 1381 | 0% | 3985 | 3460 | 15.1% |

| PBT | 269 | 263 | 2.2% | 266 | 1.1% | 763 | 716 | 6.5% |

| PAT | 222 | 195 | 13.8% | 229 | -3% | 639 | 558 | 14.5% |

Detailed Results:

- The company witnessed good revenue growth of 15% YoY in consolidated terms in Q3.

- The profits for the company were up for Q3 with a rise of 10% & 13% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 8% YoY in Q3 and EBITDA margin fell 185 bps to 22%.

- Gross margins fell 49 bps to 46% in Q3. This was due to lower export incentives and partial cost pass through.

- Fixed overheads increased by 24% YoY in Q3. This was mainly due to sharp increase in fuel and related utilities, shipping cost and one-time expenses pertaining to strategic projects.

- Exports saw a growth of 19% YoY in Q3 while domestic sales increased 8% YoY in the same period.

- 9M saw revenue and PAT rise of 15% and 14% YoY while EBITDA margin fell 177 bps to 21%. Exports were up 24% YoY while domestic sales were down -3% YoY.

- Surplus Cash net of Debt as on Dec ’21 stood at Rs 2078 Cr. QIP funds remain invested into deposits and debt mutual funds with SLR philosophy while final deployment aligned with PI’s longer term growth strategy is underway.

- 12 new products were launched in 9M which were 1 new insecticide for leaf folder in rice and another was a new fungicide for Sheath blight control.

- 4 new molecules were commercialized this quarter. 3 new molecules planned to be commercialized in Q4.

- One MPP has been commissioned in Q3 and another MPH also got commissioned in Q3.

- PI has signed a technology partnership under joint venture structure in bio-chemical space with a foreign partner. Scale up is expected to start from FY23.

- The acquisition of API & Intermediate business undertaking of ISLL called off amid non-fulfilment of vital CPs, renegotiation of deal.

- The company has received 32 inquiries received in different stages. Its order book is at $1.4 billion.

Investor Conference Call Highlights:

- The company acquired 8 new customers in the 9M period.

- It is also targeting to commercialize 3 more molecules in Q4 bringing the total for FY22 to 8.

- The company has 15-18 products in various stages of development.

- Awkira is expected to increase 3x in the coming year.

- The margin fall was mainly due to increased overheads by 24%, mainly attributed to sharp increase in fuel and other related utilities costs, logistics costs and one-off expenses pertaining to strategic initiatives.

- The management reiterated that it should take 3-5 years for new products to reach peak volumes.

- DSO should remain for nearly 70 days according to the management. The receivable cycle for exports is shorter than that for domestic sales according to the management.

- The management states that despite some patented molecules going off patent will be damaging to sales, it should not have much impact as the innovator molecule will always be at a premium to generic versions and the innovator should also have a big advantage with an optimized cost structure before everyone else.

- The company will be pursuing both organic and inorganic expansion. In organic expansion, it will expand to pharma intermediates while for inorganic expansion, it is open to options.

- The company is looking to launch MMH which is a backward integration strategy providing cost arbitrage and a risk mitigation plan along with some revenues in certain intermediate blocks.

- The company has shown borrowings of Rs 300 Cr on its books which is mainly the ECB facility taken 2 years back and is up for repayment in 3 more years.

- MMH should help increase revenues from both existing and new molecules according to the management.

- Capex done so far in FY22 was Rs 228 Cr and the total for the year is expected to be near Rs 300-350 Cr.

- The capex in coming years is not only expected to increase capacity but also to improve margins for the company according to the management.

- The capex for the backward integration is expected to be at Rs 70 Cr for FY22.

- The company is ideally looking to acquire a pharma company which can deliver Rs 1000 Cr revenues in 3 years time.

- Despite the rise in competition in the industry, the management believes that new product development does require a lot of trust and competencies and is not suitable for the RFQ approach.

- The company has launched PB Knot which is a new product based on pheromones and PI is working with various FPOs and state govts to increase adoption of this product and technology. PB Knot itself is targeted at Pink Bollworm.

- The company has an exclusive license for Asia for PB Knot.

- The management stated that non-agro CSM could rise to 15-20% of the total customer composition in the next 3 years.

- The management also stated that it takes 3-4 years for each new capacity to be fully utilized.

- In CSM, the company is looking to focus on customer stickiness rather than just order book expansion according to the management.

- The company had done price hikes where a partial impact was seen in Q3 revenues and the remaining will be seen in Q4.

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a good performance in Q3 on the back of sustained sales momentum in export markets despite margins being under pressure. The company‘s acquisition of ISLL has gotten terminated and it is looking for new acquisition opportunities. PI is already in talks for expanding into biochemicals and electronic chemicals spaces. The company is also looking to start a new backward integration project which should help enhance capacity and operational efficiency for PI. It remains to be seen whether PI will be able to find a pharma acquisition opportunity in time to aid the commercialization of products in its new pharma segment, what challenges will it face in the 2 new segments of biochemicals and electronic chemicals, and whether the company will be able to match its medium-term guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q2 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 1278 | 1102 | 16.0% | 1133 | 12.8% | 2411 | 2074 | 16.2% |

| PBT | 265 | 250 | 6.0% | 224 | 18.3% | 489 | 423 | 15.6% |

| PAT | 230 | 209 | 10.0% | 184 | 25.0% | 414 | 341 | 21.4% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 1382 | 1191 | 16.0% | 1222 | 13.1% | 2603 | 2260 | 15.2% |

| PBT | 267 | 263 | 1.5% | 228 | 17.1% | 494 | 453 | 9.1% |

| PAT | 230 | 218 | 5.5% | 187 | 23.0% | 417 | 363 | 14.9% |

Detailed Results:

- The company witnessed good revenue growth of 16% YoY in consolidated terms in Q2.

- The profits for the company were up for Q2 with a rise of 10% & 5.5% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 4% YoY in Q2 and EBITDA margin fell 260 bps to 22%.

- Gross margin improved 90 bps to 45% in Q2. This was due to a favourable change in product mix.

- Fixed overheads increased by 38% YoY in Q2. This was mainly due to one-time expenses pertaining to strategic projects and sharp rise in fuel and other utilities.

- Exports saw a growth of 24% YoY in Q2 while domestic sales increase 1% YoY in the same period.

- H1 saw revenue and PAT rise of 15% YoY while EBITDA margin fell 180 bps to 21%. Exports were up 27% YoY while domestic sales were down 7% YoY.

- The company saw operating cash flow of Rs ~208 Cr.

- Surplus Cash net of Debt as on Sep ’21 stood at Rs 2062 Cr (including of QIP proceeds).

- The company completed capacity enhancement of 5% in Q1.

- 2 new products were launched in H1 which were 1 new insecticide for leaf folder in rice and another was a new fungicide for Sheath blight control.

- 6 new molecules planned to be commercialized in FY22, out of which 3 molecules are planned in H2.

- One MPP has commissioned in Q2 and another MPP is planned for commissioning in Q3

- 3 new products were commercialized for exports.

- PI has signed a technology partnership under joint venture structure in bio-chemical space with a foreign partner. Scale up is expected to start from FY23.

- The acquisition of API & Intermediate business undertaking of ISLL called off amid non-fulfilment of vital CPs, renegotiation of deal.

- The company has received >30 inquiries received in different stages. Its order book at >$1.5 billion.

Investor Conference Call Highlights:

- The company had done Rs 168 Cr of capex in H1 and expects to do Rs 105 Cr in H2.

- The management states that the company already has many intermediates at different scale-up levels and these will not require any external facilities to commercialize. The company is looking at other options for acquisition now that the IndSwift transaction has been canceled.

- The management remains committed to delivering 20% of revenues from the pharma segment in the next 4 years. It is even ready to outsource the manufacturing if it doesn’t acquire any new facilities before commercialization.

- The company is looking to pass on most of the price increases to its customers and is determined to preserve its margins.

- The management states that the company incurred non-recurring costs of Rs 10-12 Cr in Q2 which should go away in the future and help in margin appreciation.

- The management expects a capex of Rs 75 Cr for modification of white spaces for the pharma segment on its facilities.

- The domestic market has stayed muted because of continuous rains and supply chain issues.

- The drop in order book is mainly due to the rise in price trends for all inputs and conversion costs which have led to a minor drop in the order book size.

- The company has gone into the manufacturing of electronics chemicals for a leading global player. The company is looking to secure long-term contracts in this space in the next 2 quarters.

- The management states that the electronic chemical opportunity is a small volume, high-value, complex chemistry area. This is another adjacent operating area along with Pharma intermediates that the company is working on.

- The company is also working on the biochemicals side which is also a space where PI is looking to leverage its capabilities in agrochemicals and pharma spaces.

- The company expects to cover 3x the area covered last year by its product Awkira.

- The management guides for a 20% growth visibility in CSM build-up in exports and that PI can reach asset turnover of 2.4-2.5 times in the next 1 year.

- The management does not expect any issues related to land acquisition preventing it from expanding its existing facilities.

- The company is aiming to maintain a capex rate of Rs 300 Cr per year to meet its planned capacity requirements.

- The management maintains that it can reach the same level of capability in pharma CRAMS as it possesses in the Agri CRAMS space, but it will take a lot of time to do so organically and thus the company is looking for an acquisition to expedite this process.

- The management mentioned that there are 2 ways of differentiation in the CRAMS space which are solving supply chain issues or process innovation.

- The management maintains that the primary focus and strategy for the company’s future will remain technological innovation and the advancements in technological capabilities lead to stickier customer relationships.

- The company will continue to go deeper into its core segment of agrichemicals and develop the new verticals of pharma, biochemicals, and electronic chemicals at the same time.

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a good performance in Q2 on the back of sustained sales momentum in export markets despite the domestic revenue decline in H1 so far. The company‘s acquisition of ISLL has gotten terminated and it is looking for new acquisition opportunities. PI is already in talks for expanding into biochemicals and electronic chemicals spaces. The management remains focused on developing the new verticals while pursuing deeper capabilities and innovation in its core agrichemicals segment. It remains to be seen whether PI will be able to find a pharma acquisition opportunity in time to aid the commercialization of products in its new pharma segment, what challenges will it face in the 2 new segments of biochemicals and electronic chemicals, and whether the company will be able to match its medium-term guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q1 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 1133 | 972 | 16.56% | 1162 | -2.50% |

| PBT | 224 | 172 | 30.23% | 224 | 0.00% |

| PAT | 184 | 132 | 39.39% | 182 | 1.10% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 1222 | 1068 | 14.42% | 1241 | -1.53% |

| PBT | 228 | 190 | 20% | 222 | 2.70% |

| PAT | 187 | 146 | 28% | 180 | 3.89% |

Detailed Results:

- The company witnessed decent revenue growth of 14% YoY in consolidated terms in Q1.

- The profits for the company were up for Q1 with a rise of 39% & 28% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 8% YoY in Q1 and EBITDA margin fell 100 bps to 21%.

- Gross margin improved 174 bps to 44% in Q1. This was due to a favourable change in product mix.

- Fixed overheads increased by 26% YoY in Q1. This was mainly due to one-time expenses pertaining to Covid Management and consulting fee and other costs pertaining to other strategic projects.

- Exports saw a growth of 31% YoY in Q1 while domestic sales declined 13% YoY in the same period.

- The company saw operating cash flow of Rs ~250 Cr in Q1.

- Surplus Cash net of Debt as on June ’21 stood at Rs 2193 Cr (including of QIP proceeds).

- The company completed capacity enhancement of 5% in Q1.

- 5 new products were commercialized for exports.

- >30 inquiries received in different stages.

- Order book at >$1.5 billion.

- A new product was launched in Q1 which was a fungicide for Sheath Blight Control.

- Isagro and Jivagro integration completed. Jivagro to introduce 12 co-branded and 2

new products in Q2. - Capacity utilization in Isagro was >80%.

- Completed the acquisition of Ind-Swift Labs Ltd (ISLL) for an all-cash transaction of Rs 1530 Cr. ISLL is involved in making APIs and intermediates. It saw revenues of Rs 857 Cr and EBITDA of Rs 202 Cr in FY21.

Investor Conference Call Highlights:

- The company has 3 new products lined up in Q3 with rice, cotton, and horticulture portfolio.

- Q2 will see a product transitioning to new packaging which should help increase brand recall.

- Gross margin rose by 170 bps due to improved product mix in the domestic business.

- Capex outlay for Q1 was at Rs 71 Cr with a commitment from PI to spend Rs 350 Cr in capex for FY22.

- The management maintains its previous guidance of 15% revenue growth in FY21.

- The primary drivers for the ISLL bid were the company’s regulatory approval, product portfolio, and the pipeline of products in R&D.

- ISLL has most of its business in generics and a very small part in CRAMS. PI will be looking to gradually expand the company into the CRAMS space according to the management.

- The management states that ISLL was going through some financial stress and thus its working capital days were stretched. PI will be looking to normalize the WC days back to optimal levels.

- Although CSM business fell 20% QoQ, it has risen 30% YoY which is a good indicator of the rise of the business segment according to the management.

- The 15% revenue growth guidance is for organic growth of the company excluding ISLL.

- For the 2 innovative molecules in development, the company is looking for partnership opportunities for co-development with global innovators and other parties.

- The company is looking to use the rest of the Rs 500 Cr from the QIP on opportunities involving technology and others that can contribute directly to the company’s organic growth.

- The company is indeed looking to apply a crossover lever to leverage its chemistry tech expertise and apply it to the new pharma platform provided by ISLL.

- The management firmly believes that the addition of ISLL will have major incremental benefits for PI beyond the simple addition of extra sales and profits.

- The company has been hiring top-level talent for the positions available from the exit of the promoter/management of ISLL. It is also looking to develop its in-house talent pool to fill a large part of the open positions.

- The 2 novel molecules are expected to stay in development for the next 4-5 years and thus the company is looking for a partner to share in the development and commercialization of these new products.

- The management explains that the fall in domestic sales for PI was mainly due to the high base last year because of the excess prepurchase done by customers due to the uncertainty arising from the national lockdown.

- The management states that it will take at least 2 more years for a clear picture to emerge on how the company will evolve in the pharma space with ISLL.

- The current utilization level for ISLL is at 70-75% across different blocks.

Analyst’s View:

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a decent performance in Q1 on the back of sustained sales momentum in export markets despite the domestic revenue decline because of the high base last year. The company has completed the acquisition of ISLL which is an API and intermediate manufacturer. PI is looking to combine the acquired and its native technologies for newer opportunities and explore the CSM and CRAMS spaces. The integration and opportunity will take some time to develop since the promoter/management has not been part of the acquisition and thus the company will have to chart out its approach on how ISLL will evolve with the help of PI. It remains to be seen what challenges does PI faces in the integration with ISLL and whether the company will be able to match its medium-term guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q4FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1162 | 801 | 45.07% | 1153 | 0.78% | 4390 | 3355 | 30.85% |

| PBT | 224 | 125 | 79.20% | 263 | -14.83% | 910 | 594 | 53.2% |

| PAT | 182 | 98 | 85.71% | 196 | -7.14% | 719 | 442 | 62.67% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1241 | 862 | 43.97% | 1201 | 3.33% | 4702 | 3415 | 37.69% |

| PBT | 222 | 142 | 56% | 264 | -15.91% | 939 | 614 | 53% |

| PAT | 180 | 111 | 62% | 195 | -7.69% | 738 | 457 | 61.49% |

Detailed Results

- The company witnessed exceptional revenue growth of 44% YoY in consolidated terms in Q4.

- The profits for the company were up for Q4 with a rise of 86% & 62% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 22% YoY in Q4 and EBITDA margin fell 290 bps to 19%.

- Fixed overheads increased by 29% YoY in Q4.

- Exports saw a growth of 47% YoY in Q4 while domestic sales grew 11% YoY in the same period. Isagro grew 51% YoY.

- FY21 Performance was similarly stellar with 38% YoY revenue growth and 61.5% YoY PAT growth.

- Exports saw a growth of 35% YoY in FY21 while domestic sales grew 39% YoY in the same period.

- EBITDA margin in FY21 improved 90 bps to 22%.

- The company saw free cash flow of Rs 303 Cr in FY21.

- Capex for FY21 was at Rs 459 Cr.

- Surplus Cash net of Debt as on March’21 stood at Rs 2070Cr (including of QIP net proceeds of Rs. 1975 Cr)

- 5 new launches planned in FY22 for rice, cotton and horticulture portfolio.

- 5‐6 pipeline molecules at various stages of development to be commercialized in the coming FY22.

- Order book at >$1.5 billion.

- PI announced a final dividend of Rs 2 per share.

Investor Conference Call Highlights

- The market for crop protection chemicals in India is expected to expand at a CAGR of 8% to 10% between the years ’20 to ’25.

- Isagro has now been renamed Jivagro.

- There has been a reduction of 4.7-4.8% in gross margins in Q4. Part of it was due to a change in product mix & part of it was due to the MEIS going away.

- The company is in the advanced stages of its next acquisition and has gotten delayed due to the 2nd wave of COVID-19. It should get clarity by Q1 or the start of Q2.

- The management has assured that the planned acquisitions will be completed within FY22.

- The management has guided for a cautious target of 15% revenue growth. It states that the cautious stance is due to the current COVID situation in the country.

- Barring the loss of margin due to MEIS, the management is confident that the drops are temporary, and the margin will be back at normal levels soon.

- The company will not be doing capex for capacity expansion in FY22 at the same pace as it has done in the past few years. It is now only looking to increase its asset turnover in newer facilities and looking to do major capex only for acquisitions.

- The company is indeed looking out for pharma opportunities where technologies or new units can be used as plug and play or helping the company create a differentiated solution. Its objective for this category remains to scale it up to 20-25% of sales in 3-4 years.

- The newest plant will fully be working by Q2.

- The company is also looking into green chemistry and automated process technologies to increase efficiency and reduce wastage or create safer ways for waste disposal.

- The management has stated that the breakup between long-term contracts and others should be unchanged at 70-30.

- The management maintains that PI has not lost any of its long-term customers to date and is even acquiring new ones beyond the agchem space.

- The few acquisition options that PI is looking at are all with the majority assets in India but with significant sales in exports.

- Of the 5 new launches in FY22, 3 are insecticides. 1 of these is a new molecule while the rest 2 are mixtures for cotton and rice specifically. These mixtures are expected to be released in Q3 or Q4. The last 2 products to be launched will be fungicides with one being a bio fungicide.

- The management expects these new products to do well and contribute to significant growth in the next 2-3 years.

- On the desirable technologies side for acquisition, PI is looking for technological opportunities to combine and leverage both agchem and pharma sides.

- The key driver for the domestic acquisition in the pharma space is the import substitution opportunity in intermediates or APIs where the majority of domestic demand is imported. The driver for international opportunities is to derisk the concentration of operations in Gujarat and to get closer to customer sites.

Analyst’s View

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw another stellar performance in Q4 on the back of sustained sales momentum in both domestic and export markets despite the fall in EBITDA margin. The company is still evaluating options for acquisition. It is specifically looking for acquisition opportunities in the pharma sector to speed up expansion into this sector & where it can combine the acquired and its native technologies for newer opportunities. PI already has clarified that it is looking at options with domestic assets and significant export sales. It remains to be seen whether there are any other disruptions in-store from the expansion into the pharma space and whether the company will be able to match its medium-term guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q3FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 1153 | 870 | 32.53% | 1102 | 4.63% | 3228 | 2554 | 26.39% |

| PBT | 263 | 169 | 55.62% | 250 | 5.20% | 686 | 470 | 45.96% |

| PAT | 196 | 120 | 63.33% | 209 | -6.22% | 537 | 344 | 56.10% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 1201 | 869 | 38.20% | 1191 | 0.84% | 3461 | 2553 | 35.57% |

| PBT | 264 | 170 | 55% | 263 | 0.38% | 716 | 472 | 51.69% |

| PAT | 195 | 121 | 61% | 218 | -10.55% | 559 | 346 | 61.56% |

Detailed Results

- The company witnessed exceptional revenue growth of 38% YoY in consolidated terms in Q3.

- The profits for the company were up for Q3 with a rise of 63% & 61% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 48% YoY in Q3 and EBITDA margin improved 176 bps to 24%.

- Fixed overheads increased by 29% YoY in Q3.

- Exports saw a growth of 40% YoY in Q3 while domestic sales grew 26% YoY in the same period.

- 9M Performance was similarly stellar with 35.6% YoY revenue growth and 61.5% YoY PAT growth.

- Exports saw a growth of 30% YoY in 9M while domestic sales grew 46% YoY in the same period.

- The company saw net cash generation of Rs 301 Cr in 9M period.

- Capex for 9M period was at Rs 320 Cr.

- Completed Integration of Isagro brand molecules with PI.

- Successfully commissioned 4 molecules at the recently acquired Isagro site.

- PI saw the highest ever sales in Nominee herbicide and Osheen insecticide led by rice and cotton crop respectively.

- 5-6 pipeline molecules at various stages of development to be commercialized in the coming FY.

- Another MPP is planned to be made ready by Q4 FY21, thus enhancing the overall capacities.

- The company maintained an order book of > $1.5 billion.

- PI announced an interim dividend of Rs 3 per share.

Investor Conference Call Highlights

- Capacity utilization building has almost come back to the pre-COVID levels.

- The management maintains the growth guidance of 20-25% for the CSM business.

- PI’s residual brand portfolio has seen domestic growth of 17% YoY and Isagro has grown 26% YoY.

- The company currently has 2 options that it is actively evaluating for acquisition.

- The management has stated that PI is ready to commercialize 12-15 new molecules in the next 2 years.

- The pace of commercialization of new molecules has risen in the past 2 years as the R&D pipeline has matured and the flow of new inquiries has gone up.

- The management has stated that the current R&D pipeline will be geared more towards specialty refined chemicals going forward.

- The company has 15 lead scientists in the pharma division and it has 4 PhDs in the leadership team.

- The company is still evaluating opportunities for allocation of the QIP proceeds.

- The management has stated that the company and the whole Agchem sector is expanding slowly in the world and North America remains one of the biggest markets for the industry.

- The management maintains that it has a good pipeline for the next 2 years and any capacity expansion will probably be for some of these new products. Apart from building new capacity, the company is also working on increasing throughput from existing capacity which would increase capital efficiency of existing facilities.

- The management has stated that growth opportunities for PI remain intact but capex intensity may go down as the company uses technology initiatives for capacity expansion. The target is to increase asset turnover above 2 times.

- In a multi-product plant scenario, the management states that the ideal utilization rate should be between 80-85%. The technological initiatives are taken to widen the existing capacity in current plants and bring in room for expansion in utilization back to ideal levels.

- The management states that the order book remaining stable at $1.5 billion should not be a cause for concern as it is constrained by the asset base of the company and as PI gets larger and scalable into products and deep over the relationships, the importance of order book gets declined.

- Although the container shortage issue is seen as a challenge by the management, it doesn’t feel that the shortage will have much impact on operations.

- Employee costs will remain high as the company is looking to attract top talent but the management is comfortable with it.

- The company is also looking to implement digital technologies from IBM for data analysis and processing to generate insights to drive throughput.

- 20% of domestic growth comes from Isagro.

- The company’s plan for the pharma space is to develop APIs and intermediaries to establish its credentials and eventually graduate to the CDMO/CRAMS model.

- The company hopes to highlight its complex chemistry capability and establish cost leadership in less competitive and highly complex products in the pharma space to show its technology as its key differentiator.

- The company has 24-25 products in the commercialization stage and around 40-45 products in the synthesis stage.

- Although valuations in the entire chemicals and pharma industry have gone up, the management remains confident in its acquisition capabilities.

- The share of the export business will continue to remain large as the international market is much bigger than the domestic market.

- The company currently has 15 multi-product plants.

- The primary purpose for the evaluation of the current acquisition opportunities is to be able to expedite the whole process of expanding into the pharma sector without time-consuming activities like getting approvals and passing the regulations for its facilities.

- The company has 3-4 specialty non-agro chemicals and 2-3 agrochemicals in the pipeline currently.

- The utilization level for the 2 new plants is at 80% and below 50% currently. The lower one is expected to come up to 50% soon.

- The management remains confident of sustaining the revenue growth rate of 18-20% in FY22 as well.

- The company has seen the application of Awkira to 1 Lac acres out of an opportunity size of 13 million acres which highlights good room for growth according to the management.

- The management maintains that any acquisition that the company does will be EPS accretive.

- The target for the expansion in specialty chemicals will be additives that will not be in food.

Analyst’s View

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw another stellar performance in Q3 on the back of sustained sales momentum in both domestic and export markets and the completed integration of Isagro. The company is evaluating options on how to use the Rs 2000 Cr through QIP. It is specifically looking for acquisition opportunities in the pharma sector to expedite the process of expansion into this sector. PI already has 2 earmarked opportunities that it is evaluating actively right now. It remains to be seen whether there are any other disruptions in-store from the expansion into the pharma space and whether the company will be able to match its lofty guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q2FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 1102 | 918 | 20.04% | 972 | 13.37% | 2074 | 1684 | 23.16% |

| PBT | 250 | 169 | 47.93% | 172 | 45.35% | 423 | 301 | 40.53% |

| PAT | 209 | 123 | 69.92% | 132 | 58.33% | 341 | 224 | 52.23% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 1191 | 918 | 29.74% | 1068 | 11.52% | 2260 | 1685 | 34.12% |

| PBT | 263 | 169 | 55.62% | 190 | 38.42% | 453 | 302 | 50.00% |

| PAT | 218 | 123 | 77.24% | 146 | 49.32% | 363 | 225 | 61.33% |

Detailed Results

- The company witnessed good revenue growth of 30% YoY in consolidated terms in Q2.

- The profits for the company were up for Q2 with a rise of 70% & 77% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 45% YoY in Q2 and EBITDA margin improved 298 bps to 24%.

- Fixed overheads increased by 20% YoY in Q2.

- Exports saw a growth of 25% YoY in Q2 while domestic sales grew 33% YoY in the same period.

- H1 Performance was similarly stellar with 34% YoY revenue growth and 61% YoY PAT growth.

- Exports saw a growth of 24% YoY in H1 while domestic sales grew 54% YoY in the same period.

- The company now has a surplus cash position of Rs 98 Cr as of 30th June 2020.

- The company saw the highest ever POG of Nominee Gold. It launched Londax Power (insecticide) and Shield (fungicide) in Q2.

- 40+ products at various stages of the R&D pipeline.

- 18 new patent applications were made in H1 including intermediary of COVID-19.

- Continue to supply Pharma intermediates on a commercial scale with more than 10+ pharma products at various development stages in R&D.

- The company maintained an order book of > $1.5 billion.

Investor Conference Call Highlights

- The 2 newly launched brands of Londax Power and Shield are aimed at the rice crop.

- A favourable product mix was responsible for better EBITDA performance during this quarter.

- Isagro has seen good uptake due to fruits, vegetables, and plantations recouping well after the end of the lockdown.

- Isagro’s contribution to the overall consolidated growth of PI has been around 11% in H1.

- The management maintains its earlier guidance of >20% revenue growth in FY21.

- The company has a couple of multiproduct plants are under construction currently. It is also looking to enhance the utilization of growth plans and some possible acquisitions.

- The company is aiming to keep the order book at near current levels of $1.5 billion as it helps maintain revenue visibility for 3-4 years. It is a testament to the company’s growth that despite stellar growth in the past 4 quarters, the order book size has remained nearly the same.

- The company’s objective is to fully deploy the QIP funds in the next 5, 6 quarters.

- The management aims to keep the company growing on the back of its strong technical abilities and its IPs.

- The management has also mentioned that as the company is growing at 30-35%, the operating leverage is getting reflected in an improved EBITDA margin.

- The management is confident that there will be at least 2 to 3 new products that PI plans to launch every year for the next 3 to 5 years. Along with the company’s focus on strengthening the quality of the business from channel management and rising emphasis on digital marketing, the company should be able to keep on expanding on the margins of the domestic business.

- The tax rate for Q2 was at 19.3%.

- The capex plan for FY21 is at Rs 550-600 Cr. Around Rs 100-150 Cr of this is expected to carry over to FY22.

- The MEIS for the company has fallen to Rs 2 Cr in Q2 from Rs 17-18 Cr last year. The company is waiting on the details of the alternative scheme announced by the govt.

- The company is looking at insight opportunities where it can easily deploy INR 3,000 crores which is expected to be generated as cash in the next 18 months and sustainability generates returns better than what it is doing today.

- The MPP getting commissioned this year has gotten delayed due to COVID-19 and is expected to be commissioned by the end of the year or Q1FY22.

- The capex for next year is expected to be around Rs 400-500 Cr.

- The management expects the concentration risk both in terms of customers and in terms of products will be reduced over time. With the diversification into pharma and other specialty chemical areas, this concentration risk will reduce even further.

- The company does not have any current capacities for making the 10 pharma intermediates under R&D and is looking at possible acquisition targets that will help the company address this gap and bypass the requirement of building assets and getting regulatory approval.

- The current demand scenarios are expected to sustain in the medium term at least for the company according to the management.

- Most of the pharma intermediate opportunities for the company lie in already commercialized products. The key technological differentiation the company is aiming at is improving the quality or the cost or other parameters.

- In CSM, the company has commercialized 1 product in Q2 and si aiming to do so for a few products in H2.

- The management is confident that in the next 1 or 2 years, PI will be able to enhance the capacities without really putting in capital.

- Londax Power is actually a product inherited from PI Kumiai, which they had acquired from DuPont. It is an existing brand that has a very strong brand position in certain markets in both South and East of India in the rice crop.

- The shield is an in-house R&D innovation of an existing molecule with a new innovative formulation that has been specifically launched for disease control in rice.

- Both of these products are generic products.

Analyst’s View

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a phenomenal performance in Q2 on the back of normal monsoons, the addition of Isagro, and the focus on increasing the quality of channel management and digital marketing. The company was able to successfully raise Rs 2000 Cr through QIP. The company has raised enough funds to be able to directly acquire entities that will immediately give the ability to start manufacturing those products which they are researching but do not have any manufacturing capacity for. It remains to be seen whether there are any other disruptions in-store from COVID-19 or whether the company will be able to match its lofty guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q1FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 972 | 766 | 26.89% | 801 | 21.35% |

| PBT | 172 | 132 | 30.30% | 125 | 37.60% |

| PAT | 132 | 101 | 30.69% | 98 | 34.69% |

| Consolidated Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 1068 | 786 | 35.88% | 863 | 23.75% |

| PBT | 190 | 133 | 42.86% | 142 | 33.80% |

| PAT | 146 | 102 | 43.14% | 111 | 31.53% |

Detailed Results

-

- The company witnessed phenomenal revenue growth of 36% YoY in consolidated terms in Q1.

- The profits for the company were up for Q1 with a rise of 31% & 43% YoY respectively in standalone and consolidated terms.

- The EBITDA for the company grew 55% YoY in Q1 and EBITDA margin improved 140 bps to 22%.

- Fixed overheads declined 17% YoY in Q1.

- Isagro Asia saw good growth of 13% YoY in Q1.

- The board has recommended a final dividend of Rs 1/share.

- Exports saw a growth of 23% YoY in Q1 while domestic sales grew 76% YoY in the same period.

- FCF of Rs 298 Cr was generated in Q1. Networking capital to sales improved from 3.68 to 4.95.

- The company now has a surplus cash position of Rs 98 Cr as of 30th June 2020.

- Debt to equity was at 0.18 times vs 0.02 a year ago.

- The company saw the highest ever placement of Nominee Gold. It also launched PI MItra in Q1.

- 7 new patent applications were made in Q1 including intermediary of COVID-19.

- The company successfully raised Rs 2000 Cr in QIP at an average price of Rs 1470 per share.

- The company maintained an order book of > $1.5 billion.

- The company expects to launch 2 new products in Q2 & Q3.

- The company remains confident of achieving 20%+ growth in FY21.

Investor Conference Call Highlights

- The management attributes the stellar performance in Q1 to a solid business model portfolio of industry-leading brands, meticulous planning, and a unique go-to-market approach.

- Gross margins have fallen in standalone level due to the addition of Isagro business which had a lower margin profile as compared to the residual product portfolio. But this fall in gross margins was mitigated by the fall in fixed overheads and thus the company was able to report EBITDA margin appreciation.

- The industry has grown 10-15% YoY while PI maintained its pace by growing 1.5 times the industry growth.

- The company has seen a huge growth in inquiries in the last 2-3 years with up to 50-60 inquiries coming in. It has also seen a rise in non-agro inquiries for R&D. It is also expecting 4 to 5 products getting commercialized and negotiations with the global customers for both AgChem and non-AgChem side.

- The reason for the company not seeing an immediate increase due to quick product launches is that new molecules need 2-2.5 years to be fully commercialized.

- The management maintains its previous capex guidance of Rs 550-600 Cr in the next 1-1.5 years.

- Excluding the incremental revenue from Isagro, growth in domestic business has been >20% YoY.

- The management has guided that it will take around 5-6 quarters to fully deploy the funds raised from the QIP.

- Isagro revenues in Q1 were at Rs 99 Cr with Rs 69 Cr in domestic sales and Rs 30 Cr in exports.

- Margins are expected to stay stable at current levels for the company going forward.

- The management expects growth momentum in Isagro to remain at up to 5% in FY21.

- The company has created 2 wholly-owned subsidiaries to expand its strategy for the pharma intermediates and advanced intermediate space.

- The company currently does not have any plans to invest and set up manufacturing units for these new subsidiaries yet.

- Generally, pricing in the domestic segment has improved YoY but it remains dependent on liquidity.

- 3-4 years back, the company used to import 30-40% of RM requirements from China. Now, this number has gone down to <10%. This is mainly because the company has been able to develop a lot of alternatives in India and in geographies other than China.

- The management has admitted that the company will indeed prefer to look to expand into the pharma adjacent segment using inorganic opportunities rather than creating infrastructure, getting new approvals, acquiring incremental customers, etc.

- The company is also looking at opportunities to de-risk its concentration of operations in India.

- It is also looking to acquire complementary technologies to broaden its product portfolio.

- The management expects to maintain the Export-to-Domestic ratio of 70:30 going forward.

- The management maintains that any projects that it chooses to deploy the QIP funds in have to be EPS and margin accretive.

- The company is looking to start off MPP5 in Q2 as the regulatory system to be put there got delayed due to COVID-19.

- MPP10 has seen the biggest impact from COVID-19 as the unavailability of the contractual labor in the desired number. Has caused some projects to get delayed by a few months.

- The company has decided not to merge Isagro with PI as the addressable market for Isagro is different from PI. The management believes that a differentiated kind of go-to-market approach should help unlock tremendous value given the company’s track record of bringing in new products, safer products.

- Other synergies to rise form the Isagro acquisition will be common back-end services like finance, supply chain, etc. A key driver behind the acquisition was the underutilized capacities of Isagro. The management expects to double throughput and revenues from these assets in almost 3 years.

- The company does not have any significant molecules that are going off patent in the next 2-3 years.

- The 3 main areas to use the QIP funds are:

- Expanding into adjacent segments

- The derisking geographic concentration of operations in India

- Acquiring new technologies

- The management maintains that there are a lot of products in the R&D pipeline and the business model in CSM takes time to reflect changes and additions as products may require 1.5 to 2 years for product development, scale-up, and then commercialization.

- In Isagro, the company will shift from focusing on the end of the life cycle products to a particular segment in fruits and vegetables and plantation crops. Thus product portfolio will also change over time and expand upon margins from the current level of 8-9% to >15%.

- The management is guiding for 20%+ growth in CSM business.

Analyst’s View

PI Industries have been one of the most consistent performers in the agrichemicals business. The company saw a phenomenal performance in Q1 on the back of normal monsoons and the addition of Isagro. The China substitution phenomenon should provide the company with opportunities in both its native agrichemicals and the new adjacent space that it is looking to expand into. The company was able to successfully raise Rs 2000 Cr through QIP. It will be used to finance its expansion into adjacent segments and into expanding operations beyond India. It remains to be seen whether there are any other disruptions in-store from COVID-19 or whether the company will be able to match its lofty guidance for growth in all segments. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, a good agricultural season, and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for.

Q4FY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 800.8 | 827 | -3.17% | 869.5 | -7.90% | 3354.7 | 2900.9 | 15.64% |

| PBT | 124.9 | 168.4 | -25.83% | 169 | -26.09% | 594.4 | 534.6 | 11.19% |

| PAT | 98.3 | 124.4 | -20.98% | 120.4 | -18.36% | 442.3 | 407.7 | 8.49% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 862 | 826.9 | 4.24% | 868.9 | -0.79% | 3415.4 | 2900.4 | 17.76% |

| PBT | 141.9 | 170.1 | -16.58% | 169.8 | -16.43% | 613.8 | 537.9 | 14.11% |

| PAT | 110.7 | 125.7 | -11.93% | 121.1 | -8.59% | 456.6 | 410.2 | 11.31% |

Detailed Results

-

- The company witnessed a modest revenue growth of 4% YoY in consolidated terms in Q4.

- The profits for the company were down for Q4 with a fall of 21% & 12% YoY respectively in standalone and consolidated terms.

- FY20 was a good year for the company with an 18% YoY rise in consolidated revenues and an 11% YoY rise in consolidated profits.

- The EBITDA for the company grew 7% YoY in Q4 and 25% YoY in FY20.

- Q4 exports increased by 12% YoY.

- Isagro Asia saw good growth of 10% YoY in Q4.

- EBITDA margin maintained at 22% despite the rise in raw material prices.

- The board has recommended a final dividend of Rs 1/share.

- Exports saw a massive growth of 31% YoY in FY20 while domestic sales fell 6% YoY in the same period.

- Debt to equity was at 0.15 times vs 0 a year ago. The increase was mainly due to the higher Capex of Rs 635 Cr in FY20.

- In FY20, the company launched 5 new products, filed 22 patents, and currently has 60 new molecules in the R&D pipeline. It also reached >20% in non-agrichemical business.

- The company initiated commercial-scale business with 3 new customers and has an order book of > $1.5 billion.

- The company has frozen discretionary spending in FY21 and is looking for avenues for cost reduction.

Investor Conference Call Highlights

- The company has successfully developed an advanced intermediate for a potential COVID-19 drug.

- The management maintains a robust outlook for FY21 due to new brands coming in domestic business and expanding operations in exports. Favourable outlook for agriculture along with the expectation of normal monsoons and govt support for agriculture are also expected to contribute to the industry.

- The management remains confident of maintaining the company’s growth momentum at >20% YoY revenue growth in FY21.

- The management is not too concerned with the approval for the generic version for Osheen as the management is confident in the life cycle management of the company’s brands. Even after Nominee went generic, the company was able to maintain brand image and expand upon sales thus vindicating their confidence.

- The 11th multipurpose plant for the company started in March but had to be shut down due to the lockdown. The management is looking to start it now and the capacity will be going on full steam from Q2 onwards.

- The company is currently looking to optimize and augment its capacities to be able to handle large scale production of intermediates once the company gets client approvals.

- The management believes that there is a big opportunity for the company in the pharma intermediates industry especially due to the China substitution phenomenon that is gaining ground these days.

- The objective of the pharma intermediate business is to contribute more than 10% of total sales in 3-4 years.

- The improvement in margins in domestic business was due to the end of the life cycle of some lower-margin products which have been withdrawn now.

- The management has stated that it takes anywhere between 2-5 years for a molecule to get commercialized.

- The management sees most of the post COVID opportunities arising from India itself.

- The company does not have reason to go forward into generic manufacturing and it is mostly looking for a supportive and non-compete business model with its customers.

- The company is guiding for Rs 650 Cr of Capex again in FY21. Most of this is towards capacity expansion and some of it is to be used to repurpose existing facilities at Isagro. All of it is towards organic growth opportunities.

- The company is also in the lookout for inorganic growth opportunities in adjacent sectors like pharma or specialty chemicals.

- Out of the Rs 60 Cr revenue of Isagro, Rs 33 cr is from domestic sales and the rest is from exports.

- The management maintains that the company is on the lookout for both organic and inorganic opportunities for growth in the new pharma business.

- The management expects to gain clarity on the proposed QIP in the next 2 months.

- The management reassures that there has not been any significant change or damage to its previous plans and they have just gotten delayed due to COVID disruptions and market uncertainties.

- The management admits that chemical companies have been seeing opportunities from the China substitution phenomenon for the last 1-1.5 years and it is expected to go on. But custom synthesis manufacturing does take some time to consolidate and commercialize. The company will continue to address inquiries and keep enhancing the capacities to meet these inquiries.

- The management admits that product sales in the crop protection segment can be lumpy and thus to mitigate the issue of dependence on specific products, they are constantly looking to introduce new products in the category to balance the load and replace the existing star brand. The management believes the brand Awkira, which was launched in FY20, to be a leading brand in 2-3 years and contribute to 30-35% of segment sales in the future.

- The management admits that the company has taken price hikes for the Kharif season.

- The management expects volatility and supply-demand gap to stabilize in the next 4-6 weeks.

- The management has stated that the revenue growth target for FY21 is not taking into account any currency depreciation tailwinds and it should be seen on a constant currency basis only.

- The management maintains that the company will be able to sustain current margins and may also see margin appreciation due to change towards favourable product mix in the future.

- The company is not looking to expand in the building blocks area of chemicals like fluorine but is focussing more on value-added process technologies.

Analyst’s View

PI Industries have been one of the most consistent performers in the agrichemicals business. FY20 was very good for the company with robust growth in export businesses. The company is now expanding into adjacent segments and has already gotten into pharma intermediate space. The overall favourable outlook for agriculture and monsoons going forward bodes well for the company. The China substitution phenomenon should provide the company with opportunities in both its native agrichemicals and the new adjacent space that it is looking to expand into. Although the management plans for QIP to finance the capacity expansion for the company has been delayed due to COVID-19 disruptions and economic uncertainties, they remain confident of raising the capital required. It remains to be seen whether there are any other disruptions in store from COVID-19 or whether the company will be able to go forward with its QIP as easily as the management anticipates. Nonetheless, given the company’s strong track record, strong tailwinds of the industry, expectations of a good agricultural season and opportunities arising from the China substitution phenomenon, PI Industries remains a pivotal agrichemical sector stock to watch out for, particularly given the share resilient performance since the market crash in March.

Q3FY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY20 | Q3FY19 | YoY % | Q2FY20 | QoQ % | 9MFY20 | 9MFY19 | YoY% | |

| Sales | 869.5 | 722.7 | 20.31% | 918 | -5.28% | 2563.9 | 2073.9 | 23.63% |

| PBT | 169 | 138.9 | 21.67% | 168.8 | 0.12% | 469.5 | 388.2 | 20.94% |

| PAT | 120.4 | 107.3 | 12.21% | 122.8 | -1.95% | 344 | 283.3 | 21.43% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY20 | Q3FY19 | YoY % | Q2FY20 | QoQ % | 9MFY20 | 9MFY19 | YoY% | |

| Sales | 868.9 | 722.2 | 20.31% | 918.3 | -5.38% | 2553.4 | 2073.6 | 23.14% |

| PBT | 169.8 | 139.5 | 21.72% | 169.3 | 0.30% | 471.9 | 367.6 | 28.37% |

| PAT | 121.1 | 107.7 | 12.44% | 123.2 | -1.70% | 345.9 | 284.8 | 21.45% |

Detailed Results

-

- The company witnessed good revenue growth of more than 20% YoY in both standalone and consolidated terms.

- The profits for the company were similarly good with PBT and PAT rising 22% and 12% YoY in both standalone and consolidated terms.

- The EBITDA for the company grew 24.6% YoY and EBITDA margins stood at 21.9%.

- The revenues were up mainly on the back of a 19% improvement in exports and 24% improvement in domestic business.

- Overall the 9MFY20 was good for the company with revenues rising 23% YoY and profits rising 21% YoY.

- EBITDA for 9MFY20 was up 31.7% YoY while EBITDA margins in the period were at 21%.

- The effective tax rate for the company was at 27%.

- The net debt position of the company as of 31st December 2019 was Rs 252 Cr.

- The company has announced an interim dividend of Rs 3 per share.

- The company has also completed the acquisition of Isagro Asia. Total consideration paid out for this transaction was Rs 455 Cr. The domestic distribution business of this company will be transferred to Jivagro Ltd and the rest will be merged with PI Industries.

- The board of directors has approved fundraising of Rs 2000 Cr to support the next leg of growth for the business. The details of this fundraising are yet to be decided.

Investor Conference Call Highlights

- The company’s new product Awkira has seen positive response in the recent rabi season.

- The management expects the company’s distribution and crop reach to get stronger post-acquisition of Isagro.

- The company will also repurpose Isagro’s existing plants to enhance the company’s manufacturing capacity and this is expected to start operations in FY21.

- The management has stated that the main objectives of the fundraising plan is to

- scale-up organic growth and expansion,

- scale-up niche technologies that the company has developed in the last few years,

- and to diversify into adjacent verticals which could be CDMO or CSM for pharma or specialty chemicals or even nutraceuticals or carbonizing chemicals.

- The company is yet to finalize which way to go in the new verticals.

- The management has clarified that the company sources less than 10% of its raw materials from China in the CSM business mostly. So it will not face any significant disruption from the coronavirus event if it drags on further.

- The company has started a new multiproduct plant in the quarter and another will be commissioned by the end of Q1FY21.

- The company has plans to start one more plant in FY21 by Q2FY21.

- The management has acknowledged that the revenue generation for the company is more in H2 of the year typically and this is expected to continue.

- The company has already done Capex of Rs 550 Cr in Fy20 so far and is expected to do Rs 50 Cr more by the end of the year. This number is not including the Isagro transaction.

- The estimated Capex for FY21 is around 250-300 Cr.