About the Company

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. The exchange platform enables efficient price discovery and increases the accessibility and transparency of the power market in India while also enhancing the speed and efficiency of trade execution. In August 2016, the Exchange received ISO Certifications for quality management, Information security management, and environment management. The Exchange is now a publicly listed company with NSE and BSE. IEX is approved and regulated by the Central Electricity Regulatory Commission (CERC) and has been operating since 27 June 2008.

Q4FY23 Updates

Financial Results & Highlights

Detailed Results:

- On a consolidated basis, for fiscal year 2023 the revenue declined by 2.1% on a year-on-year basis from 484.4 Crores in FY22 to 474.1 Crores in FY23.

- PAT at 305.9 Crores was lower by 0.9% on a year-on-year basis as compared to 308.6 Crores in FY22.

- Revenue breakup for Q2 included

- Transaction fees – 80%

- Admission & annual fees – 4%

- Other income – 16%

- IGX generated a total volume of 50.9 million MMBTU during FY23, a 319% year-on-year increase. A total of 2,355 trades were executed during this year, an increase of 400% on a year-on-year basis. The profitability of IGX for FY23 has increased to Rs.28 Crores from 1.75 Crores in FY22.

- For the fiscal year 2023, IEX traded 96.8 BUs, a decline of 5% year-on-year, the day-ahead market price was Rs.5.96 per unit which was higher by 36% on a year-on-year basis.

- TAM & DAC Volume increased over 115% and 240% YoY respectively in FY’23.

- IEX’s market share in the following products in Q2:

- DAM :- >99%

- RTM:- >99%

- Green Power:- 88.4%

- TAM:- 88.4%

- LDC:- 88.4%

Investor Conference Call Highlights:

- For fiscal year 2023, the Board of Directors of the company announced a final dividend of Rs.1.

- During the year the Board of Directors of the company approved the buyback of the equity shares from the open market amounting to Rs.98 Crores and this was completed successfully from January to March.

- IEX plans to help build a vibrant gas market in India enabling the Government’s aim of doubling their share of natural gas in the energy mix of the country.

- There was a reduction in the availability of e-auction coal by over 50% to 53 million tonnes in FY23 in comparison to 108 million tonnes in FY22 leading to a higher premium of nearly 260%, recently the prices of e-auction coal have reduced to a premium of nearly 137% over the notified price in April 2023.

- The average market clearing price for DAM for the fiscal increased by nearly 36% to Rs.5.96 per unit.

- For gas also the prices have reduced to almost about $10 per MMBtu in May which is a drop of more than 100% on a year-on-year basis.

- Section 11 of the Electricity Act was invoked thereby all imported coal-based power plants were asked to operate at full capacity with the option of selling unsold power on the power exchange.

- General Network Access was notified during the year,& it will remove regulatory arbitrage which has led to a temporary shift of volume from DAM to DAC and will be more conducive towards further market development in the country, this will be effective from August 1, 2023.

- IEX launched the much-awaited Term-Ahead market contracts with delivery up to 90 days. This contract enables customers to help risk against volatility in the spot market.

- IEX commenced trade in the High Price Day-Ahead market after it was launched on March 9, 2023. This segment will bring more capacity to the spot market during the high-demand period.

- Going forward with gradual improvement in domestic production of coal and improvement in coal inventory which is at 14 days compared to 11 days of last year and reduction in imported coal and gas prices, management expects rationalization of power prices on the exchange platform. This will enable cost optimization by DISCOMs and Open Access consumers and should result in higher volume on the exchange platform.

- IEX has been certified as India’s first carbon-neutral power exchange by using market-based tradable instruments to offset its carbon emissions.

- The management expects good volume growth in the DAM market. Last year approximately 1.6 BU was done in 8 months, this year they are planning at least 5 BU in this segment. Already done 1 BU in two months, at this rate it should be more than 6 BU.

- The employee cost HAS cOme down from 41 Crores to 34.5 Crores, it was majorly because some portion of the IGX cost was in the IEX cost for the nine months of last year, which was of significant value and secondly because of the higher profits last year there was a provision there for the variable scheme. So these were the two impacts there because of which we can see a gap in the cost.

- There was a shift of investments into long-term products and secondly because of few initiatives the funds were parked into good-yielding products.

- Management thinks there is a significant improvement in the supply side but it is not as it was two years back. But in the next two to three months with the increased coal supply to the IPPs, there should be further improvement in the supply side.

- IEX has a better share in the day-ahead contingency market in comparison to the other two exchanges.

- Last year there was more demand than supply that is why the prices were higher. This year they are expecting a much better situation because coal production targets are very high. The target is for 1 billion tonnes of coal production which is 12% more than last year. Whereas the electricity demand increase is expected to be only 5-6%, so increased coal availability in the market should lead to better liquidity on the sell side and lower price on the exchange platform.

- The transactions happening in the DAC market are mainly because of the arbitrage available in the DAC market. Once that arbitrage is over there is no reason for the transaction to happen in the DAC market.

- If the arbitrage situation persists IEX will lose market share.

- IEX will be taking only supply-side bids and forwarding them to the NLDC who will take them based on the merit order, the transaction fee can be charged up to Rs 0.02. IEX does not intend to charge any fees as the scope of work is very less.

- Now since the demand has increased, if there is a shortage of capacity maybe for 15 days or 1 month in this year, gas-based generation can also be utilized.

- While higher input costs impacted their volumes last year, now going forward with increased coal production and cooling down of prices of input materials. IEX expects lower clearing prices and increasing optimization potential for Discoms and Open Access consumers, thereby supporting better volumes on their platform.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for the physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company saw a miniscule quarter on quarter growth of around 8% due to volume, revenues & profit degrowth. IGX saw a great rise in volumes mainly on the back of increased consumption in the country and the power shortage due to rising fuel costs however IEX on a standalone basis saw lower volumes due to lack of supply in the market leading to higher price discovery. It remains to be seen whether the MBED development will pan out as the management expects, how will it grow its subsidiaries like ICX & IGX and how IEX will fare with the addition of new rival exchanges in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a leading player in this industry.

Q3FY23 Updates

Financial Results & Highlights

Detailed Results:

- On a consolidated basis, PAT & PAT was down 11% YoY as the company witnessed a slowdown in growth.

- 2.2% consolidated volume degrowth YoY was witnessed.

- EBITDA decreased by 10.4% YoY.

- Revenue breakup for Q2 included

- Transaction fees – 86%

- Admission & annual fees – 4%

- Other income – 10%

- Indian Gas Exchange traded 24.4 million MMBTU in terms of volume(a 560% rise) while PAT stood at 12.5 Crs..

- India witnessed an increase in electricity consumption by 6.8% YoY to 343 BU.

- IEX’s market share in the following products in Q2:

- DAM :- 100%

- RTM:- 100%

- Green Power:- 85%

- TAM:- 55.2%

- LDC:- 53.4%

Investor Conference Call Highlights:

- In the quarter that ended December 2022, the price of e-auction coal continued to be high, While the quarterly average price premium declined from 293% in Q2 FY23 to 242% in Q3 FY 23, it was considerably higher as compared to 35% for the special forward e-auction price for the power sector in FY 22.

- Continuing high spot e-auction coal prices led to the average clearing price in the Day-ahead market at Rs 4.56 in Q3 FY23, while lower from Rs.5.40 in the previous quarter, but still high to provide optimization potential for Discoms and Open Access consumers.

- During the quarter, coal production increased by 8.7% YoY to 225mt, while coal dispatch to the power sector remained almost similar at 184 mt compared with the same period FY22. leading Inventories at power plants of 13 days.

- The company is seeing good traction in long-term contracts having conducted more than 50 auctions. But since the price discovery in this auction is on the higher side because of supply-side constraints, many of these auctions have not resulted in a contract.

- The management sees good scope for growth in long-term contracts as Almost 50 billion units of transactions are happening in less than one year contract for the trading companies.

- Despite of increase in coal production, the majority of volumes are going towards PPA’s for states to run their power plants, leading to lower volume on exchanges & higher prices.

- The management explains that demands primarily come from A) DIscoms, B) states located far away from coal plants, & C) Industrial consumers. Therefore when clearing prices are high, demand comes only from Discoms leading to lower volumes.

- The regulators have already issued the GNA regulations where they have addressed this issue and there will be no double charging. Only thing is that GNA regulations will be implemented after the finalization of the grid code and transmission charge-sharing regulations.

- The present companies who have long-term PPAs(which contribute 85% of total contracts), after 25 years, are free to sell their power in the market having the option to sell the power under bilateral contracts, on a medium-term basis or short-term basis, but the Exchange is the most flexible option as per management.

- The company is confident that its share of the green market will increase from 6% to 10% in the coming year.

- The management doesn’t see allowing trading companies to have any adverse impact on REC volumes.

- The IGX share in the total gas volumes of the country stands at 1-1.5%.

- The management expects volumes in IGX to rise due to a decrease in LPG prices.

- Quarterly overheads at IGX stand at 5.5 Crs.

- The SEB volumes on the Buy side are about 88% to 90%, and on the sell side, it is 65%.

- The company states that it is witnessing deficit buying & therefore as the supply will improve and as the input cost goes down, it expects more buyers to come from the same SEBs.

- The non-SEB volume is only 10% because prices are very high & As the prices will start to come down, this number is expected to go up to as high as 30%- 35%.

- The INR12 Rs. price cap is expected to continue but management doesn’t expect this to hamper IEX’s volume.

- The management expects TAM volumes to go down with the increase in coal supplies, and price moderating on the exchange platform.

- The rise in coal prices is due to higher demand growth of 10% Vs earlier periods of 5-6% coupled with higher international prices.

- The management states that ICX is going to be a global opportunity (That is why the name of this company is International Carbon Exchange) Because as of now, many European and American companies who have to comply with their ESG commitment, are buying these carbon credits & there is a good opportunity for sale from India, Southeast Asia countries and African countries.

- The company currently has contracts for the delivery of up to three months & it is in talks with the regulators to approve the delivery of contracts of up to 11 months.

- On the regulatory and policy front several developments took place:-

- A) In early December the new REC regulations for RE generators were implemented. The new REC mechanism of no floor price and fungibility between REC is likely to increase liquidity in the market.

- B) The trading of ESCerts is expected to start this month. Recently, CERC made amendments to define a Floor Price for trading Energy Savings Certificates, fixed at 10% of the price of one metric tonne of oil equivalent of energy consumed as notified by the Central Government.

- C) The GNA regulations were notified in October 2022 and were partially implemented as the Grid Code is in the draft stage. The regulations are expected to be implemented before the end of FY23. Implementation of GNA will remove regulatory arbitrage which has led to the temporary shift in Volume from DAM to DAC and will be more conducive towards further market development within the country.

- D) CERC issued the Deviation Settlement Mechanism and Related Matters Regulations, 2022 linking the DSM charges to the time block-wise price discovered on the Exchanges. This will discourage discoms to over-draw under DSM and will lead to an increase in RTM volumes on the Exchange.

- REC market witnessed a de-growth of 68% on a YoY basis as compared to Q3 FY22 as Q3 FY22 had exceptionally high REC volumes of 38.3 lacs to fulfill the pent-up demand caused by a stay on REC trading by APTEL for almost a period of 16-months.

25 . In November 2022, IEX filed a petition for introducing the High-Price Day Ahead (HP-DAM) market to enable generators that have high variable costs of more than Rs. 12/ unit to participate in the market & it is expecting this to start by February 2023.

26 . The quarter saw IEX become India’s first carbon-neutral Power Exchange, using market-based tradable instruments to offset its carbon emissions.

27 . During this quarter, 7 members including RIL, BP Exploration (Alpha), and Vedanta Limited, joined IGX.

28 . IGX launched GIXI – the first-ever nationwide price index to reflect benchmark natural gas prices for India. The IGX Price Index is developed with the purpose to derive a single price for the country in line with international benchmarks such as JKM, HH, WIM & TTF.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for the physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company saw a poor quarter due to volume, revenues & profit degrowth. IGX saw a great rise in volumes mainly on the back of increased consumption in the country and the power shortage due to rising fuel costs however IEX on a standalone basis saw lower volumes due to lack of supply in the market leading to higher price discovery. It remains to be seen whether the MBED development will pan out as the management expects, how will it grow its subsidiaries like ICX & IGX and how IEX will fare with the addition of new rival exchanges in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q2FY23 Updates

Financial Results & Highlights

Detailed Results:

- On a consolidated basis, PAT was up 3% QoQ & down 8% YoY while revenue for the quarter was up 0.3% QoQ & down 7% YoY, as the company witnessed a slowdown in growth.

- 11% volume degrowth YoY was witnessed across all markets in Q2 .

- EBIDTA decreased by 8.8% YoY & increased 1.5% QoQ.

- Margins were at 63% for Q2 .

- During the quarter, the Exchange traded 23.1 BU electricity volume versus 23.4 BU in Q1 FY’23. The volume comprised of 19.7 BU in the conventional power market, 1.5 BU in the Green Market segment and 19.14 lac Certificates in the Renewable Energy Certificates (REC) Market which is equivalent to 1.9 BU.

- Revenue breakup for Q2 included

- Transaction fees – 80%

- Admission & annual fees – 4%

- Other income – 16%

- Indian Gas Exchange traded 5.9 million MMBTU in terms of volume and the profit after tax was recorded at Rs 2.42 Cr. witnessing a growth of 111% on QoQ basis.

- India witnessed an increase in electricity consumption by 6% YoY to 385 BU.

- IEX’s market share in the following products in Q2:

- DAM :- 99.5%

- RTM:- 100%

- Green Power:- 91.8%

- TAM:- 49.1%

- ESCerts:- 97%

Investor Conference Call Highlights:

- The Government of India reduced the supply of coal through e-auction and increased the supply of coal to Gencos with long-term PPAs to manage the power crisis. This led to the E-auctioning quantity declining by 63% YoY in the first 5 months of FY23 which led to increasing in E-auction prices & decline in the availability of E-auction coal, however, coal situation is improving.

- During the quarter, the domestic coal production increased by 10% YoY and the dispatch to the energy sector grew by 11% YoY

- The Govt. brought in several policies & amendments in the acts like the Energy conservation act, the draft electricity amendment Rules 2005, etc, which will create a conducive environment for the power market.

- Management believes that with a rationalization of power prices on the Exchange, the volumes are expected to improve in H2.

- The company successfully added daily contracts for up to 90 days, weekly contracts for up to 12 weeks, and monthly contracts for up to 3 months to its existing Longer Duration Contracts portfolio. These new products now constitute nearly 40% of the total traded volume of electricity on the exchange.

- The management expects H2 to be significantly better due to the better availability of coal.

- The company expects the ancillary markets to be available through the exchange platform from 1st January 2023.

- The company is actively working with Govt. for bringing derivative contracts because it believes that when derivatives are launched in the market, it will bring large volumes & liquidity & reduce the volatility in the price since the participants will have the option to hedge their position in the derivative market.

- The DAC portion increased upwards of 50% due to single charging of transmission from either the buyer or seller unlike double charging taking place in DAM. However, the company expects this anomaly to get resolved post-introduction of GNA from 1st January.

- RTM market is mainly improving because of the higher share of renewable generation taking place in the country & variability in the renewable generation.

- The management states that if the n the availability of coal improves and prices go down further to maybe about INR 3.25 paisa to INR 3.40 paisa, then 1) distribution companies will meet their demand, 2) they optimize their cost and shut down their costly plants. And 3) it is viable even for industrial consumers to buy power from the exchanges.

- The revenue fall was higher Vs volumes due to rebates on REC certificates & concessions in membership & client fees.

- The management explains the carbon credit market where there will be a voluntary market involving companies buying these credits to comply with ESG initiatives & create branding & then there will be another compulsory market created & regulated by Govt.

- The management states that the “ draft national electricity plan projection is around 7% growth in the demand for the next five years which is a very high number & If the demand increase continues to happen, I’m sure a good part of the demand increase will come in the market.”

- The management states that even though the majority of renewable capacity is under PPA, their participation has started increasing in the exchange.

- The company is confident of achieving 20% growth in volumes in the electricity segment if demand grows by 7-8% in the coming FY.

- The management explains that “ in a country like India, maybe we’re talking about 7%, 8% kind of GDP growth, and our per capita consumption is only about 1,300, 1,400 units per year. The world average is more than 3,500, which is huge. There is a very high potential for power demand growth which is not happening because there’s no incentive for distribution companies to supply more power”.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company saw a poor quarter & H1 due to volume, revenues & profit degrowth.. IGX saw a great rise in volumes mainly on the back of increased consumption in the country and the power shortage due to rising fuel costs however IEX on a standalone basis saw lower volumes due to lack of supply in the market leading to higher price discovery.. It remains to be seen whether the MBED development will pan out as the management expects and how IEX will fare with the addition of new rival exchanges in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q4FY22 Updates

Financial Results & Highlights

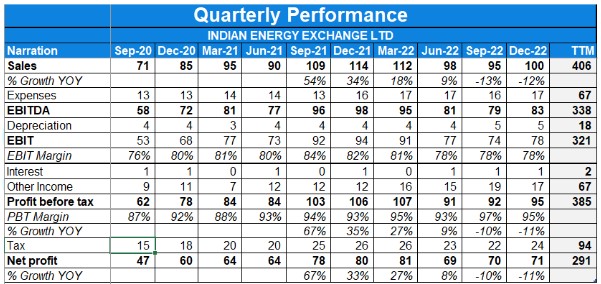

| Standalone Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 128 | 102 | 25.5% | 127 | 0.8% | 478 | 357 | 33.9% |

| PBT | 106 | 84 | 26.2% | 106 | 0.0% | 400 | 282 | 41.8% |

| PAT | 81 | 64 | 26.6% | 80 | 1.3% | 302 | 213 | 41.8% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 128 | 100 | 28.0% | 131 | -2.3% | 484 | 356 | 36.0% |

| PBT | 107 | 80 | 33.8% | 107 | 0.0% | 398 | 270 | 47.4% |

| PAT | 88 | 60 | 46.7% | 80 | 10.0% | 309 | 205 | 50.7% |

Detailed Results:

- On a consolidated basis, PAT was up 46% YoY while revenue for the quarter was up 28% YoY ( before exceptional items).

- 21% volume growth YoY was witnessed across all markets in the quarter with FY22 seeing 37% YoY growth in volumes.

- Margins were at 63% for the Q4 & FY22.

- Revenue breakup for Q4 included

- Transaction fees – 83%

- Admission & annual fees – 5%

- Other income – 12%

- Indian Gas Exchange sees volume growth with 7 million MMBTU traded in Q4 & 12 million MMBTU traded for the year.

- IGX achieved breakeven with PAT of approx. Rs 1.8 Cr in FY22.

- Total electricity consumption in India has risen 7.8% YoY in FY22.

- Final dividend of Rs.1 was announced in Q4 and with total dividend payout for the year at Rs. 2.

Investor Conference Call Highlights:

- In FY22, volumes involved 90.6 billion in conventional power market, 5 billion in green market and 6.4 billion in certificates.

- New segment such as RTM cumulatively contributed 24% to total volumes.

- The company was conferred as best business by finance minister in 70TH CNBC business excellence awards.

- The company is working to promote long term power contracts, national access registry etc .

- CRC approved IEX for hydro power contracts trading.

- The company will be shortly launching web based platform for its customer to make trading more seamless along with provide research and information to its customers.

- The management saw demand for April increase by 11-12% YoY

- The management saw gap between demand and supply leading to high prices in exchange leading to capping of price by Govt. which led to buyers shifting to alternative platforms but management believes this to be short term phenomenon and expects scenario to improve from May onwards.

- Since the company can only launch products for 11 days, thus it is launching long duration contracts offering delivery contracts upto 365 days & get good share from bilateral market where market size is 55-60 Billion units.

- Cross bidding is a new innovative product by co. which is will help in efficient selling & buying of power.

- National open access registry product by co. will help in streamlining process and grow the spot market.

- Market share of company for certificates in FY22 was 75%

- The company expects 80-90 lakh certificates to happen in FY23 Vs 60 lakh in FY22.

- The company paid 60% dividend pay out of total net profit & expects to continue this policy in future.

- The company’s market share of total generation is 7% & wants to take this share to 25% through thrust of Govt. due to high renewable power generation to be expected in the future & integration with grid which will require a liquid platform for exchange.

- The company expects to grow at 20-25%.

- Power shortage scenario is not conducive for the market and will adversely affect company’s performance in future.

- Revenue achieved by IGX is 5.6 Cr and EBIDTA of 1.8 Cr.

- Open access market’s clearing price is Rs. 4.4 which is very high leading to volume degrowth of 8%.

- The company is interacting with regulators to take part in unified carbon market.

- The company expects order in NBC within a month.

- The management doesn’t expects its market share to get hindered by someone offering at lower transaction costs as the key value provided in the form of liquidity is the key for the biz and due to small part of transaction fees to total revenue to the seller of power, they believe that the seller won’t shift to another platform just because of lower transaction fees.

- Higher volume & prices has led to significant increase in payables amount which is a short term phenomenon and will normalise.

- The company expects gas volumes increasing post rationalisation of gas prices.

- The management doesn’t intends to revise its exchange fees upwards.

- Since company has to reduce its stake in IGX to 25% post 5 years , it will explore various options like an IPO to reduce its stake.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company continues its growth march with another good quarter with volume growth of 21% YoY and sales & profit growth of 28% & 46% YoY. IEX saw a great rise in volumes mainly on the back of increased consumption in the country and the power shortage due to rising fuel costs. It has also received approval for long duration contracts and is planning to launch ESCERTs and GTAM very soon.. It remains to be seen whether the MBED development will pan out as the management expects and how IEX will fare with the addition of new rival exchanges in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q3FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 127 | 96 | 32.3% | 121 | 5.0% | 350 | 256 | 36.7% |

| PBT | 106 | 78 | 35.9% | 103 | 2.9% | 293 | 198 | 48.0% |

| PAT | 79 | 60 | 31.7% | 78 | 1.3% | 222 | 150 | 48.0% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 131 | 96 | 36.5% | 122 | 7.4% | 356 | 256 | 39.1% |

| PBT | 107 | 76 | 40.8% | 102 | 4.9% | 291 | 191 | 52.4% |

| PAT | 81 | 58 | 39.7% | 77 | 5.2% | 220 | 144 | 52.8% |

Detailed Results:

- On a consolidated basis, PAT was up 40% YoY while revenue for the quarter was up 36% YoY.

- Traded volume on exchange increased by 37% YoY.

- India’s renewable installed capacity is 151 gigawatts.

- Power consumption in the Q3 of FY22 increased by 5% CAGR on a 2 year basis.

- IGX recorded trade volume of 3.6 MMBTU in Q3. It has now reached break-even level.

- Margins stood at 63.1%.

- Interim dividend of 100% per equity share was announced.

- Real time market (RTM) grew by 70% YoY & contributed 20% of the total revenues

Investor Conference Call Highlights:

- The power consumption in India has risen with a CAGR of 5% in the least 2 years.

- The CERC draft (Connectivity and General Network Access to the inter-State Transmission System) was released in Dec which is expected to clarify on how transmission access will be available for participants on the Exchange. The General Network Access is expected to promote the power market in India according to the management.

- The dispute between SEBI & CERC has been resolved which will lead to introduction of long duration contracts & electronic derivatives in power exchanges.

- The company will be able to launch long duration contracts in the next financial year.

- The management states that electricity derivatives will smoothen out the price volatility, and buyers will be able to hedge their portions and take delivery in the spot markets, which will lead to an increase in exchange transactions.

- The National Open Access Registry is likely to be implemented by Q4 of FY22 which will lead to further development of power market in India.

- Trading in the REC market has resumed in Nov and the management expects good momentum ahead in this market.

- The company has commenced cross border electricity trade initiatives with key stakeholders in Bangladesh & Nepal.

- The RTM segment grew 70% YoY and accounted for 20% of overall electricity volumes on the exchange.

- The company has also applied for a voluntary gross bidding platform which would simulate the objectives that the MBED draft is looking to achieve.

- The management expects ESCerts trading to start from next month.

- After the stake sale of 4.93% to IOCL, IGX is now an associate company of IEX.

- The company brought in NSE as a strategic investor with 26% stake sale due to its experience of dealing in large volumes as well as avoiding competition with another exchange like NSE according to the management.

- The management believes that general network access is a very market friendly regulation as only buyers will have to pay charge now instead of both sellers & buyers thus making the process simpler. Further, a provision for short-term general network access has been introduced for meeting seasonal demand of 2-3 months.

- The management states that if the gross bidding voluntary mechanism is implemented effectively and used by the states effectively, the MBED will become redundant.

- The management expects IEX to garner decent market share of REC. the demand for RECs is much higher currently due to the inactivity of the last 2 years and REC inventory being limited as no new capacity is being added under the REC scheme.

- The top 10 buyers constituted about 58% of total volumes.

- The top 10 sellers contributed about 56% of total volumes.

- The company charges Rs 20 from buyer & seller each on every energy certificate.

- Of the 37% YoY growth in volumes in IEX, 20% was from REC and ESCerts. The remaining 17% was from electricity trading of which RTM was a significant share.

- The volumes from green market have increased from 0.7 BU to 1.2BU in the current year. The management expects to see good growth even in future.

- The management is confident about future growth prospects despite emergence of the 2 new rival exchanges.

- The other expenses were optically higher in the Q3 due to bonus issue and higher expenses on CSR.

- The company’s gas exchange division has seen volumes grow from 3.3 Lac MMBTU in Q1 to 36 MMBTU in Q3 in FY22 so far. The management expects exponential growth in coming quarters as well.

- The DAM volume is growing tepidly due to higher growth from green markets and RTM.

- The management states that IEX has a consistent policy of giving more than 50% of its profits in the form of dividends & it intends to maintain the same.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company continues its growth march with another good quarter with volume growth of 37% YoY and sales & profit growth of 36% & 40% YoY. IEX saw a great rise in volumes mainly on the back of increased consumption in the country and the resurgence of the REC and ESCerts segments. It has also received approval for long duration contracts and is expecting the resumption of ESCERTs and GTAM very soon. The management does not appear very concerned about the MoP directive for MBED implementation by April 2022 and has even applied for a product for a gross voluntary bidding mechanism which will make MBED redundant. It also states that MBED implementation is still very open to changes under discussion, and it should not lead to any decrease in volumes for IEX. It remains to be seen whether the MBED development will pan out as the management expects and how IEX will fare with the addition of new rival exchanges in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q2FY22 Updates

Financial Results & Highlights

|

Standalone Financials (In Crs) |

||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 121 | 79 | 53.16% | 102 | 18.63% | 223 | 160 | 39.38% |

| PBT | 103 | 62 | 66.13% | 84 | 22.62% | 187 | 120 | 55.8% |

| PAT | 78 | 47 | 65.96% | 64 | 21.88% | 142 | 90 | 57.78% |

|

Consolidated Financials (In Crs) |

||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 122 | 79 | 54.43% | 103 | 18.45% | 225 | 160 | 40.63% |

| PBT | 102 | 58 | 76% | 82 | 24.39% | 184 | 115 | 60% |

| PAT | 77 | 44 | 75% | 62 | 24.19% | 139 | 86 | 61.63% |

Detailed Results:

- On a consolidated basis, PAT was up 75% YoY while revenue for the quarter was up 54% YoY.

- Q2FY22 saw an increase of 57.6% YoY in electricity exchange volumes.

- Indian Gas Exchange sees volume growth with 10 Lac MMBTU traded in Q2 vs 3,60,050 MMBTU traded in Q1.

- Total electricity consumption in India has risen 9.7% YoY in Sep.

- Total installed power capacity in India grew 4.2% YoY to 389 GW. The renewable capacity saw 13.8% YoY growth with cumulative capacity to 101.5 GW in Q2FY22.

- The court dispute about long duration contracts has been resolved and long duration delivery contracts are now under CERC while electricity derivatives are under SEBI.

- The Ministry of Power has issued a press release stating that MBED to be operational on exchanges by April 2022. It has also released another release mentioning redesigning of REC price mechanism to allow REC prices to be market determined.

- IEX saw trading volumes for H1 grow 50.6% YoY.

- The real-time electricity market grew 125% YoY. It traded 5.3 BU in Q2.

- The green market cumulatively traded 1.7 BU during Q2 and 3.4 BU since inception.

- IEX is now looking to launch trading in ESCERTs.

- Gas producers are allowed to trade 10% of production or 500 MMSCM, whichever is higher on exchanges.

- The company announced a bonus share issue of 1:2.

Investor Conference Call Highlights:

- H1FY22 has seen a 14% YoY rise in power consumption in India.

- LNG prices have risen 10x YoY to $30 per MMBTU.

- IEX received CERC approval to commence the Green Day-Ahead contract as a part of the integrated Day-Ahead market. Under the integrated Day-Ahead market, that change will allow the market participants to submit bids together with [indiscernible] as we were doing in the DAM market.

- IEX has also launched value-added services for renewable energy generators.

- The Ministry of Power issued the draft rules for promoting renewable energy through open access, driving consumers with contracted demand load of 100-kilowatt and above as eligible for green energy open access.

- RTM contributed almost 20% of the overall volume on the exchange.

- ESCERTs and STAM are expected to be launched on 26th Oct 2021.

- Long duration contracts planned to be launched by IEX will be for fortnightly, monthly, quarterly and yearly contracts. All of these contracts will be for less than 1 year.

- The management states that the implementation of MBED can be as complicated as the implementation of GST.

- The management expects the long-duration contracts to be launched in the next few weeks.

- The management states that the major reason for the shift from bilateral contracts to exchange trading in the power procurement in India was mainly due to superior supply-demand matching provided by the exchange mechanism.

- For long-duration contracts, the company will be putting in an LC mechanism for payment security and will also ensure that delivery happens only after payment is done. The exchange has the authority to regulate and intervene as part of the contract.

- The company has put in the DSM mechanism for any shortfall in the contract. For example, if party A is to sell 100 megawatts, & they are selling 90 megawatts, they will have to use DSM to pay for the pending 10 MW.

- The management states that the company is ready to prepare for the MBED implementation and all things in the proposal are under discussion.

- The company is indeed looking to target bilateral contracts using the long duration contracts trading according to the management.

- The company will have a revenue-sharing arrangement with MCX for electricity derivative trading as MCX will be using prices from IEX.

- The management states that there isn’t any international benchmark on transaction charges, and they depend on the ground situation in the geography the exchange is functioning in.

- The management indicates that there isn’t much threat from the market coupling issue as it will not reduce trading volumes for anyone.

- The management states that the purpose of MBED is mainly to keep power prices subdued and to help manage capacity better and promote renewables.

- The management states that to facilitate the transition to renewables, the exchange mechanism needs to be promoted as helps address the variability of renewable power generation.

- The major advantage of IEX according to the management is its long history of consistent performance on the exchange which should help it preserve its volumes even with the implementation of MBED.

- The management admits that power volumes are not consistent and Q2 is also seasonally higher than other quarters.

- The company is on the lookout for growth and diversification opportunities to use its surplus liquidity.

- The derivative market should not have any threat to the spot market as most of it will be financially settled and the physical settlement will also take place through the spot market only.

- Any delivery of the derivatives from MCX will be done by IEX only.

- IGX is expected to break even by Q4.

- The transaction charges for IGX are at Rs 4 per MMBTU.

- The management expects volumes in GTAM to rise slowly but steadily over time.

- Open access volumes accounted for less than 20% of total volumes in Q2.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company continues its growth march with another good quarter with volume growth of 58% YoY and sales & profit growth of 54% & 75% YoY. IEX saw a great rise in volumes mainly on the back of increased consumption in the country and the power shortage due to rising fuel costs. It has also received approval for long duration contracts and is planning to launch ESCERTs and GTAM very soon. The management does not appear very concerned about the MoP directive for MBED implementation by April 2022. It states that MBED implementation is still very open to changes under discussion, and it should not lead to any decrease in volumes for IEX. It remains to be seen whether the MBED development will pan out as the management expects and how IEX will fare with the addition of new rival exchanges in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q1FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 102 | 81 | 25.93% | 102 | 0.00% |

| PBT | 84 | 58 | 44.83% | 84 | 0.00% |

| PAT | 64 | 43 | 48.84% | 64 | 0.00% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 103 | 81 | 27.16% | 100 | 3.00% |

| PBT | 82 | 56 | 46% | 80 | 2.50% |

| PAT | 62 | 42 | 48% | 61 | 1.64% |

Detailed Results:

- On a consolidated basis, PAT was up 48% YoY while revenue for the quarter was also up 27% YoY.

- Q1FY22 saw an increase of 42.9% YoY in electricity exchange volumes.

- Indian Gas Exchange sees volume growth of 206% QoQ with 3,60,050 MMBTU traded in Q1

- Nepal becomes the first country to start doing the Cross Border Electricity Trade with IEX.

- Total installed power capacity in India grew 3.5% YoY to 384 GW. The renewable capacity saw 10.4% YoY growth with cumulative capacity to 97 GW in Q1FY22.

- The Govt of India has issued the draft National Electricity Policy 2021 which stipulates intention of the Government to increase the share of spot markets to 25% by the year FY24.

- The real-time electricity market traded 4,635 MU in Q1 at an average price of Rs 3.01.

- There was a 39.5% YoY growth in open access volumes.

- The green market cumulatively traded 937 MU during Q1 which was higher than the total volume of 785 MU in FY21.

- The company announced a final dividend of Rs 1.5 per share for FY21.

Investor Conference Call Highlights:

- IEX launched Phase 1 of the web-based platform for the market participants.

- It is in talks with Bhutan and Bangladesh for commencing cross-border electricity trades.

- The company has implemented a Mixed-Integer Linear Programming price history algorithm.

- RTM now contributes to over 20% of traded volumes.

- GTAM grew 41% YoY in FY21 while the bilateral market declined 25% in the year.

- Ancillary services through the exchange have an opportunity size of 3000-4000 MW but the exchange will only be collecting the bids and passing it on to NLDC who will take care of everything else.

- The management states that MBED should only be implemented once each state has adequate contracted capacity to meet its demand.

- The management states that in the case of DAM, price matching for buyers and sellers takes place while for the day ahead, price discovery takes place. DAM markets provide more flexibility by allowing for sales of electricity for a specific time block and removes the need to buy power throughout the day ahead.

- Power consumption in India in Q1 was up 17% YoY.

- The management states that the LDC issue can be expected to be resolved in the courts by Q4FY22.

- REC trading started in July, but it is still being discussed by the Ministry of Power and can be expected to see orders coming in by Sep.

- Right now, DSM rates are the same as the day ahead rates so there is little incentive for discoms to buy from the RTM. The management states that the regulators are working to establish a DSM rate where there is an additional incentive for buying in RTM for discoms instead of over-drafting on the grid. When this happens, DSM volumes will start shifting to RTM.

- DSM should be seen as only a component of the opportunity size for RTM which is much bigger than DSM.

- The management is expecting an opportunity size of 8-10 billion units from the cross-border trade in the next 5 years.

- GTAM should continue its good momentum for the next 4-5 months till wind generation is high.

- The margin mechanism for LDC is expected to be 2 days of margin for the transaction. This is yet to be approved by the regulator.

- The management is not worried about the incoming competition as it is confident of IEX’s edge and long customer relationships.

- The company is advocating for a policy change to make solar power generators keep up to 15% of power for sales to the market.

- The management states that the long-term shift to renewables in the energy sector should be beneficial for the exchange.

- The primary opportunity for IEX is coming from the shift from bilateral contracts and PPAs to exchanges for energy procurement. The opportunity size for the short-term market is expected to be around 50 billion units.

- 20% of total volumes were purchased by industries.

- The company does see an opportunity to create emissions trading products like those in the EU.

- The potential GDAM market size is very big with the Govt looking to create 175 GW by 2022 and 450 GW by 2030.

Analyst’s View:

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company continues its growth march with another good quarter with volume growth of 43% YoY and sales & profit growth of 27% & 48% YoY. IEX continues to see increased participation from discoms in the exchange given the flexibility and competitive pricing as compared to bilateral contracts. This is the biggest opportunity for the company according to the management. It also expects the GTAM to continue its momentum due to the additional capacity expected to be generated by wind generators till Oct at least. It remains to be seen how the policies and regulations will evolve in the power sector and how IEX will fare with the addition of a new rival exchange in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q4FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 102 | 79 | 29.11% | 96 | 6.25% | 357 | 297 | 20.20% |

| PBT | 84 | 59 | 42.37% | 78 | 7.69% | 282 | 228 | 23.68% |

| PAT | 64 | 47 | 36.17% | 60 | 6.67% | 213 | 178 | 19.66% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 100 | 80 | 25.00% | 96 | 4.17% | 356 | 297 | 19.87% |

| PBT | 80 | 58 | 38% | 76 | 5.26% | 270 | 226 | 19.47% |

| PAT | 61 | 46 | 33% | 58 | 5.17% | 205 | 176 | 16.48% |

Detailed Results

- On a consolidated basis, PAT was up 33% YoY while revenue for the quarter was also up 25% YoY.

- FY21 saw an increase of 37.3% YoY in electricity exchange volumes. Q4 saw 62.1% YoY growth in electricity volumes.

- Digital transformation and new market segments – RTM and GTAM, were the key growth drivers for Company in FY21.

- Total installed power capacity in India grew 3.3% YoY to 382 GW. The renewable capacity saw 9% YoY growth with cumulative capacity to 94 GW in FY21.

- The REC trading remains halted in the quarter due to a stay order from APTEL (Appellate Tribunal for Electricity).

- The day-ahead market saw an average market clearing price of Rs 2.82 per unit in Q4 which was 6% down YoY.

- The real-time electricity market traded 3,766 MU in Q4 & 9,468 MU YTD.

- There was a 39.5% YoY growth in open access volumes.

- The green market cumulatively traded 785 MU during the year till date.

- The company retained its market shares of 92% in DAM+TAM, 99.9% in RTM, & 99.9% in GTAM markets.

- Share of exchanges in total electricity consumption has risen to 6.1% in FY21 from 4% last year. Share of exchanges in short term market has risen to 54% in FY21 from 41% last year.

Investor Conference Call Highlights

- In Feb 2021, the CEA laid down the procedure for approval and facilitation of cross-border trade of electricity. IEX has already started the commencement of the cross-border electricity trade on exchange with Nepal as of 17th April 2021.

- The company expects to start electricity trading with Bhutan & Bangladesh soon.

- It is also working to introduce longer-duration delivery contracts up to 365 days in both electricity and green markets.

- The latest date given by APTEL on the hearing for REC is July 14th.

- The management expects it to start no earlier than Q2.

- The company was looking to launch trading in Energy Saving Certificates or ESCerts market in Q3FY21 but was delayed due to the pandemic. It is now expected to commence in Q2FY22.

- The company is also expecting the launch of the LDC product to be in Q2 or Q3 in the year ahead. It has all the tech ready and is only waiting on regulatory approval to go ahead here. The company expects trade volumes of 25-30 BU from this forward contract platform each year.

- The RTM accounts for 13% of total volumes in FY21. It has risen to 17-17.5% in Q4. IEX is seeing increased participation coming from almost all the segments, which includes distribution utilities as well as open access consumers. Thus, the management expects this rising trend for RTM to continue to maybe 20-25% in the next few quarters.

- The company has already applied for Green day-ahead market contracts, but it doesn’t expect CERC to pass approval on this before the end of June. Thus, this product is also expected to be launched in Q2.

- The main market gains in RTM are from the DSM market where there are high penalties to overdrawing requirements and thus any pending or extra requirements are serviced by the exchange at a much lower price. To make up for the lost opportunity in DSM, the captive plant also has to come to the RTM, thus deepening the shift.

- The management states that the company wants to endeavour that 50% of the profit should be distributed in the form of dividends. But it has not given out any dividends in Q4 due to the uncertainty from COVID-19.

- The company is sitting on a cash pile of Rs 600 Cr.

- The GTAM market is expected to gain momentum going ahead as the summer season brings in additional generation from wind which is largely present in H1 and from more sellers joining in.

- All green generators are under some PPA. Most of them are small generators so the PPA in question is of smaller duration. IEX has over 10 such generators on the platform already. The company is not only targeting generators but also distribution companies that may have surplus green capacity.

- The cross-border trade has seen volumes go up to 5% of DAM. The volumes remain low here since the only mechanism allowed currently is spot market of fewer than 7 days. Anything greater than 7 days comes under bilateral contracts which is not under the exchange mechanism.

- The company is also expecting the RTM market to become the option for discoms as an immediate answer to demand-supply gaps that used to result in load shedding. Thus load shedding can become less frequent as discoms participate more in the RTM.

- The main use of the day-ahead market is to meet the deficit for discoms. The management believes that once the discoms see that they can service most of their requirements from the day-ahead market, they will come to it automatically to optimize their power costs.

- The management has stated that it will not divest any more of the pending 30% in IGX any time soon since it has 4 years to do so, and will only do so after deciding on the premium.

- The management states that it welcomes the formation and approval for the new exchange in the power sector as it should increase adoption of power exchanges and should be ultimately good for the expansion of the sector.

- The company launched an automated bidding option for the customers through the API. This was required as with the launch of RTM, the customers had to bid 48 times in a day. This auto bidding option has been adopted well by customers such that some large members have close to 60%, 70% of the cleared volume in the real-time market placed using this mechanism.

- Most of the tech initiatives by the company revolve around automation of the process to speed up customer response time and enhance customer experience. It has also provided customers with a web-based platform to provide a bidding option for all products and a mobile platform for the same. Both platforms are expected to enhance customer convenience and help gather data on customer behaviour and preferences.

Analyst’s View

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company continues its growth march with another good quarter with volume growth of 62% YoY and sales & profit growth of 25% & 33% YoY. It has also divested 47% of IGX till date and brought on NSE as a marquee investor in Q4. IEX continues to see increased participation from discoms in the exchange given the flexibility and competitive pricing as compared to bilateral contracts. It also expects the GTAM to gather additional momentum due to the additional capacity expected to be generated by wind generators in the summer season. It remains to be seen how the policies and regulations will evolve in the power sector and how IEX will fare with the addition of a new rival exchange in this space. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q3FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 96 | 69 | 39.13% | 79 | 21.52% | 256 | 218 | 17.43% |

| PBT | 78 | 53 | 47.17% | 62 | 25.81% | 198 | 169 | 17.16% |

| PAT | 60 | 42 | 42.86% | 47 | 27.66% | 150 | 131 | 14.50% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 96 | 69 | 39.13% | 79 | 21.52% | 256 | 218 | 17.43% |

| PBT | 76 | 53 | 43.40% | 58 | 31.03% | 191 | 168 | 13.69% |

| PAT | 58 | 42 | 38.10% | 44 | 31.82% | 145 | 130 | 11.54% |

Detailed Results

- On a consolidated basis, PAT was up 38% YoY while revenue for the quarter was also up 39% YoY.

- Q3 saw an increase of 61.8% YoY in electricity exchange volumes.

- Indian Gas Exchange secures PNGRB authorisation to become India’s first delivery-based Gas Exchange. Adani Total Gas & Torrent Gas become the first strategic investors in IGX by acquiring 5% stake each.

- The REC trading remains halted in the quarter due to a stay order from APTEL (Appellate Tribunal for Electricity).

- The day-ahead market saw good volumes growth of 43% YoY. The market witnessed an average market clearing price of Rs 2.76 per unit in Q3.

- Total volumes including REC rose 48.2% YoY.

- There was a 39.5% YoY growth in open access volumes.

- The Real-time electricity registered an all-time high monthly volume of 1129 MU in December.

- The green market cumulatively traded 473 MU during the quarter.

- The company announced an interim dividend of Rs 2.5 per share.

Investor Conference Call Highlights

- IEX successfully introduced 2 new contracts (daily and weekly) in the green market.

- It also signed a licensing agreement with MCX to launch electricity derivatives in the market using IEX price as a clearing.

- The national energy consumption increased 7% YoY in Q3.

- As on 31st December 2020, the installed power capacity in India was at 375 GW with a growth of 1.8% YoY. The renewable capacity grew 6% YoY.

- On Dec 4th 2020, the Ministry of Power introduced a draft proposal to enable distribution utilities to exit from the power purchase agreements after completion of the term of the PPA. This initiative will enable more buying by the utilities and sale of power by the generators on the exchange platform.

- The REC market used to have transactions of around Rs 80-90 Lacs a year for IEX.

- The management has clarified that IEX is only looking for strategic partners to invest in IGX at the moment.

- The increase in the open access volume is 14% YoY in Q3 and it formed 24% of total volumes in the quarter. Majority of the open access is traded through day ahead market only.

- The remaining 76% volumes are all from distribution companies.

- Although there is an opportunity for monetizing of software that IEX owns, the management has stated that IEX will not be doing so as the best way to make money with the software is to maintain it as the USP of the exchange.

- The electricity derivative by MCX is still pending approval from regulators. These derivatives will be physically settled on IEX platform and financially settled using IEX price.

- The main business development activity for IEX is to create awareness about the platform and values that it provides energy at.

- In the green market, the sellers are mainly distribution companies, distribution companies of Telangana and Karnataka. As the demand in these discoms is rising the volumes to be sold is coming down. The green market clearing price is between Rs 3.5-4.

- Annuals fees collected in Q3 was at Rs 4.2 Cr which was flat QoQ. This is because the number of participants is not increasing but the volumes are. Top 10 DISCOMs contribute almost about 75% to 80% of the total buy.

- IEX is looking to maintain a significant stake in IGX within permissible levels and will bring it down to 25% in the next 5 years.

- Participation in exchange is increasing mainly due to the flexibility and the competitive pricing offered as compared to bilateral traders contracts which have fixed terms for price and quantum.

- The main hurdles in the growth in adoption of the gas exchange are the absence of a uniform tax system for gas which is not under GST, gas transportation tariffs and almost no spare capacity in active LNG terminals.

- The company is seeing more and more states making power available as open access as it contributes to ease of doing business and thus IEX is seeing more states doing so to promote industrial activity in their territories.

- The company has filed a petition with CRC for long duration contracts and is waiting for the result. In the case of cross border activities, it will be dependent on whether the Govt of India will approve to do so with neighbouring countries.

- The top 3 states for open access are Gujarat, Tamil Nadu and Telangana. In many states, the breakeven rate for open access is around Rs 2.8-3.4 depending on various charges like cross-subsidy surcharge, transmission charges, billing charges, etc.

- The management has stated that there is scope for volumes rise in states like Andhra Pradesh, Maharashtra and Gujarat as there may be power plants here which have variable costs higher than exchange clearing price and thus there is an opportunity for cost savings here. On the other hand, such opportunities are low in states like Chhattisgarh, Orissa, West Bengal where the variable costs are very low due to plants located near RM sources.

- The company has kept transaction charges constant for the last 8 years at INR 0.02 from the buyer and INR 0.02 from the seller.

- The company will be looking to do a lot of marketing awareness with the participants to bring enough liquidity in long-duration contracts and GDAM when they are launched. Once these products reach sufficient liquidity and the market evolves, the company will look to develop new products.

Analyst’s View

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. The company has seen a good quarter with its highest ever volumes traded on the platform and sales & profit growth of 39% YoY. It has also gotten approval for IGX and has already gotten strategic partners like Adani Total Gas and Torrent Gas to invest 5% each in it. IEX is also seeing increased participation from discoms in the exchange given the flexibility and competitive pricing as compared to bilateral contracts. It remains to be seen how the policies and regulations will evolve in the power sector and how the issues capping the gas sector in India will be resolved in the future. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q2FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 79 | 79 | 0.00% | 81 | -2.47% | 160 | 148 | 8.11% |

| PBT | 62 | 61 | 1.64% | 58 | 6.90% | 120 | 115 | 4.35% |

| PAT | 47 | 49 | -4.08% | 43 | 9.30% | 90 | 88 | 2.27% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 79 | 79 | 0.00% | 81 | -2.47% | 160 | 148 | 8.11% |

| PBT | 58 | 61 | -4.92% | 56 | 3.57% | 115 | 115 | 0.00% |

| PAT | 44 | 49 | -10.20% | 42 | 4.76% | 86 | 88 | -2.27% |

Detailed Results

-

- On a standalone basis, PAT was down 4% YoY while revenue for the quarter was flat YoY largely on account of a fall of 20% YoY in power prices.

- Q2 saw an increase of 13.2% YoY in exchange volumes due to a rise in overall energy consumption.

- Consumption has risen and there has been a 4.6% YoY increase in energy consumption in Sep ‘20.

- The REC trading was halted in the quarter due to a stay order from APTEL (Appellate Tribunal for Electricity).

- The day-ahead market saw good volumes on the sell-side with sell volumes at 2.2x of cleared volumes which led to a 20% YoY decline in power prices.The market witnessed an average market clearing price of Rs 2.53 per unit during the quarter as compared to Rs 3.15 per unit in Q2FY20.

- There was a 39.5% YoY growth in open access volumes.

- A new market segment Green Term-ahead Market (G-TAM) was launched on August 21, 2020.

- The Real-time electricity market (RTM) traded 2,350 MU in Q2FY21. It crossed a cumulative volume mark of 3 billion units.

Investor Conference Call Highlights

- The company did an equity infusion into IGX and has filed an application for approval with the PNGRB, who is the gas regulator in India.

- The total installed power capacity of India has risen to 373 GW which is a rise of 3% YoY.

- Power demand is back to pre-covid levels in September.

- The company filed a petition with CERC for approval to commence trade in the long-duration delivery-based contracts. CERC is expected to give its approval only after the jurisdiction issue is solved in the Supreme Court.

- The Supreme Court hearing mentioned above has been postponed to the first week of December.

- There are a number of issues that have hampered the expansion of IGX such as gas transportation tariff, not GST for gas which means that each state has a different tax rate, Fewer enablers in place as compared to the electricity market.

- The demand for gas remains robust and intact. This is evident from the fact that both of the company’s regasification terminals by Petronet & Shell are working at near 100% capacity.

- The management has stated that the opportunity in the gas exchange space is much bigger than that in the electricity exchange space.

- The company’s volumes in TAM have dried up and shifted to the RTM market. Because of the competitive price offering, many state distribution agencies are also purchasing increasing quantities from the RTM platform.

- Long-term duration contracts should not cannibalize the TAM market rather it is expected to take away volumes from the bilateral market.

- The management has clarified that the DEEP platform is only used for price discovery and it does not enable future delivery, financial and physical settlement while in the case of the long term duration contracts, all of the background work of future delivery, financial and physical settlement is also taken care of by the platform.

- The verdict from APTEL on REC trading is expected to come on 28th

- The company has seen an increase of 10% in manpower costs mainly due to the annual increment impacts and larger workforce needed to operate the 24-hour market.

- GAIL is interested in acquiring 26% of IGX but according to regulations, it can only acquire a max of 5%. The company is also looking at other strategic buyers to come in and invest in IGX and bring down its holding to the required levels.

- The management has stated that the participation of all states has increased and particularly Punjab has been seeing more demand during this season. Large states like Maharashtra, Telangana, Tamil Nadu, and others have also seen good demand and participation as overall power consumption is rising.

- Currently, the short-term market is almost about 11% of the total generation. IEX’s share used to be around 35%-40% market share. Of this, the short-term market has risen to 50% in H1FY21.

- The management believes that on the introduction of long-term contracts, IEX will be able to address around 70-75% of the market. On the introduction of the financial contract, which would be similar to banking, the company will be able to address the whole 100% of the power market in India.

- The management has clarified that there is no other product available in the market which can meet the demand from the REC volumes from IEX. CERC has revised the forbearance price and the base price from Rs 1,000-2,400 to Rs 0-1,000 which is expected to attract a lot of industrial consumers and captive industries.

- The management has clarified that NTPC is not the one selling in RTM. NTPC has to allocate all of its power to the states which in turn are allowed to sell the excess to the RTM whenever required.

- The management feels that all the underproduced power should also be allowed to be sold on the DAM market to boost liquidity but it has not been accepted by the regulator and the government so far.

- The management is confident that the MBED provision mandating all power transactions through the exchange for 100% of the power generators (which requires uniform power pricing throughout the country) will not be taking place in the future.

- Open access volumes for H1 were up almost 40% YoY. This was mainly due to the low clearing price which was at Rs 2.50 vs Rs 3.15 last year. But open access is still being hampered by states through tariff and non-tariff barriers. Open access volumes now account for 23-24% of total volumes.

- Every day almost 400 participants participate in the real-time market including institutional buyers and DISCOMS.

- There are almost 40 participants in the GTAM market every day. The clearing rate in the green market is almost about 70%, 80% more than that rates cleared in the conventional market. Earlier states were backing down the green generators when the demand was less. Now they have a market to sell that power instead of backing down the generators.

- The annual fees collected in Q2 was at Rs 4.46 Cr.

- On the draft merit order dispatch from states, it says that if there is any shortfall in demand from long term contracts, it can purchase power from exchanges. That is – If the exchange clearing price is lower than the variable cost of some of the plants under the long-term contracts, the entity should back down the power from those costly plants and purchase power from the exchange.

- The management has clarified that transaction fees have remained the same and are not dependent on the clearing price at all. The main reason for volume growth to outpace revenue growth is that REC volumes have stalled. REC contributed to almost 12-13% of revenues for the company.

- On average, other expenses would be at Rs 5-6 Cr per quarter.

- The management reiterates that it doesn’t expect market coupling to come into place and even if it does there shouldn’t be any issues for having different prices in different exchanges just like in the case for BSE & NSE for equities.

- The entire renewable capacity is tied up under the long-term contract. So most of the participation in the GTAM is done by the distribution companies who have got surplus renewable power generation beyond the RPO application.

- Currently, the major participants in GTAM are Karnataka and Telangana and the management expects states with large renewable capacity like Andhra Pradesh, Gujarat, Rajasthan, and Maharashtra to start participating soon.

- Short term market has stayed at 10-11% of the total market for the last 4-5 years and the govt is working hard to increase liquidity in this space. One of the measures taken is that long-term PPAs are not happening. Another source for rising in demand for short term market will the phasing out of old plants which service long term contracts. When these plants will be phased out the unaddressed demand will have to fulfilled using the short-term market. Thus the management expects the market size of the short term to rise to almost 15% in the next 2-3 years.

- The management reassures that even if market coupling takes place, given the company manages to defend its market share, its overall volumes will rise drastically which will ultimately be good for IEX.

Analyst’s View

IEX is the first and largest energy exchange in India providing a nationwide, automated trading platform for physical delivery of electricity, Renewable Energy Certificates, and Energy Saving Certificates. It has a very asset-light business model and a strong Balance Sheet. In the last several years it has done well by constantly adding new products and improving offerings for the participants on its platform. With the share of renewable energy rising in total energy consumption, and the launch of the GTAM market, the future of IEX looks very exciting. However, it seems that competition in this sector is also increasing at a rapid pace. It remains to be seen how the whole COVID episode plays out and how will the supreme verdict on the derivatives on power will go. However, the company seems to have the financial muscle to tide over the disruption of COVID and also launch new segments as it goes along. It is still very early days in the power exchange market. However, as of date, IEX looks like a pivotal player in this industry.

Q1FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 81 | 70 | 15.71% | 79 | 2.53% |

| PBT | 58 | 55 | 5.45% | 59 | -1.69% |

| PAT | 43 | 40 | 7.50% | 47 | -8.51% |

| Consolidated Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 81 | 70 | 15.71% | 80 | 1.25% |

| PBT | 56 | 55 | 1.82% | 58 | -3.45% |

| PAT | 42 | 40 | 5.00% | 46 | -8.70% |

Detailed Results

-

- On a standalone basis, PAT was up 7.5% YoY while revenue for the quarter was up 16% YoY largely on account of the increase in overall volumes.

- Q1 saw an increase of 14.5% YoY in exchange volumes despite overall energy consumption declining 16% YoY.

- Exchange power prices were down 26% YoY which yielded significant savings for distribution utilities and Industries.

- Consumption started rising towards June which saw rise 28.7% MoM.

- The newly launched real-time electricity market commenced on 31st May 2020 and now accounts for 10% of total volumes.

- The Indian Gas Exchange commenced operations on June 15, 2020 and traded a total of 9600 MMBTU of gas within the first 15 days of launch.

Investor Conference Call Highlights

- Renewable capacity in the domestic space grew 10% YoY while thermal production contracted 23% in the same period.

- The company made a contribution of Rs 5 Cr to COVID CARES fund and had a tax liability of Rs 2.6 Cr. Without these non-recurring items, PAT growth would be at 18% YoY.

- On July 10th Ministry of Power released an office memorandum that should facilitate the introduction of long-duration power contracts. The longer-duration, delivery-based forward contracts, and derivative contracts are expected to alter the way power is procured in our country because you get a hedge over a long period of time.

- The company hopes to launch long-duration power contracts in Q3.

- The management is clearly seeing the need for derivative at this stage because the dependence of Discoms in the stock market is increasing.

- The company is going to launch the forward market in the IEX platform while it is looking at other options for the pure financial product where the company may need to float a new company to operate it.

- The management has stated that derivative volumes are higher than spot volumes everywhere around the world and this should also be the case here.

- The company is expecting the market size for the forward & futures combined to be around 20 billion units.

- IGX is currently owned 100% by IEX and GAIL has issued an expression of interest to invest 26%. There are also other proposals and inquiries from big gas players in the works currently.

- The company wats to maintain a majority shareholding of at least 51% in IGX at the end.

- There is indeed a regulation that states that a neutral player should hold 15% at most. The company is reviewing the situation and looking to talk to the regulator regarding this.

- The management has maintained a neutral stance on the issue of power coupling which was included as a provision in the draft of PMR 2020.

- The management has stated that the transaction margin cannot be changed easily and needs approval from CERC to be changed in any direction.

- The long duration derivative contracts will be under SEBI and the company is looking to collaborate with the exchange in India to make this new company to launch energy derivatives. The company will also be formed such that all delivery happens on IEX.

- The management has stated that cash-settled electricity futures will also be available and these can also be converted to electricity on the spot.

- Currently, the company has a weekly contract as the longest contract. With the launch of the longer duration contracts, the company will be looking to offer monthly, quarterly, and annual contracts.

- The intraday market has been cannibalized by the RTM market. Around 80-90% of volumes have shifted.

- The REC fee in Q1 was at Rs 4.35 Cr.

- TAM volumes accounted for less than 5% of total volumes.

- The management expects that every buyer would want to play in the whole basket to figure out what is the optimum procurement program for themselves.

- The management has stated that if the 3 functions of the price coupling operator, the exchanges & clearing, and settlement mechanism need to separate, then the company can easily do so.

Analyst’s View