About the Company

EaseMyTrip is an Indian online travel company, founded in 2008 by Nishant Pitti, Rikant Pitti, and Prashant Pitti. Headquartered in New Delhi, the company provides hotel bookings, air tickets, holiday packages, bus bookings, and white-label services. EaseMyTrip has overseas offices in Singapore, Dubai, Maldives, and Bangkok.

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results:

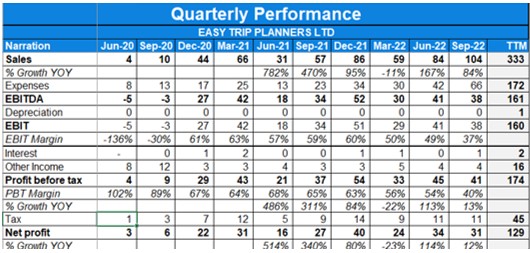

- The company booked a revenue of INR 8050.6 Crores.

- The company reported a significant growth of 116.7% in Gross Booking Revenues (GBR) in FY2023 compared to FY2022, reaching INR 3715.6 Crores.

- Despite a weak quarter in Q4 FY2023, the company achieved sustained growth with an 83.0% year-on-year increase, reaching INR 2143 Crores.

- Adjusted revenues in FY2023 grew by 68.6% to INR 675 Crores compared to INR 400 Crores in FY2022.

- Easy Trip Planners experienced successful business operations in Dubai, surpassing INR 100 Crores in GBR within the first year.

- The company maintained efficient cost management, with marketing spend as a percentage of GBR at 1% in FY2023.

- In the air travel segment, Easy Trip Planners sold 1.15 Crores air tickets in FY2023, a significant increase from 70.9 lakhs in FY2022.

- The hotel segment saw substantial growth, with a 121% increase in hotel night sales compared to FY2022.

- Easy Trip Planners achieved consistent profitability, with an EBITDA of INR 191 Crores in FY2023, a 30.2% increase from the previous fiscal year.

Investor Conference Call Highlights

- Easy Trip Planners expanded its presence by opening a franchise store in Patna, Bihar, to enhance customer service and cater to travel needs.

- The launch of the EMT Royale program offered exclusive and personalized services to elite customers, strengthening customer experiences.

- Strategic partnerships were formed with various entities, including UP Warriorz team in the Women’s Premier League, Swiggy, HT Digital, Chennai Blitz, and the Andhra Pradesh government, boosting brand presence and exposure.

- The company has experienced a significant increase in trade receivables primarily due to the growth of its B2B business and corporate business. The trade receivables have increased from INR 52 Crores to INR 155 Crores.

- The company aims to achieve higher double-digit growth in its Gross Merchandise Value (GMV) for the coming year, following a growth rate of 116% in the previous year.

- The company is making concentrated efforts to expand its overseas business. The average ticket size in overseas markets can be up to three times higher than in India, and the competition is manageable due to the absence of convenience fees charged by other OTAs.

- The company expects its margins to improve as the cost of operations does not necessarily grow at the same rate as business expansion. Payment gateway charges are expected to diminish as UPI becomes more prevalent in the country.

- The company anticipates employee costs to reduce as the business continues to improve, although marketing costs will remain around 0.9% to 1% of GMV.

- The company aims for a minimum GMV growth of 50% for the current year.

- The take rate (interplay between the company’s take rate and customer discounts) has stabilized between 8.2% and 8.7% in the last five quarters, and the company expects this to continue in the future. The growth of the hotel sector, which has a higher take rate, has a minimal impact on the overall take rate due to its single-digit contribution to the company’s revenue.

- The cost items have not increased disproportionately compared to revenue growth. Employee costs, marketing and promotion costs, and discounts have remained stable or decreased on a yearly basis. The company has been able to achieve over 100% business growth even after reducing discounts significantly.

- The company’s current focus is to grow its hotel business at a break-even pace, which explains the notional loss reported. The commissions received from hotels are passed on to customers in the form of discounts.

- The company has made acquisitions such as YoloBus and one in the hotel segment. The financials of these acquisitions may be included in future presentations to provide visibility on their performance.

- The Spree Hospitality business is growing profitably, adding around 5 to 6 hotels every quarter. YoloBus is still in the early stages but has shown potential for breakeven. The company is waiting for YoloBus to achieve profitability before further expansion.

- There is an outstanding receivable of INR 69 Crores from GoAir. The company is hopeful that GoAir will resume operations, and the outstanding amount will be adjusted with sales once operations restart.

- The decrease in hotel revenue in the current quarter compared to the previous one is attributed to the cyclical nature of the travel business, with Q3 being stronger due to holiday seasons. The company’s hotel business is growing at a break-even pace.

- The fluctuation in PAT margins as a percentage of revenue is explained by the inclusion of discounts offered to customers. The company suggests looking at PAT as a percentage of Gross Booking Revenue (GBR) for a more accurate representation of profitability.

- Employee expenses were higher in the quarter due to annual increments given in December, as per company policy.

- Marketing expenses increased due to tie-up with the Woman Premium League, which was not present in the previous quarter.

- The company experienced negative operating cash flow for the first time, attributed to increased trade receivables and advances given to airlines and hotels.

- The segment contract liability on the balance sheet increased four times, representing advances received from ITQ and agents in the B2B business.

Analyst’s View

The company offers a comprehensive range of travel – related products and services under the flagship brand ”Ease My Trip”.

It also provides end- to -end travel solutions, including airline tickets, hotels and holiday packages,rail tickets, bus tickets and taxis as well as ancillary value- added services such as travel insurance, visa processing and tickets for activities and attraction.

EaseMyTrip plans to grow its GMV in the higher side of double digits for the coming year and expects its GMV to grow by more than 50% for the corresponding year. The company is making concentrated efforts to grow its overseas business and expects to generate north of INR 700-800 crores from all the newer operational areas in the next couple of years.

The company’s core focus continues to be on creating value, driving profitability, and delivering exceptional service to its customers. As part of its growth strategy, the company is exploring opportunities to expand its product offerings by introducing additional insurance products. With a large consumer base and a robust B2B network, the company aims to leverage these strengths to tap into the insurance market.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

- Revenue growth of 52% YoY.

- Adjusted Revenue grew by 29% while PAT grew by 4% for the quarter.

- Gross Booking Revenue (GBR) reported stands at Rs. 2267 cr up 75% YoY.

- In % of GBR terms, discount to customers stood at 3.1% of GBR, but in absolute terms, it increased to Rs.70.1cr up from Rs.60.6cr last year.

- As a % of GBR Marketing expenses increased to 1.5% from 0.9% while other expenses remained stable.

- Manpower costs as a percentage of GBR has slightly increased to 0.6% of GBR as compared to the corresponding quarter’s level of 0.5% of GBR

- Operational Performance:

- Flight Bookings – up 31% YoY

- Hotel Nights – up 88% YoY

- Trains, Buses & others – down 7%

- Consolidated EBITDA Margins stood at 42.1% Vs 61%.

Investor Conference Call Details:

- The company’s Travel Utsav Festival Sales were a great success exceeding Rs. 555 crores between October 6th and 23rd.

- Recently, the Company introduced a robust referral-based reward program, EMT Pro, that aims to reward loyal with a refer now and earn forever scheme.

- The company Company launched 2.0 Self-Booking tool for corporates which uses AI, Machine Learning, and Data Mining technologies to become more efficient and resourceful.

- During the quarter the Company collaborated with MobiKwik Zip, India’s leading “buy now, pay later” platform to enable users to book their travel today and pay at a later date, all the while gaining attractive discounts

- The company signed a GSA with Go First to exclusively sell, promote and market passenger tickets to passengers in Saudi Arabia.

- On the marketing front, the company became the official travel partner for the first World Tennis League held in Dubai and the official travel partner for IIFA Awards 2023 to be held in Abu Dhabi.

- The company acquired Gujarat’s GIFT city-based Nutana Aviation which leases charter aircraft, enabling operators to run efficiently, along with providing charter booking services to its clients. The acquisition will add a new revenue stream and help develop EaseMyTrip into a comprehensive travel ecosystem.

- In order to strengthen its hotel booking portfolio, the company recently acquired a majority stake in CheQin. CheQin is a first-of-its-kind real-time marketplace for hotel booking, which allows travelers to bargain directly with the hoteliers over the prices of the room.

- During the quarter, 84% of total volumes were sold in B2C segments, 14% in the B2B2C segment, and the remaining in B2E segments.

- The employee expenses have risen owing to higher additions due to acquisition.

- The other expenses rose due to higher commissions paid for the B2B2C segment.

- The management believes the listing on the stock exchange has helped in improving the company’s brand image & reputation leading to higher market share despite lower discounts.

- The company’s rationale for the Nutanna acquisition was to capture the market of $2 to $3 billion, which exists for non-scheduled aircraft.

- The management states that CheqIn (its new acquisition) will provide technology that could be of tremendous use, specifically for the last-minute booking, when a hotel is occupied 80% to 90%, and if they can get an additional last-minute booking at a substantially higher/lower price as well.

- The management, when asked about sustaining margins, said “The EBITDA margin should continue to go up because the revenues can increase exponentially, but the cost should only go up algorithmically and that is why internet companies are valued so better.”

- Spree hospitality is profit-making, and at the time of acquisition, it had about 12 hotels. And now it has about 28 hotels in its portfolio & The target is to keep adding five new hotels every quarter.

- The management is very bullish on the Indian travel ecosystem is that there is no other country in the world which can say that there are 66 new airports that are going to come in the next decade, except for India.

- The company is targeting PAT of 500 Crs in the next 3-4 years.

- Air travel portion to total revenues stood at 89%.

- The company operates its hotel business in a very unique way, through channel partnerships with aggregators, which enables it to provide the best room rates in the industry, because of this its hotel business is increasing manifold on a year-to-year basis. It is a huge differentiator as this model itself allows to keep adding more and more aggregators so that prices keep going down, Not because of heavy discounting but because there are multiple parties who are contesting for its business by reducing their price for any particular hotel via the aggregator model.

- The quarter’s profit for spree stood at 30 lakhs.

- The promoters put in only Rs.15 lakh of their own capital in the Company during the first five years of EaseMyTrip.

- The company is the only OTA in India, that runs its own call center.

- The management states that “ having an extra insurance that people would get their money back if they fall sick, 100% money would be refunded by EaseMyTrip is that it’s absolutely a big reason why people are switching to EaseMyTrip over others”

Analyst Views:

Ease my trip is the second largest OTA player in air travel booking segment.It reported mediocre results with revenues growing decently while margins collapsing due to higher expenses. It recently acquired two companies namely CheqIn & Nutanna which will help in improving its exisitng service profile.The company is backing on its ability to grow several verticals within its business which can provide it with its next leg of growth. It is focussing on its Hotel business and have a target to of 200 Hotels which they hope to achieve in the next 5 years, it is looking to expand services in the International market, the optimism of which is corroborated by the MoM growth in the Middle East business. For growing businesses and new verticals, management’s way of growing at break-even can be justified to an extent. The only thing probably supporting its high valuation currently is the growth leaving room for only a small margin of error. Going forward the thing to look out for would be the competition in the space and operating leverage playing out.

Q2 FY23 Updates

Financial Results & Highlights

Detailed Results:

- Revenue growth of 68% YoY.

- Strong growth in Revenue of 40% and PAT of 44% on QoQ basis.

- Gross Booking Revenue (GBR) reported stands at Rs. 1977 cr up 121% YoY and 42% QoQ.

- Air segment booking increased by 52%.

- In % of GBR terms, discount to customers fell to 3.1%% from 4.9% YoY, but in absolute terms, it increased to Rs. 60.6cr up from Rs.44.2cr last year.

- As a % of GBR Marketing expenses increased to 1.5% from 0.9% while other expenses remained stable.

- Operational Performance:

- Flight Bookings – up 52% YoY

- Hotel Nights – up 70% YoY at 77,919

- Trains, Buses & others – up 12% YoY at 137,326

- EBITDA Margins stood at 35.9% Vs 61.7% due to high one off marketing expenses

Investor Conference Call Details:

- The company launched launched ‘Travel Utsav’ festival between October 6th and 23rd of October, which helped record the highest gross sales of> Rs.555 crores for the Company.

- The Company became a Co-Powered sponsor of Asia Cup Cricket 2022 which had an estimated collective viewership of more than 4.9 billion.

- EaseMyTrip became the presenting partner for Road Safety World Series Tournament of 2022.

- The company spent one-time costs of Rs. 13 crores on these marketing initiatives.

- The company is taking various initiatives to increase its presence abroad including partnering with SpiceJet Airlines through its Thai subsidiary to sell tickets and other services to customers in Thailand.

- The management expects marketing expenses to remain at 0.6-0.9% of GBR in the future Vs 1.5% in the current quarter.

- The revenue from the hotel segment decreased despite an increase in bookings due to higher discounts provided to the customers.

- The company targets flight: non-flight revenue split of 70:30 after which it plans to start focusing on profits in the non-flight segment by decreasing the discounts offered.

- The seasonally strong quarters are Q1 & Q3 due to vacations. Despite that, the company grew 20% QoQ owing to a market share increase.

- The company’s trade receivables increased by Rs.45 Crs due to higher shares from corporate & travel agents as a part of its long-term strategy.

- The liability increased by Rs.70 Crs on account of advances received from ITQ & GDS which provides some part of the commission to be received by the company in advance.

- The Payment gateway charges are directly proportional to the GBR & this corollary is expected to decrease due to the increased adoption of UPI.

- The company expects to make good grounds & potentially disrupt foreign markets owing to higher service & convenience fees charged by the incumbent firms.

- The company is seeing good progress in its acquisitions with A) Spree hotels increasing from 12 to 27 properties post acquisition & generating 20-30 lakhs profits on a monthly basis & B) the valuation of Yolo bus increasing to Rs.100 in the last funding round vs Rs.2 Crs at which the company was acquired.

Analyst Views:

The company is backing on its ability to grow several verticals within its business which can provide it with its next leg of growth. It is focussing on its Hotel business and have a target to of 200 Hotels which they hope to achieve in the next 5 years, it is looking to expand services in the International market, the optimism of which is corroborated by the MoM growth in the Middle East business. For a growing businesses and new verticals, management’s way of growing at break-even can be justified to an extent. The only thing probably supporting its high valuation currently is the growth leaving room for only a small margin of error. Going forward the thing to look out for would be the competition in the space and operating leverage playing out.

Q1 FY23 Updates

Financial Results & Highlights

| Standalone financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 87.7 | 34.8 | 152% | 64 | 37% | 247 | 151 | 63.6% |

| PBT | 45 | 21.1 | 113% | 33 | 36% | 145 | 85 | 70.6% |

| PAT | 33.6 | 15.7 | 114% | 24 | 40% | 107 | 62 | 72.6% |

| Consolidated financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 91.4 | 34.7 | 163% | 65 | 40% | 250 | 151 | 65.6% |

| PBT | 44.4 | 20.8 | 113% | 32 | 38% | 143 | 83 | 72.3% |

| PAT | 33.1 | 15.4 | 114% | 23 | 44% | 106 | 61 | 73.8% |

Detailed Results:

- Revenue growth of 163% YoY was on a low base due to Covid 2nd Wave last year.

- Strong growth in Revenue of 40% and PAT of 44% on QoQ basis.

- Gross Booking Revenue (GBR) reported stands at Rs. 1663 cr up 350% YoY [Covid effect] and 42% QoQ.

- In % of GBR terms, discount to customers fell to 2.6% from 4.9% YoY, but in absolute terms it increased Rs. 44cr up from Rs.17cr last year.

- As a % of GBR, Employee expense, Marketing expense and other expenses remained stable.

- Operational Performance:

- Flight Bookings – up 9% QoQ at 2.2M [30% Volume from International]

- Hotel Nights – up 157% QoQ at 71,791

- Trains, Buses & others – down 12% QoQ at 160,540

- EBITDA Margins lower both YoY and QoQ at 49.7%, driven by higher employee expenses and other expenses. [Reason: Point 6 below]

- Launched co-branded credit card in partnership with Standard Chartered Bank as a part of marketing initiative.

Investor Conference Call Details:

- Set-up EaseMyTrip New Zealand as a wholly owned subsidiary.

- GMV from Middle East Office stood at Rs.7 cr for the quarter. Majority of it is from air bookings.

- ME operations started from April. Monthly GMV – April: 84 Lakhs | May: Rs. 1.2 cr | June Rs.5 cr.

- Backoffice operations to be handled from India itself, unless issue of language barrier comes up, like in case of customer call centres.

- At current quarter run rate, expect GBR to touch around Rs. 7000 cr.

- Many International routes are still not operating. With more routes opening and relaxing of Covid-related rules will help the Flight bookings.

- Expect to expand to 200 hotels in the next five years. Currently the figure stands at 23 Hotels.

- Regarding YOLO acquisition: Aim to provide premium segment of buses. Will help bus operators to improve the condition of the bus, install GPS Trackers and as a whole provide a comfortable ride to customers.

- YOLO revenues have started to come in from July.

- This quarter take rate was at 5.3%. Adjusted revenue figure affected by discounts. [Adjusted revenue figure affected by discounts.]

- When discounts are given, convenience charges levied and vice versa, this set-offs each other and take rates on net revenue basis are maintained around 5%.

- Take rates of Industry has declined by 0.9% but EMT has been able to maintain theirs.

- Payments Gateway charges to be looked at from GBR perspective because the charges are on the whole amount. Standard Rates 0.6% – 0.7%.

- Increase in other expenses is due to growth in B2B segment where commissions are paid to agents.

- Take rates on gross level are same for International and Domestic Flights. In absolute terms take rates are higher in international due to higher ticket prices. Higher margins will be driven by more business class bookings.

- OTA Market Share would be around 20%. Market share is in part a function of discounts which have been decreasing for EMT on % of GBR basis. [Down from 4.2% in Q3FY22 to 2.6% this quarter]

- With respect to competition from old player [Cleartrip] who is now backed by Flipkart – having sailed through many competition cycle, management is confident of protecting its market share and growing.

- Confident of its bootstrapped DNA to defend against competition as well as grow in a sustainable way. [Was bootstrapped with just 15 lakhs in funds for first 5 years, with no outside funding from banks or VC/PEs]

- Expect to grow 2x of the Airline Industry growth rate which is expected to grow at around 14% for the coming 2-3 years.

Analyst Views:

The company is backing on its ability to grow several verticals within its business which can provide it with its next leg of growth. It is focussing on its Hotel business and have a target to of 200 Hotels which they hope to achieve in the next 5 years, it is looking to expand services in the International market, the optimism of which is corroborated by the MoM growth in the Middle East business. For a growing businesses and new verticals, management’s way of growing at break-even can be justified to an extent. The only thing probably supporting its high valuation currently is the growth leaving room for only a small margin of error. Going forward the thing to look out for would be the competition in the space and operating leverage playing out.

Q4 FY22 Updates

Financial Results & Highlights

| Standalone financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 64 | 69 | -7.2% | 89 | -28.1% | 247 | 151 | 63.6% |

| PBT | 33 | 43 | -23.3% | 54 | -38.9% | 145 | 85 | 70.6% |

| PAT | 24 | 31 | -22.6% | 40 | -40.0% | 107 | 62 | 72.6% |

| Consolidated financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 65 | 69 | -5.8% | 90 | -27.8% | 250 | 151 | 65.6% |

| PBT | 32 | 42 | -23.8% | 54 | -40.7% | 143 | 83 | 72.3% |

| PAT | 23 | 30 | -23.3% | 40 | -42.5% | 106 | 61 | 73.8% |

Detailed Results:

- The company had an weak quarter with revenues de-growing by 6% YoY on consolidated basis.

- PAT decreased by 23% YoY on a consolidated basis.

- Gross booking revenue for this FY increased by 75% YoY whereas Air segment bookings increased by 56.9% YoY.

- Air segment & trains/bus segment saw transaction numbers growing by 13% & 59% YoY in Q4.

- Hotel nights (in numbers) de-grew by 15% YoY for Q4.

- The Board has recommended a bonus issue of 1:1.

Investor Conference Call Details:

- The company saw lower revenues were due to a reduction in discount income & commission which the company receives based on performance targets which couldn’t be achieved due to the Omicron wave.

- The management states that the overall market share should be north of 10% & for the online market, it should be north of 20%.

- The company is targeting double-digit growth in its hotel segment for the next 2-3 years.

- The management explains that the OTA can offer better discounts than captives due to tie-ups with several banks, credit cards & fin-tech companies who contribute a certain portion of the company’s discounts to the users.

- The company got lower convenience fees due to lower discounts offered.

- The management believes that since most of its competitors are loss-making & dependent on PE, VC funds unlike the company will be able to perform better at times of cash scarcity.

- The company gave an advance of Rs.40 Cr to airlines in FY22 to help the company get better commissions from the airlines.

- The management is very bullish about demand in the current year due to the pent-up demand of previous years.

Analyst Views:

Founded in 2008, EaseMyTrip is India’s 2nd largest online travel booking portal. The Q4 was impacted due to the omicron wave leading to lower discount & commission incomes coupled with the company missing its volume targets resulting in further lower commission income. The company is making good inroads into the travel industry and is looking to expand its influence in the sector with key acquisitions which help enhance its portfolio of offerings and help provide bundled services. The company has also taken various actions and introduced new policies like a full medical refund and others which are expected to help differentiate EasyTrip from the rest of the market. It remains to be seen how long it will take for normal travel behaviour to come back to pre-covid levels and whether the acquisitions and policy actions of the company will help it separate itself from the rest of the pack. Nonetheless, given the large market share in online travel bookings for EaseMyTrip and the steady revival of the travel sector in India, Easy Trip Planners is a pivotal stock to watch out for in the travel sector.

Q3 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 86 | 44 | 95.5% | 57 | 50.9% | 174 | 72 | 141.7% |

| PBT | 54 | 29 | 86.2% | 36 | 50.0% | 112 | 42 | 166.7% |

| PAT | 40 | 22 | 81.8% | 27 | 48.1% | 83 | 31 | 167.7% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 90 | 47 | 91.5% | 60 | 50.0% | 184 | 81 | 127.2% |

| PBT | 54 | 29 | 86.2% | 36 | 50.0% | 111 | 41 | 170.7% |

| PAT | 40 | 22 | 81.8% | 27 | 48.1% | 82 | 30 | 173.3% |

Detailed Results:

- The company had an excellent quarter with revenues growing by 91% YoY on consolidated basis.

- PAT increased by 81% YoY on a consolidated basis.

- Gross booking revenue for this quarter increased by 65% YoY whereas Air segment bookings increased by 49% YoY.

- Gross booking revenue for 9M increased by 108% YoY whereas Air segment bookings increased by 87% YoY.

- The key acquisitions for this quarter include

- Spree: A 1200 room-keys hospitality management company

- Traviate: India’s first B2B technology-driven travel marketplace

- YoloBus: A premium intercity mobility platform.

- Hotel nights sold saw a jump of 144% YoY in Q3.

- Train, bus & others segment grew by 162% YoY in Q3.

- The Board has recommended a bonus issue of 1:1.

Investor Conference Call Details:

- Yolobus has an asset-light business model and works with bus operators pan India. The company entered into a definitive agreement with YoloBus to acquire the brand name, technology, running business expertise, data, and the team of Yolo Traveltech Private Limited, operating under the name of YoloBus. The deal will be consummated within a month & it will be an all-cash deal.

- Spree Hospitality is a 1200 room-keys hospitality management company, to expand its presence in the hotel and holiday segment. It was acquired for Rs.18.25 Cr and profit contribution for December from this stood at Rs.12 lakhs.

- Key initiatives in this quarter includes full refund-medical policy, special airfare discount on waitlisted tickets & partnership with SpiceJet.

- Vijay Raaz & Varun Sharma were appointed as first brand ambassadors.

- Company is doing multiple tie-ups with various brands, banks & e-wallets.

- Margins for the current quarter increased due to change in product mix towards hotel & other services.

- Revenue from hotel bookings in the December quarter was low due to the 3rd covid wave.

- The current GBR is the highest in the company’s history.

- The company’s market share in the Air segment has increased from 7.5-8% to the north of 10% YoY.

- The management is very bullish about the next 2 years due to the high pent-up demand coupled with the pandemic almost reaching its ending phase.

- The company is planning to take benefit of synergies between the company itself and its new acquisition-Spree by leveraging its offering for providing a bundled service (like asking people booking a flight ticket to add a spree hotel stay by paying a little extra thus creating a bundled offering).

- The company’s acquisitions are primarily focused on acquiring asset-light fast-growing companies that have synergies with the company rather than being too much focused on payback from investment.

- The management wants to become the leader in the travel industry and not just create a platform, but also create the entire ecosystem on the travel side, where a lot of good companies are in the travel trade.

- The management is focused on ensuring the profitability of the company & maintaining an operating margin of 60% in the future as well.

Analyst Views:

Founded in 2008, EaseMyTrip is India’s 2nd largest online travel booking portal. The company has seen a very good recovery with bookings across all segments rising a lot YoY. The company is making good inroads into the travel industry and is looking to expand its influence in the sector with key acquisitions which help enhance its portfolio of offerings and help provide bundled services. The company has also taken various actions and introduced new policies like a full medical refund and others which are expected to help differentiate EasyTrip from the rest of the market. It remains to be seen how long it will take for normal travel behavior to come back to pre-covid levels and whether the acquisitions and policy actions of the company will help it separate itself from the rest of the pack. Nonetheless, given the large market share in online travel bookings for EaseMyTrip and the steady revival of the travel sector in India, Easy Trip Planners is a pivotal stock to watch out for in the travel sector.

Disclaimer

This is not a piece of investment advice. Please read our terms and conditions.