About the Company

Founded by Jaidayal Dalmia in 1939, Dalmia Bharat possesses India’s fifth largest installed cement manufacturing operational capacity of 30.75 million tonnes per annum (MTPA). This capacity is spread across 13 state-of-the-art manufacturing plants in nine States. Dalmia Bharat contributes ~6% of the entire country’s cement capacity. It has a brand portfolio of three marquee brands: Dalmia Cement,

Dalmia DSP and Konark Cement. These brands are available as Portland Pozzolona Cement, Portland Slag Cement, Composite Cement, and Ordinary Portland Cement in select markets.

Q4FY23 Updates

Financial Results & Highlights

Detailed Results:

- The average receivable as of March 31st was 700 crores.

- Gross debt increased by 623 crores on a full-year basis, closing debt as of March 31st was 3,763 crores. The net debt to EBITDA ratio was 0.29 time

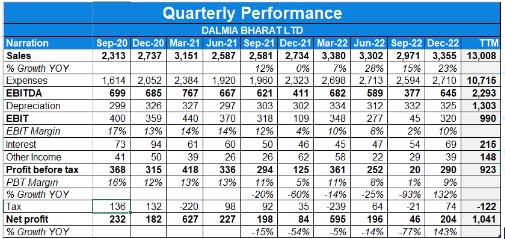

- Sales Volume for Q4FY23 increased 13.3% YoY to 7.4MnT, and 15.9% to 25.7MnT in FY23.

- Revenue for Q4FY23 increased 15.7% YoY to Rs 3,912Cr, and 20.0% to Rs 13,540Cr in FY23.

- EBITDA/T at Rs 951/T for Q4FY23 and Rs 900/T for FY23

- Net Debt/EBITDA stood at 0.29x.

Investor Conference Call Highlights

- The company expects GDP growth of 6.5% to 7% in FY24 and beyond. Dalmia Bharat Limited’s growth is expected to accelerate along with the growth of India.

- The company stated that capacity was increased by 15% from 35.9 million tons to 41.1 million tons per annum.

- The company accrued Rs. 92 crores of incentives in the quarter, with total accrual for FY23 at around 272 crores

- The company signed a definitive agreement for the acquisition of 2.2 million tons of cement capacity at Bhilai and 3.3 million tons of clinker at Babupur and Jaypee Super.

- The company is proposing a long-term lease agreement for the Nigrie Cement capacity of 2 million tons with an option to purchase within 7 years for an enterprise value of Rs. 250 crores.

- The company anticipates strong cement demand upcycle in the pre-election year 2024, with industry demand expected to grow from 8% to 9%.

- Deferred the 2.5 million tons Grinding unit expansion in Bihar, resulting in a revised expansion plan of 46.6 million tons organic capacity and 56 million tons total capacity by FY24.

- The company achieved industry-leading volume growth of 15.9% YoY.

- – Improved operating metrics, such as increased CC ratio and renewable energy consumption, while reducing carbon footprint.

- The company is committed to environmental goals, including RE100, EP100, and EV100 by 2030, and carbon negative by 2040.

- Sameer Nagpal has been appointed as the Chief Operating Officer of the company. He was previously the CEO of Dalmia Bharat Refractory and played a crucial role in growing the business and leading the refractory business’s M&A transaction.

- In FY23, the company achieved volume growth of 15.9% and revenue growth of 20% YoY, with regions like east, northeast, west, and south delivering double-digit volume growth.

- The quarter saw the highest-ever sales volume and revenue, with 7.4 million tons of volume and revenue of Rs. 3,912 crores.

- The company stated that NSR (Net Sales Realization) growth was around 4%, driven by price stability and strengthening in the East and Northeast states.

- There was a variation in inventory levels on a quarter-to-quarter basis due to factors like seasonality, plant shutdowns, and repair work.

- The company stated that EBITDA per ton for the full year was Rs. 900, with an exit EBITDA of Rs. 951 per ton in Q4.

- The company stated that the blending ratio improved from 79% in FY22 to 84% in FY23, reaching an all-time high of 88% in Q4.

- The company stated that renewable energy capacity increased from 17 MW in FY19 to 166 MW by FY23 and targets doubling it to around 324 MW in FY24.

- The company stated that sales of premium products improved by 19% to 3.4 million tons in FY23.

- The company stated carbon footprint was reduced to 463 kg per ton, one of the lowest in the global cement industry.

- The company will focus on utilizing capacity efficiently and stable pricing in the East market.

- The company commercialized 2.7 million tons of capacity in the east and northeast regions, reaching a closing cement capacity of 38.6 million tons in FY23.

- The company recently commercialized a new cement line at Bokaro with a 2.5 million tons capacity, taking the installed capacity to 41.1 million tons.

- Murli plant has built limestone visibility of 18 to 20 years, with capacity utilization expected to reach over 60% in FY24. Cost initiatives at the Murli plant include commissioning WHRS of 7 MW and solar capacity of 4.5 MW, as well as addressing coal leakage. Successful turnaround of the Kalyanpur plant, now one of the most profitable plants in the eastern operations, with WHRS and floating solar power initiatives.

- The company enrolled around 1,000 dealers of Jaypee to expand Dalmia Brand cement sales in the central regions.

- The company stated that CAPEX spending during the period was approximately 2,710 crores. Pending CAPEX for organic expansion is not disclosed, but the total estimated CAPEX for FY24, including the Jaypee acquisition, is around 5,000-5,500 crores.

- The company stated operationalizing the Jaypee assets is in process, awaiting lender approval, and is expected to be completed within a couple of months.

- Raw material costs have increased partly due to high opening cost inventory and an increase in the CC ratio.

- The company stated power and fuel costs in Q4 were around $174-$175 per ton, and in Q1, it is expected to be around $165 per ton.

- The blending ratio of cement reached 84% in FY23.

- The company stated that Government departments and infrastructure projects have started accepting blended cement (PPC or PSC) in place of OPC. Builders, road contractors, and NHAI are also increasingly accepting PPC cement.

- The company aims to produce only blended cement (low-carbon cement) in the future.

- There is no specific target shared for the blending ratio in FY24-25, but the goal is to achieve 100% blended cement

- The budgeted CAPEX spend for FY24 is estimated to be in the range of 5,000 to 5,500 crores, including the payment for the acquisition of Jaypee cement assets.

- The company proposed a final dividend of Rs. 5 per share, subject to shareholder approval, in addition to the interim dividend of Rs. 4 per share.

- Dalmia is confident about completing the Jaypee acquisition in a couple of months.

- The company remains committed to its goal of reaching 75 million tons by FY27 and plans to provide a roadmap for the next phase of expansion from 56 to 75 million tons in the next quarter.

- The company aims to become a 110 and 130-million tons company by FY31.

- The company has started tolling agreements, enrolling dealers, and building the brand in preparation for the closure of the Jaypee transactions.

- The decline in power and fuel costs is expected to flow through to the EBITDA line in the first half of the year, but pricing remains uncertain and varies by region and market.

- The company stated that anomalies in the opening and closing stock impacted the power and fuel cost during Quarter 3 and Quarter 4, but it is expected to normalize going forward.

- On a year-on-year basis, the inventory impact is negligible, while on a quarterly basis, the impact of opening and closing stock affects the variable cost calculation.

- There will be an increase in blending ratios in South India, and the acceptability of blended cement has improved significantly over the past year.

- The company is confident about the growth opportunities and expansion potential of the Jaypee assets, considering the good plant and limestone reserves, as well as the increasing demand in the central and northern regions.

- Dalmia Cement’s fixed cost per ton is one of the lowest in the industry.

- No price increase was observed in April.

Analyst’s View

The company is in the business for more than 80 years now. The company had a great quarter with an increase in revenues by 15.7% YoY. The Cement business, through sustainability initiatives, has achieved the lowest carbon footprint in the cement sector globally and is amongst the most efficient cement companies in the world. Being one of the leading sugar producers in the country, the sugar business is geographically well diversified and committed to ‘Green Growth’ which empowers the group to enhance value for all its customers. It remains to be seen how the company’s near-term performance will pan out given the steady rise in inflation and the acquisition of Jaypee assets. Given the company’s strong working, Dalmia Bharat Ltd is a good Cement stock to watch out for.

Q3FY23 Updates

Financial Results & Highlights

Detailed Results:

- The company had a 23% YoY rise in revenues and a 143% YoY rise in PAT on a consolidated basis.

- Volume increased 11.5% YOY to 6.3 MnT

- EBITDA per ton stood at INR 1022.

- Net Debt/EBITDA stood at 0.39x.

- Added Renewable power capacity of 25 MW taking the total to 154MW.

- The blended cement percentage has been 83.1%

- Signed Definitive Agreement for the acquisition of the cement assets of Jaiprakash Associates Limited at an EV of INR 3,230 Cr

➢ Cement 5.2Mnt ➢ Clinker of 3.3Mnt ➢ Thermal Power 280MW (which includes 180MW in an SPV of which 57% stake is to be held by DCBL)

- Cement capacity targets are given by the management:

- Interim milestone of 49 million tons by March ’24 (excluding Jaiprakash associate’s acquired capacity)

- Interim milestone of 70-75 million tons by financial year ’27

- The long-term goal of 110-130 million tons by 2031

- Quarterly variable costs decreased by 8.3% QoQ due to the Moderation of fuel prices combined with efficiency measures.

- The cost of borrowing has increased from 5.6% to 7.5% YoY.

Investor Conference Call Highlights

- The company has been able to bring down its carbon footprint to 462 kg per ton of cement which is probably one of the lowest in the world cement sector as well which also matches the target it had given three years back.

- The acquisition is for an enterprise value of INR3,230 crores.

- The per kilocalorie for the quarter was around INR2,100 per million kilocalories.

- The management expects the profitability to improve going forward since utilisations in the month of January were around 55% and it’s improving. And prices in Western India, particularly in Maharashtra, are also stable.

- The company is focused on keeping net debt to EBITDA below 2 and ensuring that its growth is funded with a very strong and well-capitalized balance sheet.

- The power cost went down by 25% per ton due to a lower per kcal cost from 2.5 to 2.4 coupled with an increasing green power proportion which has increased to 24% from 15-17% in the previous quarter.

- The company is witnessing improvement in pricing in the Eastern market aided by higher demand in the past few months.

- The management is acknowledging the need for executive development & increased emphasis on succession planning owing to high growth targets set by the company which will need larger management bandwidth.

- The trade Share percentage for the quarter was 60%.

- The lead distance was around 310 kilometers. And on the fuel mix, it used about 70% pet coke and 16% coal.

- Capacity utilization for the quarter stood at 58% & expect the number to be around 64-66% for FY23.

- The company won’t get any tax benefit out of its Jaypee acquisition due to the slump sale.

- The freight cost increase was on account of the imposition of the busy season surcharge imposed by the Railways (which account for a 17% share of freight) from October onwards.

- The premium proportion in this quarter was 22%.

- The management states that there is no price increase in the month of January.

Analyst’s View

Dalmia Bharat is one of the leading cement makers in India. The company has had a decent quarter with a 23% YoY rise in revenues. The company has done well to maintain Debt to EBITDA. It is planning to reach 100% blended cement sales by 2025 from the current 75%. The company is aggressive at adding more and more renewable energy. It remains to be seen whether the company will be able to keep its debt low while trying to maintain its ambitious capacity growth, whether its expansion plans will bear fruit according to the management and board expectations & how will it weather the current inflationary climate. Nonetheless, given the strong brand image of the company, the efficient utilization of its plants, and the high EBITDA/ton and high carbon efficiency of its operations, Dalmia Bharat can prove to be a pivotal cement sector stock going forward.

Q2FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 121.00 | 144.00 | -15.97% | 40.00 | 202.50% | 349 | 189 | 84.66% |

| PBT | 89.00 | 9.00 | 888.89% | 82.00 | 8.54% | 195 | 34 | 473.53% |

| PAT | 85.00 | 9.00 | 844.44% | 67.00 | 26.87% | 183 | 25 | 632.00% |

| Consolidated Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 3,009.00 | 2,626.00 | 14.58% | 3,324.00 | -9.48% | 11,441 | 10,291 | 11.17% |

| PBT | 29.00 | 307.00 | -90.55% | 252.00 | -88.49% | 1,146 | 1,364 | -15.98% |

| PAT | -21.00 | 92.00 | -122.83% | 64.00 | -132.81% | 1,165 | 1,185 | -1.69% |

Detailed Results:

- The company had 15% YoY rise in revenues and a 123% YoY fall in PAT on the consolidated basis.

- Volume increased 13.2% YOY to 5.8 MnT

- EBITDA for the quarter stood at INR 379 crores, which translates to INR 656 per ton

- Added Renewable power capacity of 24 MW

- The blended cement percentage has been 82%

- Cement capacity targets given by the management:

- Interim milestone of 49 million tons by March ’24

- Interim milestone of 70-75 million tons by financial year ’27

- The long-term goal of 110-130 million tons by 2031

- Closing gross debt as on 30th of September stands at INR 3,287 crores, which is an increase of INR 147 crores during H1 this year. Net debt to EBITDA as of 30th September is 0.32 times.

- Premium segment share is 20% of trade for Q2, it was 19% in Q1.

- Lead distance is 308 kilometers.

- Trade share is 64%

- Fuel mix for Q2:

- Petcoke – 59%

- Domestic coal – 14%

- Currently, it’s about 70 days of inventory on the balance sheet

- Clinker ratio 1.71 for the company, it was 1.59 on YoY basis.

Investor Conference Call Highlights

- The margin compression is due to energy inflation, which management expects to recover with energy costs coming down in the coming quarters.

- During the quarter, the company has commercialized 4 megawatts of waste heat recovery system power (WHRS) and 20 megawatts of solar power, which takes total renewable energy capacity to 129 megawatts and which constitutes 24% of the power mix.

- Another 173 megawatts of renewable power is on track to implement by March ’23.

- beyond this 173, the company has taken the Board’s approval to further add 155 megawatts to renewable power.

- These renewable energy additions will give additional savings from FY24, which can be around INR 5-6.

- The management stated renewable as a percentage of total power mix which is 24% can go to 36% in two years.

- South India has traditionally been an OPC market, and the company has increased blending to 63% as compared to 47% in Q2 last year. According to the management, the increase in the blending ratio is sustainable, because the company’s focus on retail sales, focus on trade sales is yielding these results.

- The company has been able to bring down its carbon footprint to 467 kg per ton of cement, which, according to the management, should be one of the lowest in the world cement sector.

- The company has acquired one coal block and in times to come, that coal block will be able to give fuel security for the company’s Eastern operations. In addition to this, the company is also working in a way on ensuring limestone security for a large number of years, and in each and every plant, the company has big limestone security.

- Of the total CAPEX of INR 3,000 crores planned for FY ’23, the company has spent about INR 1,200 crores in H1 and is on track to spend the planned capex in H2.

- The management stated that they will be able to commission Bihar grinding unit by March ’24.

- During the quarter, the company received INR 84 crores as an incentive. And as of the quarter-end, INR 655 crores of incentive is receivable. 61 crores is accrued.

- the per kilo cal fuel cost in Q2 is INR 2.52, it was 2.47 in Q1 and management expect it to reduce by around 10% in coming quarters.

- Out of the total reduction in cash and cash equivalents, about INR 1,190 crores is because of the reduction in the value of the IEX share, and balance reduction is deliberately planned according to requirements.

- Prices have gone up by INR 20-25 in Kerala, INR 10-15 in Tamil Nadu, and not much in Karnataka and Maharashtra. In East markets, only INR 5 here and there. (price increase are net of discounts).

- For the CAPEX to come, the company has shared the capital allocation policy that net debt-to-EBITDA will not cross to 2:1, unless there is a strategic acquisition.

- For FY ’24 and FY ’25, CAPEX should be around INR 3,500 crores to INR 4,000 crores.

- In terms of the Murli, utilization would be between 55% to 60% for the whole year, the management stated.

- The management stated for LC3 to become popular, it will take four years to five years; the company has been able to identify mines of clay; it is not currently in pipeline due to higher energy needs.

- The management is expecting 14%, or 15% growth in the Northeast in the next three years.

- Current utilization in the Northeast is 70%.

- For the Bihar greenfield CAPEX, the company is almost close to the completion of the land acquisition, and the work should start.

- The increase in raw material cost is due to the fly-ash price increase and also due to the higher use of fly-ash given a higher blending ratio.

- The management stated they are expecting volume growth 1.5 times of the industry growth.

- The company has a limestone mine in Madhya Pradesh. So that project is already started to develop. The company is also looking at buying some land in Uttar Pradesh. So the long-term vision is pan-India, the company is looking at organic and inorganic opportunities all across the country.

Analyst’s View

Dalmia Bharat is one of the leading cement makers in India. The company has had a decent quarter with a 15% YoY rise in revenues. The company has done well to maintain Debt to EBITDA. But the company has not been able to grow in terms of utilization level which has remained at 60% since 2019. It is planning to reach 100% blended cement sales by 2025 from the current 75%. The company is aggressive at adding more and more renewable energy. It remains to be seen whether the company will be able to keep its debt low while trying to maintain its ambitious capacity growth, whether its expansion plans will bear fruit according to the management and board expectations & how will it weather the current inflationary climate. Nonetheless, given the strong brand image of the company, the efficient utilization of its plants, and the high EBITDA/ton and high carbon efficiency of its operations, Dalmia Bharat can prove to be a pivotal cement sector stock going forward.

Q4FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 127 | 55 | 130.9% | 36 | 252.8% | 349 | 189 | 84.7% |

| PBT | 96 | 5 | 1820.0% | 7 | 1270.4% | 195 | 34 | 473.5% |

| PAT | 96 | 5 | 1820.0% | 37 | 159.5% | 183 | 25 | 632.0% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 3433 | 3190 | 7.6% | 2764 | 24.2% | 11441 | 10291 | 11.2% |

| PBT | 360 | 420 | -14.3% | 93 | 287.1% | 1146 | 1364 | -16.0% |

| PAT | 599 | 641 | -6.6% | 61 | 882.0% | 1165 | 1185 | -1.7% |

Detailed Results:

- The company had 7% YoY rise in revenues and a 6% YoY fall in PAT.

- Dalmia Bharat saw quarterly volume growth of 2.3% YoY while EBITDA stood at Rs 683 Cr.

- The company commenced commercial production of 2.9 MnT Murli Cement plant in Maharashtra on 15th January 2022.

- Total Cement Capacity increased to 35.9 MnT while Total Clinker Capacity stood at 18.9 MnT.

- Annual volumes grew by 7.3% YoY.

- WHRS & Solar capacity for FY22 stood at 32 & 31 MW each.

- EBIDTA margins stood at 20.1%.

- Quarterly variable costs increased by 20.9% YoY while logistics costs increased by 8.2%.

- EBITDA/Ton was at Rs 1036.

- Net debt to EBITDA stands at -0.59X.

- The Board has proposed a final dividend of Rs. 5 per share.

Investor Conference Call Highlights:

- The company has identified 3 strategic long-term targets which are

- to be a pan-India pure-play cement company

- to maintain a significant presence in every market it serves

- to grow its capacity to between 110-130 MTPA by 2031

- Rising input costs impacted the cash flows and EBITDA for Dalmia due to the lag in passing on the cost increases.

- The cement industry demand outlook is expected to grow at a CAGR of 8-9% in the coming future.

- Petcoke prices have doubled YoY in FY22 to $246.

- The green fuel% stood at 16.4% in Q4.

- The company has won the Brinda-Sisai Coal Block in Eastern India recently.

- Overall fuel consumption has almost doubled from $78 in FY21 to $141 in FY22.

- Dalmia has also managed to double its renewable capacity from 31 MW to 62 MW in FY22.

- The management states that restricting the product mix and improvement in operating KPIs have helped in cost savings of Rs.64 per tonne.

- The company has seen cement price increase from Rs 30-50 per bag in Q4 vs Q3 and this trend is expected to continue.

- The company outperformed the industry in North & south region where it saw double digit volume growth whereas it lost some market share in Eastern market.

- The company remains on track to achieve its medium-term goal of reaching 48.5 million tonnes capacity by March ‘24.

- The company’s brand – “DSP” as a % of trade sales stood at 20% Vs 18% YoY.

- The company’s CO2 emissions per tonne of cement has reduced to 489 kg while its water positivity rate of 12.5x.

- The company’s incentive collection for FY22 was Rs.237 Cr.

- The freight costs increased by Rs.80 per tonne due to movement of higher quantities from railways along with lead distance increasing by 20 Km.

- Capex for FY22 was at Rs 1900 Cr and the projected capex for FY23 is at Rs 3000-3500 Cr.

- The management states that the delta from CPP or grid, and the WHRS and solar would be ranging between Rs.6 to Rs.7.

- The company will add capacity of 41MW in WHRS & 66Mw in solar plant & expects saving of close to Rs.150 Cr in FY23 & Rs.240 Cr in FY24.

- The company expects to clock capacity utilisation rate of 60-70% in its Murli plant in FY22.

- The management has reassured that although it is committed to maintain d a net debt EBITDA of less than 2 times, it will not be forgoing any acquisition opportunities to maintain this ratio.

- The management expects to see good demand from the rural side as tractor sales for M7M have risen 50% YoY in April which is a good sign for overall rural demand recovery.

- The upcoming H1 is expected to be tough according to the management due to supply side inflation concerns from the ongoing war and the interest rate hike cycle.

- The company’s trade mix for the quarter stood at 65%, and the lead distance for the quarter was 318 km.

- The company’s CO2 emissions reduction was relatively lower due to usage of old plants of its Murli & Kalyanpur facility.

- The company’s blending % in cement stood at 78%.

- The contribution of pet coke towards total power mix stood at 64%.

Analyst’s View:

Dalmia Bharat is one of the leading cement makers in India. The company has had a decent quarter with an 7% YoY rise in revenues. The company has done well to maintain Debt to EBITDA at negative levels and has seen commercialization of a 2.9 MT capacity in Murli plant in Maharashtra in Q4. But the company has not been able to grow in terms of utilization level which has remained at 60% since 2019. It is planning to reach 100% blended cement sales by 2025 from the current 75%. It remains to be seen whether the company will be able to keep its debt low while trying to maintain its ambitious capacity growth, whether its expansion plans will bear fruit according to the management and board expectations & how will it weather the current inflationary climate. Nonetheless, given the strong brand image of the company, the efficient utilization of its plants, and the high EBITDA/ton and high carbon efficiency of its operations, Dalmia Bharat can prove to be a pivotal cement sector stock going forward.

Q3FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 36 | 47 | -23.4% | 144 | -75.0% | 222 | 134 | 65.7% |

| PBT | 7 | 13 | -46.2% | 82 | -91.5% | 99 | 29 | 241.4% |

| PAT | 10 | 9 | 11.1% | 67 | -85.1% | 87 | 20 | 335.0% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 2761 | 2783 | -0.8% | 2622 | 5.3% | 7996 | 7092 | 12.7% |

| PBT | 93 | 311 | -70.1% | 307 | -69.7% | 786 | 977 | -19.5% |

| PAT | 73 | 179 | -59.2% | 214 | -65.9% | 575 | 601 | -4.3% |

Detailed Results:

- The company had flat revenues and a 59% YoY fall in PAT.

- Dalmia Bharat saw volume growth of 2.5% YoY while EBITDA stood at Rs 409 Cr vs Rs 681 Cr last year.

- EBIDTA margins stood at 14.97%.

- EBITDA/Ton was at Rs 718.

- Net debt to EBITDA stands at -0.64X.

- The company completed the Commercialization of Cement capacity of 2.9 MnT of Murli cement plant at Maharashtra.

- Total capacity is now at 35.9 MnT.

- The company completed slump sale of Hippo Stores (retail business) for Rs 155 Cr.

Investor Conference Call Highlights:

- Q3 was tough for both Dalmia and the cement industry with rising input costs and weak demand.

- Petcoke price increased to $164/ton in Q3.

- The company received Rs 35 Cr upfront from the slump sale of Hippo.

- Capacity utilization in Q3 was at 69% but it rose to 83% in Dec.

- The management expects to see good performance in Q4.

- The trade % was at 59% in Q3.

- The share of DSP in trade sales was at 21%.

- Lead distance rose to 298 km in Q3 from 285 km in Q2.

- The company did capex of Rs 1350 in 9M and expects to do a further Rs 800 Cr capex in Q4.

- The company has won a limestone block auction in Jhunjhunu district of Rajasthan.

- CO2 emissions were at 488 kgs per ton in Q3.

- Packing costs have also risen 40% YoY to Rs 124 per kg.

- The closing debt as of 31st Dec 2021 was at Rs 3647 Cr.

- Cement clinker ratio in 9M was at 1.62.

- Currently cement prices in the east are lower than the south and west zones but the management is confident that it will rise soon.

Analyst’s View:

Dalmia Bharat is one of the leading cement makers in India. The company has had a decent quarter with an 11% YoY rise in revenues despite a seasonal drop in industry sales due to monsoons. The company has done well to maintain Debt to EBITDA at negative levels and has seen commercialization of a 2.25 MT capacity in Odisha in Q2. But the company has not been able to grow in terms of utilization level which has remained at 60% since 2019. It is planning to reach 100% blended cement sales by 2025 from the current 75%. It remains to be seen whether the company will be able to keep its debt low while trying to maintain its ambitious capacity growth and whether its expansion plans will bear fruit according to the management and board expectations. Nonetheless, given the strong brand image of the company, the efficient utilization of its plants, and the high EBITDA/ton and high carbon efficiency of its operations, Dalmia Bharat can prove to be a pivotal cement sector stock going forward.

Q2FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 144 | 42 | 242.86% | 42 | 242.86% | 186 | 87 | 113.79% |

| PBT | 82 | 7 | 1071% | 10 | 720.00% | 92 | 16 | 475% |

| PAT | 67 | 5 | 1240% | 10 | 570.00% | 77 | 11 | 600.00% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 2622 | 2353 | 11.43% | 2613 | 0.34% | 5235 | 4309 | 21.49% |

| PBT | 307 | 367 | -16.35% | 386 | -20.47% | 693 | 666 | 4.1% |

| PAT | 209 | 232 | -9.91% | 238 | -12.18% | 447 | 420 | 6.43% |

Detailed Results:

- The company had 11% YoY rise in revenues and a 10% YoY fall in PAT.

- Dalmia Bharat saw volume growth of 6% YoY while EBITDA stood at Rs 620 Cr.

- Volume grew 6.2% YoY.

- EBIDTA margins stood at 24.1%.

- EBITDA/Ton was at Rs 1217.

- Net debt to EBITDA stands at -0.48X.

- The company completed the Commercialization of Cement capacity (Line 2) of 2.25 MnT near Cuttack, Odisha.

- Dalmia also commenced trial production at the 3MT plant at Maharashtra.

- The company declared a dividend of Rs 4 per share in Q2.

Investor Conference Call Highlights:

- The company has identified 3 strategic long-term targets which are

- to be a pan-India pure-play cement company

- to maintain a significant presence in every market it serves

- to grow its capacity to between 110-130 MTPA by 2031

- To mitigate the impact of higher fuel prices, the company shifted its product mix from PSC to PCC which has less fuel usage and is of similar quality.

- PSE products declined from 27% in Q1 to 14% in Q2.

- The company reduced its pet coke usage from 47% to 33% in the current quarter.

- Green fuel usage increased from 9% to 12% QoQ.

- The management is expecting to add 9 megawatts of WHRS power and 70-plus megawatt of solar power in the latter half of this year.

- The current capacity stands at 33MTPA with successful commercialization of KCW and Odisha plants that have capacity of 2.25MTPA.

- The management is on track to increase cement capacity to 36 million tonnes by March ’22.

- The company has sold 21.4 lacs shares in IEX, and its stake in IEX now stands at 14.8%.

- The board has approved the slump sale of Hippostores Technology Private Limited for Rs 115 Cr. The sale should be concluded by 31st Dec 2021.

- The management saw prices in the East zone stay weak in the current quarter due to low demand and Q2 being a weak quarter in general in the East. However, it is seeing prices improve in the East and expects the rise to continue in the future.

- The management expects to spend around Rs 3000 Cr in capex in FY22 and reach 48.5 MT capacity in the next 12 months.

- The company has been able to make fuel cost savings to the tune of Rs 80-100 per ton due to use of green fuels.

- The company’s consumption rate of its input cost on power and fuel has ranged at around $120 to $130 per tonne.

- The company was able to contain its freight costs which grew by 1% (including railways incentive of Rs.16 Cr) due to reduction in lead distance by 12-14Km & careful tracking of truck movement.

- The company’s per tonne procurement cost of slag in Q2 stood at Rs.1100 – 1300.

- The management is taking steps to increase the concentration of composite cement in the product mix as it believes it is “the cement of the future”.

- The company had a blended cement mix of 75% in this quarter, however it is aiming blended mix of 100% by 2025.

- The company did a write-off of Rs.30 Cr for a corporate loan given in 2010.

- The company’s power consumption to cement is now 62 kWh per tonne of cement which is one of the lowest power consumptions per tonne of cement & this helped to contain the power cost.

- The management expects to receive annual incentives of Rs.200 Cr per year till FY24.

- The realizations in the current quarter have dropped to due to low selling prices across the country.

Analyst’s View:

Dalmia Bharat is one of the leading cement makers in India. The company has had a decent quarter with an 11% YoY rise in revenues despite a seasonal drop in industry sales due to monsoons. The company has done well to maintain Debt to EBITDA at negative levels and has seen commercialization of a 2.25 MT capacity in Odisha in Q2. But the company has not been able to grow in terms of utilization level which has remained at 60% since 2019. It is planning to reach 100% blended cement sales by 2025 from the current 75%. It remains to be seen whether the company will be able to keep its debt low while trying to maintain its ambitious capacity growth and whether its expansion plans will bear fruit according to the management and board expectations. Nonetheless, given the strong brand image of the company, the efficient utilization of its plants, and the high EBITDA/ton and high carbon efficiency of its operations, Dalmia Bharat can prove to be a pivotal cement sector stock going forward.

Q1FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 42 | 45 | -6.67% | 55 | -23.64% |

| PBT | 10 | 9 | 11.11% | 5 | 100.00% |

| PAT | 10 | 6 | 66.67% | 5 | 100.00% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 2615 | 1956 | 33.69% | 3186 | -17.92% |

| PBT | 372 | 299 | 24% | 417 | -10.79% |

| PAT | 277 | 191 | 45% | 630* | -56.03% |

*Contains negative tax charge of Rs 213 Cr

Detailed Results:

- The company had 34% YoY rise in revenues and a 45% YoY rise in profits due to the low base in Q1FY21.

- Dalmia Bharat saw volume growth of 33% YoY while EBITDA grew 14% YoY.

- EBITDA/Ton was at Rs 1432.

- The company reduced its gross debt by Rs 476 Cr.

- Net debt to EBITDA stands at 0.08 vs 1.02 a year ago.

- EPS grew 40% YoY to Rs 14.23.

- The company unveiled its long term a goal of reaching 110-130 MTPA capacity by 2031.

- Its current capex plan is to expand capacity from the current 30.8 MTPA to 48.5 MTPA.

- The clinker capacity is also to be expanded to 23.4 MTPA from the current 18.68 MTPA by FY24.

- The company expects the current capex plan to include:

- Rs 1950-2000 Cr for ongoing capacity expansion of 7.75 MTPA

- Rs 4700-5000 Cr for new capacity building including 10 MTPA from clinker bottlenecking

- Rs 1000-2000 Cr for green initiatives

- Rs 900-1000 Cr for maintenance capex

Investor Conference Call Highlights:

- The company has identified 3 strategic long-term targets which are

- to be a pan-India pure-play cement company

- to maintain a significant presence in every market it serves

- to grow its capacity to between 110-130 MTPA by 2031

- Capacity expansion in the last 10 years was uneven with 1st 5 years having a CAGR of 25% while the last 5 years had a CAGR of only 4%. The company is now aiming to expand more stably and predictably and maintain a CAGR of 15% capacity expansion in the next 10 years.

- The management announced that the company is aiming to become a 100% blended cement company in the next 5 years.

- Its carbon footprint is below 500 kgs of carbon dioxide per ton of cement and it is aiming to reach 400 kgs by 2040.

- As part of the announced capital allocation policy, the company is looking to use 10% of its operating cash flows to develop and adopt innovative technologies to combat climate change.

- It is looking to allocate Rs 1000-1200 Cr in the next 2-3 years for waste heat recovery systems, solar power and equipment, and IT to substitute fossil fuels and clinker. By March 2023, the solar capacity is expected to be at 87 MW and the WHRS is expected to be at 62 MW.

- The company is targeting a ROCE of 14-15% in the next few years.

- The management has stated that although the current debt to EBITDA is very low, it can expand due to the company’s expansion initiatives. The company will be looking to maintain this figure below 2 times Debt to EBITDA.

- The company has decided to divest the retail business from DCBL and become a pure-play cement business. It will be looking to complete this in the next 3-4 months and has made an allocation of Rs 40 Cr for expenses till the divestment is completed.

- The company will be maintaining most of its treasury in AAA or AA+ rated debt instruments only.

- The company expects the commercial production of Murli Cement from the Odisha grinding unit to start by December 2021. This will expand the total capacity to 36 MTPA.

- The Bihar grinding unit is expected to start production by March 2024. The remaining capex for this unit is around Rs 2000 Cr.

- The Bokaro plant will see a brownfield expansion of 1.7 MTPA.

- DBCL also sees that a capacity of 5.3 MTPA can be added through debottlenecking across all plants.

- The company is also aiming to reach 100% renewable energy by 2030 and 100% energy productivity by 2030.

- The company has kept RM costs at Rs 855 per ton while fuel & energy costs have risen to Rs 1054 per ton due to a rise in petcoke and coat costs.

- Green fuel now accounts for 9.1% of its fuel mix and DCBL is looking to increase it to 20% by the end of FY22.

- The logistics costs have also risen marginally to Rs 1057 per ton.

- The management states that the company lost market share in the East zone in Q1 due to the stoppage of the Cuttack grinding unit for few days on account of COVID and changes in its marketing plan.

- The management has stated that the company will be slowly moving away from PPC, and it will be focusing on Portland Composite Cement and Portland Slag Cement.

- The company has done Rs 300 of capex in Q1 and it expects to do a further Rs 3700 Cr in the rest of FY22.

- The company will be mainly making PPC for its business in the South zone.

- The management remains confident that DCBL will be able to ramp up its limestone reserves in its key sites and get new blocks in new areas.

- The management expects further consolidation to take place in the cement industry with the top 4-5 players growing at a CAGR of 14-15% in the next decade.

- In the South zone, DCBL is adding to capacity in TN and Kerala as the management feels that DCBL will be getting a better cost advantage in these states than other cement players from Andhra Pradesh. Most of the capacity will also be used to service TN and Kerala markets.

- The company also has plans to expand in the North and Central zones and it will reveal them in time.

- The greenfield grinding units in TN and Kerala should be completed by March 2023 according to the management.

- The company will be ready to divest the rest of its stake in IEX as and when it requires funds for its proposed capital allocation.

- Despite having capacity utilization at near 60%, the management wants to go for further capacity utilization as it doesn’t believe that capacity expansion should be taken only when utilization hits 80% and that the company should be looking to expand capacity according to its vision of the future.

- The management has stated that it will also be on the lookout for possible inorganic opportunities for expansion but it will be dependent on it for reaching the long-term expansion goals.

- The company projections state that it will not need any extra debt to be able to sustain a growth rate of 10% CAGR for the next 10 years.

- The consolidation cycle in the cement industry is expected to mainly be driven by the decline of smaller players and the increasing debt burden of them while making expansions.

- The WHRS will be commissioned by June-July 2022.

- The company maintained a cement to clinker ratio of 1.65 in FY21.

- The management does not expect much price pressure going forward.

Analyst’s View:

Dalmia Bharat is one of the leading cement makers in India. The company has had a decent quarter and it has unveiled an ambitious capital allocation plan for the next decade which targets reaching a capacity of 110-130 MTPA by 2031 and 48.5 MTPA by 2024. The company has done well to maintain EBITDA/ton above Rs 1400 despite rising fuel and petcoke prices YoY. It is looking to make a total capex of Rs 4000 Cr in FY22 which is including setting a new solar facility, capacity expansion, and debottlenecking in current plants. But the company has not been able to grow in terms of utilization level which has remained at 60% since 2019. It remains to be seen whether the company will be able to keep its debt low while trying to maintain its ambitious capacity growth and whether its expansion plans will bear fruit according to the management and board expectations. Nonetheless, given the strong brand image of the company, the efficient utilization of its plants, and the high EBITDA/ton and high carbon efficiency of its operations, Dalmia Bharat can prove to be a pivotal cement sector stock going forward.

Disclaimer

This is not investment advice. Please read our terms and conditions.