About the Company

Balkrishna Industries Limited (BKT) is a tire manufacturing company based in Mumbai, India. Balkrishna Industries manufactures off-highway tires used in specialist segments like mining, earthmoving, agriculture and gardening in five factories located in Aurangabad, Bhiwadi, Chopanki, Dombivali, and Bhuj. In 2013, it was ranked 41st among the world’s tire makers.

Balkrishna Industries is currently an OEM vendor for heavy equipment manufacturers like JCB, John Deere, and CNH Industrial. The company currently enjoys a 6% market share of the global off-the-road tire segment.

If you are interested to know about the business of BKT in detail, watch this video .

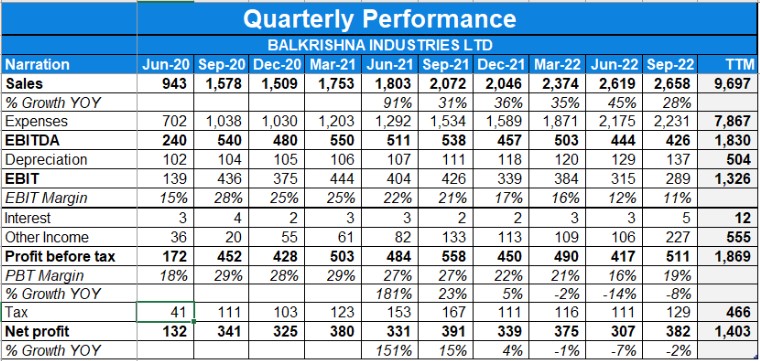

Q4FY23 Updates

Financial Results & Highlights

Detailed Results:

- The company had a poor quarter with sales growth of negative 2% while profit degrowth of 31%.

- Sales volume stood at 72,676 MT, a growth of 9% QoQ.

- Gross Cash and Cash equivalents of Rs. 2,075 Cr as on 31st March 2023.

- EBIDTA margins stood at 21.3% Vs 23.7% YoY while PAT margins stood at 11% Vs 15.4%.

- For the quarter, the company had a net forex gain of INR 26 crore. This includes a realized gain of INR 23crore and an unrealized gain of INR 3 crore.

- Gross debt stood at INR 3,254 crores at the end of 31st March ’23, of which about 75% is related to the working capital debt.

- The Board of Directors has declared a Final dividend of INR 4 per share.

- The Volume Profile for the company for FY23 were as follows :-

Investor Conference Call Highlights

- The management states that Q4FY23 has been a better quarter from a sequential point of view with an uptick in volumes, better demand from end markets, and partial clearing of high-priced raw materials. However, end markets, especially channel inventory situation, is not completely out of the woods.

- The management states that it expects the channel led inventory issues to be resolved by June or July.

- In Q4, the EBITDA margin is at 21.3%, which has improved sequentially. This has been due to better absorption of high-cost raw material inventory that they were carrying in the system and lower freight costs.

- The management states that it has continued to make higher spending in brand building and marketing initiatives, which slightly impacted margins. Excluding these investments, margins would have been slightly higher in Q4.

- In view of the long-term strategy of increasing market share, the investments are required to achieve the aspiration of 10% market share over the next few years. As sales volume increases, these spends, as a percentage of sales, will come down.

- For FY24, the management remains positive. They states that they would be in a better position to discuss volume guidance in the next few months. On the margin front, multiple levers such as favourable raw material costs, better hedge rates, and complete normalization of logistic costs, will aid the improvement in margin profile.

- In terms of end markets, the management expects Europe to normalize later during the year, while America and India will continue its FY ’23 performance trajectory.

- The advanced Carbon Black project of 30,000 metric tons per annum is running delayed, and is expected the same to be completed in H2.

- The capex for the brownfield capacity addition of 25,000 metric tons per annum at Waluj has been completed. Full ramp up of production will reach over a period of 6 months. Now the Waluj location has a total capacity of 55,000 metric tons per annum.

- The management states that at the company level, the achievable capacity stands back at the original 360,000 metric tons per annum.

- For FY24, the estimated capex spend will be of INR550 crores to INR600 crores. Of this, routine maintenance capex will be INR250 crores to INR300 crores. The balance will be spent towards new product development like rubber tracks and giant solid tyres.

- The capex will help to widen the product basket in the end market along with higher investments in brand building and marketing efforts, which are required to reach the market share goal of 10%.

- The company crossed the historical mark of INR10,000 crores sales annually for the first time in history.

- For Q4 financial year ’23, the euro hedge rate was 86.50, while for financial year it was 85.30. Forward hedge rates for financial year ’24 currently stand at around 88 to 89 levels.

- The management states that the H2 volumes for USA going down sharply is a seasonal thing. It is confident of America continuing on its growth trajectory.

- ASPs have come down 4% in the quarter, due to a combination of product mix and lower freight costs being passed through. Minor correction is expected more in the coming quarters.

- The management expects RM costs to reduce by 1%-2% by the next quarter.

- Indian market has grown 28% this year, with growth in both Agri and OTR tyres.

- The interest costs has gone up from INR15 crores in Q2 to INR25 crores in Q4 due to the EURIBOR rate going up. It is now expected to stay in the same range. The current rate is around 4% approximately.

- The management states that gross debt levels are planned to come down this FY.

- The company capitalizes a very small part of the capex-related interest costs while most of it goes to the PnL.

- The management does not plan to set up any plant outside India currently.

- The company has got a good response for the ultra large tyres on mining side, and has a capacity of 5000 tons per year.

- The Carbon Black sales to third party was 6% for FY23 with 85% to 90% capacity utilization.

- The management gives a guidance of becoming a net-debt free company in the next 15-18 months. No new major capex expansion will be announced before that.

Analyst’s View:

BKT is India’s Leading player in the Global ‘Off-Highway Tire (OHT)’ Market. The company had a poor quarter on a YoY basis due to poor demand from the end users coupled with higher raw material, interest costs as well as forex losses. The company has a wide and comprehensive product portfolio and a deep understanding of the OHT market has led to capabilities to manufacture over 3,200 SKUs. BKT has built a resilient business model and is confident to withstand the near-term challenges to emerge stronger with a higher global market share. The company has a global reach as it does sales to over 160 countries through Distribution networks in the Americas, Europe, India, and the Rest of the World. It is India’s Largest Off-Highway Tire Manufacturer. The company’s brand recognition has grown and brand acceptability has grown. BKT is working on increasing its brand recognition and therefore aggressively looking for options available. Not only does the company want to be a low-cost operator but also a branded player as well. With capex to control raw material cost and debottlenecking in place, it would be recommended to keep a watch on the updates.

Q3FY23 Updates

Financial Results & Highlights

Detailed Results:

- The company had a poor quarter with sales growth of only 6% while profit degrowth of 68%.

- Sales volume stood at 66,840 MT, a de-growth of 5%.

- Gross Cash and Cash equivalents of Rs. 2,082 Cr as on 31st December 2022.

- EBIDTA margins stood at 19.1% Vs 24.4% YoY while PAT margins stood at 4.5% Vs 15.8%.

- For the quarter, the company had a net forex gain of INR 168 crore. This includes a realized gain of INR 120 crore and an unrealized gain of INR 48 crore.

- For the quarter ended Q3FY23, it had a net forex loss of INR 88 crores, which includes realized gain of INR 78 crores and an unrealized loss of INR 166 crores.

- Gross debt stood at INR 3,464 crores at the end of 31st December ’22, of which about 75% is related to the working capital debt.

- The Board of Directors has declared a third interim dividend of INR 4 per share.

Investor Conference Call Highlights

- The management explains that since The distribution channel is across the global market and has excess inventory, So with the slow lowering of raw material prices and improvement in delivery timelines owing to better availability of containers, led to a lower reordering cycle via this channel.

- The management states that continues to face the challenges of destocking in Q4. However, the intensity of the situation is receding on a month-to-month basis.

- Freight costs have decreased significantly which has been partially passed on to customers, however, the benefits were set off by higher costs of raw materials & lower volumes leading to negative effects of operating leverage.

- On the carbon black front, The capex of the Carbon Black project along with the Power Plant has been completed & With the commissioning of 55,000 metric tons per annum, and power achievable capacity stands at 170,000 metric tons per annum. The advanced Carbon Black project of 30,000 metric tons per annum is on track and expected to commission the same by the end of the current quarter or the early part of next quarter.

- On the capacity front, The capex for Brownfield capacity, for the addition of 25,000 MTPA at Waluj has commenced & is expected to be completed in the first half of the next financial year. Post completion of this Brownfield project, Waluj will have a total capacity of 55,000 metric tons at a single location. At a company level, the achievable capacity will increase back to 360,000 metric tons per annum by end of the first half of financial year ’24.

- For the 9 months of the financial year ’23, 49% of the sales came from Europe, 21% from India, 19% from America, and the balance from the rest of the world.

- In terms of channel contribution, 70% was contributed from the replacement segment while OEM contributed 28% with the balance coming from offtake.

- In terms of category, the agricultural segment contributed 63%, while OTR, industrial, and construction contributed 34% and the balance came from other segments.

- The company’s inventory days stand at 60-65 days while it strives for 45 days.

- Interest in working capital stood at 3.5-4%.

- The realization was reduced owing to a lower surcharge.

- The company is unable to completely pass on the price increase.

- The pricing difference between its competitors in the west of 10-15% remains.

- The capex for 9M stood at 1300 Crs.

- Low single-digit growth is expected in the off-highway tire segment.

- The management expects at least 300 Bps EBITDA margins improvement in FY24 owing to lower RM costs & freight.

- The lower Volumes in the US are primarily due to inventory correction.

- The company hasn’t lost any market share & expects higher benefits of operating leverage due to higher volumes coupled with interest & depreciation costs going down.

- Carbon black contributed 5% of the total topline.

- The tenure for long-term & short-term borrowings is 3 years & 6 months respectively.

- The company’s current market share stands at 5-6% & it targets 10%.

- The overstocking at the current period stands at 5-10% of the volumes ordered by the distributors.

Analyst’s View:

BKT is India’s Leading player in the Global ‘Off-Highway Tire (OHT)’ Market.The company had a poor quarter on a YoY basis due to poor demand from the end users coupled with higher raw material, interest costs as well as forex losses. The company has a wide and comprehensive product portfolio and a deep understanding of the OHT market has led to capabilities to manufacture over 3,200 SKUs. BKT has built a resilient business model and is confident to withstand the near-term challenges to emerge stronger with a higher global market share. The company has a global reach as it does sales to over 160 countries through Distribution networks in the Americas, Europe, India, and the Rest of the World. It is India’s Largest Off-Highway Tire Manufacturer. The company’s brand recognition has grown and brand acceptability has grown. BKT is working on increasing its brand recognition and therefore aggressively looking for options available. Not only does the company want to be a low-cost operator but also a branded player as well. With capex to control raw material cost and debottlenecking in place, it would be recommended to keep a watch on the updates.

Q2FY23 Updates

Financial Results & Highlights

Detailed Results:

- Gross Cash and Cash equivalents of Rs. 2,078 Cr as on 30th September 2022.

- EBIDTA margins stood at 20.1% while PAT margins stood at 14.4%.

- Revenue from operations increased by 35% while EBIDTA remained flat.

- For the quarter, the company had a net forex gain of INR 168 crore. This includes a realized gain of INR 120 crore and an unrealized gain of INR 48 crore.

Investor Conference Call Highlights

- BKT registered a sales volume of 78,872 metric tons.

- India continues to be stable supported by a better economic environment backed by good monsoons. However, the global economic weakening coupled with a sharp uptick in interest rates has also reduced order placements by dealers and distributors.

- The demand pattern in Northern America is better than in Europe although growth fears remain.

- Due to the challenging macro environment, the company won’t guide annual sales volume for this financial year.

- The recent price correction in raw materials and logistic costs bode well for the company’s profit margin, however, the benefits will kick in from early Q4.

- With respect to the Waluj plant Capex, the management decided to continue operations at both plants along with the modernization of the old plant.

- The earlier approved CAPEX of Rs. 350 crores for the modernization of the old plant will now be utilized at the new plant site to bring in economies of scale. This will be a brownfield capex expected to get completed by H1FY24.

- The Waluj location will have an overall capacity of 55,000 tons per annum at a single site.

- Accordingly, the current achievable capacity will stand reduced to 335,000 metric tons per annum and will increase back to the original number of 360,000 metric tons by the end of the first half of the next financial year post-commissioning of the Waluj Brownfield project.

- The company completed the modernization, automation and technology upgradation CAPEX at its Rajasthan and Bhuj plants.

- The CAPEX for Carbon Black continues to be on track & the commissioning of the 55,000 metric ton per annum Carbon Black project along with the power plant is expected during December. In addition, the advanced Carbon Black project of 30,000 metric tons will be commissioned during the Q4 of this financial year.

- The company is not giving guidance for Europe due to uncertainty surrounding the Geopolitical scenario & severe winter.

- ASP improved due to dollar movement, North American contributing increasing & favorable product mix.

- The current inventory levels of the dealer stand at 3 months & the company expects them to de-stock to a level of 2 months.

- The company incurred Rs.900 Crs Capex in H1 & expects to incur another Rs.300 Crs in H2.

- The current inventory levels of dealers are higher due to demand tapering off because of geopolitical scenario coupled with lower shipping time.

- The company doesn’t hedge US dollars because it has a natural hedge because fo raw material & machinery purchases. It only hedges Euro.

- The company’s Carbon Black sales are approximately 5% of its turnover for the last quarter, which used to be about 3%.

- The management expects the working capital cycle to decrease post-reduction in the freight period.

- The company is strongly positioned to take advantage of a potential increase in demand in the replacement market in Europe as 70% of the company’s channel is the replacement segment.

- Logistic costs are down for the current quarter & management is hopeful of a further 25-30% drop in the costs.

Analyst’s View:

BKT is India’s Leading player in the Global ‘Off Highway Tire (OHT)’ Market. Company has a wide and comprehensive product portfolio and deep understanding of the OHT market has led to capabilities to manufacture over 3,200 SKUs. BKT has built a resilient business model and is confident to withstand the near-term challenges to emerge stronger with a higher global market share. Company has global reach as it does sales to over 160 countries through Distribution networks in Americas, Europe, India and Rest of the World. It is India’s Largest Off-Highway Tire Manufacturer. Company’s brand recognition has grown and brand acceptability has grown. BKT is working on increasing its brand recognition and therefore aggressively looking for options available. Not only does the company want to be a low cost operator but also a branded player as well. With capex to control raw material cost and debottlenecking in place, it would be recommended to keep a watch on the updates.

Q4FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 2481 | 1804 | 37.5% | 2141 | 15.9% | 8697 | 5919 | 46.9% |

| PBT | 488 | 494 | -1.2% | 439 | 11.2% | 1954 | 1531 | 27.6% |

| PAT | 374 | 372 | 0.5% | 328 | 14.0% | 1410 | 1155 | 22.1% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 2483 | 1815 | 36.8% | 2159 | 15.0% | 8733 | 5955 | 46.6% |

| PBT | 490 | 503 | -2.6% | 450 | 8.9% | 1982 | 1555 | 27.5% |

| PAT | 375 | 380 | -1.3% | 339 | 10.6% | 1435 | 1177 | 21.9% |

Detailed Results:

- The revenue for the quarter grew 36% YoY & 15% QoQ in consolidated terms.

- PBT was down by 1% YoY & 2% YoY in standalone and consolidated terms in Q4.

- Consolidated PAT was down 1% YoY in the quarter while EBIDTA was up by 3%.

- Sales volumes for the quarter came in at 77,119 metric tons which were up 13% YoY.

- The EBITDA margin fell 820 bps YoY to 23.7% in Q4.

- Sales breakup in FY22 for the company is:

- Agri-65.5%, OTR-31.1%, Others-3.3%.

- Replacement-69.1%, OEM-27.7%, Others-3.3%

- EU-53.9%, Americas-17.3%, India-17.6%, RoW-11.2%

- The company saw a forex gain of Rs 58 Cr in Q4.

- The company remains debt-free with current cash holding at Rs 1932 Cr as of 31st March 2022.

- The company is aiming to reach achievable capacity of 3.6 Lac tons per year by the end of FY23.

- The Sales Volume guidance for FY23 stands at 320,000 – 330,000 MT.

- The company declared final divided of Rs.4 per equity share.

- The Board of Directors have decided keep the Capex investment of Rs.350 Cr announced at Old Waluj Plant in November 2021, on hold.

Investor Conference Call Highlights

- The Waluj plant Capex has been put on hold due to higher demand scenario leading to company deciding to utilise the existing plant.

- The company plans to incur capex of Rs.900 Cr in FY23 & 24.

- The management expects the current elevated freight costs to stay for the next few quarters.

- The company’s working capital costs have gone up due to higher shipping periods, higher costs of raw material & higher turnover achieved by the company.

- The company took price increase of 2-3% in February & is planning to take another hike of 3-4% in June.

- The cost of key raw materials stood as follows – Natural rubber around Rs.150 per kg, carbon around Rs.98 to Rs.100 per kg, and fabric approximately Rs.375 per kg.

- 100% of carbon black consumption is from the captive usage.

- The management states that its Bhuj power plant will be operational within 2-3 months which will help to reduce the power costs & ensure uninterrupted supply.

- The gap between company & its competitor’s price from Tier 1 is 12-15%.

-

- The company wants to maintain an EBIDTA margin of 28-30% on a sustainable basis.

- The management expects to get 8-10% of cost savings due to captive power plant in Bhuj.

- The company’s market share In India stands at 4-5%.

- The employee costs have reduced from Rs.97 Cr to Rs.90 Cr QoQ due to lapse of additional incentives given during the Covid period.

- The company will incur maintenance Capex of Rs.200 Cr in FY23.

- The company’s total carbon black capacity is 140000 metric ton out of which 115000 is currently achievable.

Analyst’s View:

BKT has been a rising player in the off-road tires business for years now. The company witnessed strong inflationary pressures with PAT remaining flat despite revenues increasing by 36%. It is looking to maintain a steady EBITDA margin of 28-30% and has done a price increase of 2-3% in February to preserve margins despite rising RM & logistics costs. The management maintains that the end industries are all seeing positive trends and good tailwinds and the company embarked on its big new capex due to the growth expectations arising from these trends. It remains to be seen how the India market shapes up for BKT in going forward and how the company’s plans for the new capex pans out. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q3FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 2141 | 1555 | 37.6% | 2182 | -1.8% | 6215 | 4115 | 51.0% |

| PBT | 438 | 424 | 3.3% | 542 | -19.1% | 1466 | 1036 | 41.5% |

| PAT | 328 | 321 | 2.1% | 377 | -12.9% | 1037 | 783 | 32.4% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 2158 | 1563 | 38% | 2205 | -2.1% | 6249 | 4140 | 50.9% |

| PBT | 450 | 427 | 5.3% | 557 | -19.2% | 1491 | 1052 | 41.7% |

| PAT | 338 | 325 | 4% | 391 | -13.5% | 1060 | 797 | 32.9% |

Detailed Results:

- The revenue for the quarter grew 38% YoY & -2.7% QoQ in consolidated terms.

- PBT was up 3.3% YoY & 5.3% YoY in standalone and consolidated terms in Q3.

- Consolidated PAT was up 4% YoY in the quarter.

- Sales volumes for the quarter came in at 70,320 metric tons which were up 18% YoY.

- The EBITDA margin fell 750 bps YoY to 24.4% in Q3.

- The company announced a third interim dividend of Rs 4 per share.

- The company also declared a special dividend of Rs 12 per share.

- Sales breakup in 9M for the company is:

- Agri-65.6%, OTR-31.1%, Others-3.3%.

- Replacement-69.6%, OEM-27.1%, Others-3.3%

- EU-53.8%, Américas-16.6%, India-17.8%, RoW-11.9%

- The company saw a forex gain of Rs 80 Cr in Q3.

- The company remains debt-free with current cash holding at Rs 1927 Cr as of 31th Dec 2021.

- The company raised fixed rate liability of Rs 500 Cr from EU at an effective interest rate of 0.055% for 3.5 years in Q2.

- The old Waluj plant will be upgraded with the capex required for this to be at Rs 350 Cr and this new capacity will come online in Q3FY23.

- The company is aiming to reach an achievable capacity of 3.6 Lac tons per year by the end of FY23.

- The company has revised its volume guidance to 275,000 – 285,000 MT.

Investor Conference Call Highlights

- The company continues to face macro challenges such as raw materials cost and logistics.

- The brownfield capex at Bhuj announced on February ‘21 will add 50,000 metric ton per annum capacity and the revamp of the old waluj plant will add 25,000 metric ton per annum.

- During 9M for FY ’22, the PAT was impacted by the crystallization of the contingent liabilities of 65.4 crores post completion of certain tax assessments.

- The gross debt stood at Rs 1881 Cr for BKT. The company has completed Rs 912 Cr of capex in 9M of which Rs 852 Cr was spent on the new capex program of Rs 2250 Cr.

- The company had taken a 2%-3% price increase in the beginning of Q3.

- The company’s current market share in the global OHT market is 5%. The market growth for the industry is 3%-4%. The management expects this market growth rate to continue going forward for a few years.

- The company’s marketing expenses are about Rs 120 – 130 Cr every year. The management expects for this to continue going forward.

- The management states that there will be 100% capacity utilisation during the upcoming quarters.

- The company is not planning to change the product mix to increase its per ton realisations during capacity shortages, but may take further price hikes as per the competitive scenario.

- The synthetic rubber costs for the company remained the same, whereas the natural rubber costs went up by more than 20% during the quarter.

- The management sees natural rubber prices remaining stable with a slight increase for some time ahead.

- The Euro hedge rate for the quarter is at 87.3 and for the year is at 89.6.

- The management expects the OEM segment to sustain on the levels it has reached.

- Carbon Black sales to third parties was 17% of the company’s capacity which contributed to about 3% of the overall sales revenue.

- The outlook by the management for Q4 and the upcoming quarters remains the same due to the bottleneck of capacity shortage.

- The company has seen better demand in recent quarters in Europe for industrial, construction and OTR.

- Once the company’s capacity increases to 360,000 ton; the carbon black capacity needed would be 90K-100K ton.

- The company is setting up a new captive power plant at Bhuj which will be completed during the ongoing expansion.

- The company is also increasing investments into solar to reduce dependency and costs.

- At Bhuj, the plant is supplied 80% power needs through captive power plants and at other plants 40% power needs are supplied through solar and windmills.

- The price difference of the company’s products with its American counterparts is currently 12%-15%. The company looks to maintain this for the short term.

- The management expects the volumes to remain flat for next few quarters due to supply constraints after which there will be a sudden jump after capex plans get finished.

- The OEM margins and replacement margins are almost similar for the company.

- The management’s endeavour is to sustain 10%-12% volume growth each year.

- The company has 10%-12% market share in the European Agri tyres market.

Analyst’s View:

BKT has been a rising player in the off-road tires business for years now. The company witnessed another phenomenal quarter with 38% YoY growth in sales but PAT up only 4% YoY. BKT is seeing continuous growth in North America while the India market was stagnant in Q3. It is looking to maintain a steady EBITDA margin of 28-30% and has done a price increase of 2-3% in October to preserve margins despite rising RM & logistics costs. The management maintains that the end industries are all seeing positive trends and good tailwinds and the company embarked on its big new capex due to the growth expectations arising from these trends. It remains to be seen how the India market shapes up for BKT in going forward and how the company’s plans for the new capex pans out. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q2FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 2182 | 1597 | 36.6% | 1891 | 15.38% | 4074 | 2559 | 59.2% |

| PBT | 542 | 450 | 20.4% | 484 | 11.98% | 1027 | 612 | 67.8% |

| PAT | 377 | 339 | 11.2% | 331 | 13.89% | 708 | 461 | 53.5% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 2205 | 1598 | 38% | 1885 | 17% | 4090 | 2576 | 58.77% |

| PBT | 557 | 452 | 23.2% | 484 | 15% | 1041 | 624 | 66.82% |

| PAT | 391 | 340 | 15% | 330 | 18.5% | 721 | 472 | 52.75% |

Detailed Results:

- The revenue for the quarter grew 38% YoY & 17% QoQ in consolidated terms.

- PBT was up 20.4% YoY & 23.2% YoY in standalone and consolidated terms in Q2.

- Consolidated PAT was up 15% YoY in the quarter.

- Sales volumes for the quarter came in at 72,748 metric tons which were up 19% YoY which was also its highest ever quarterly sales volume.

- The EBITDA margin fell 683 bps YoY to 27.1% in Q2.

- The company announced a second interim dividend of Rs 4 per share.

- Sales breakup in H1 for the company is:

- Agri-65.8%, OTR-30.9%, Others-3.3%.

- Replacement-70.3%, OEM-26.7%, Others-3%

- EU-54%, Americas-16.7%, India-17.3%, RoW-12%

- The company saw a forex gain of Rs 71 Cr in Q2.

- The company remains debt-free with current cash holding at Rs 1659 Cr as of 30th Sept 2021.

- The company raised fixed rate liability of Rs 500 Cr from EU at an effective interest rate of 0.055% for 3.5 years in Q2.

- The old Waluj plant will be upgraded with the capex required for this to be at Rs 350 Cr and this new capacity will come online in Q3FY23.

- The company is aiming to reach achievable capacity of 3.6 Lac tons per year by the end of FY23.

- The company has revised its volume guidance to 275,000 – 285,000 MT.

Investor Conference Call Highlights

- To meet the buoyant demands, the board has decided to continue operations at the old Waluj plant and to upgrade it.

- The gross debt stood at Rs 1443 Cr for BKT. The company has completed Rs 838 Cr of capex in H1 of which Rs 700 Cr was from the planned Rs 1900 Capex plan.

- The management states that some portion of the incremental logistics cost has been passed on to the customers, making the QoQ average selling price higher.

- The company has reported lower RM costs compared to the sharp inflation because of passing on and recovering the shipping costs.

- The earlier realization was INR 266 which is currently INR 286, so the company has passed on 2% to 3%. The management expects the realizations to remain at current levels only going ahead.

- The management sees a 2% to 3% cost increase in RM costs due to rising crude prices.

- The management is proposing to take another price hike from January to cope with the cost increases.

- BKT will do around Rs 400 crore capex in H2 out of the revised capex target of Rs 1100 crore for FY22.

- The management sees stability in freight costs for the ahead quarter with prices remaining high and also accepts that the availability of containers has been an issue for the company.

- The current capacity of the company stands at 285k MTPA.

- The overall market share for BKT has grown to 4-4.5% while in OHT, BKT has a market share of 5.5% to 6% currently.

- The management says that its long-term endeavor is to maintain an EBITDA margin of 28% to 30%. It expects the company to deliver in this range for the year.

- The total shipping cost is 6-7% from 2-3 % in the past, out of which half has been passed on to the customers.

- The revenue share for Mining has gone up from 8% to 13% for BKT. OTR and Industrial segments account for 31% of revenues.

- Currently, the company is operating at 100% capacity utilization because of demand exceeding supply.

- The management is seeing good demand in the European Tractor replacement market and is expecting it to continue.

- The management says that the marketing and branding are helping the company to consistently outperform in prolonged downturns in the markets.

- The management says that for capacity constraints after the completion of the current capex, it will do another round of brownfield expansion in Q3 next year which would be completed in 12 months.

- The management remains committed to reaching a 10% market share in the OHT segment from the current market share of 6%.

- Raw material costs of the company have increased more compared to peers because of continuous buying of inventory for longer periods. The lag time for the increased raw material prices to reflect is 2 months.

- Globally the company is spending at Rs 130-140 Cr on A&P annually and it plans to continue on this level.

- The current inventory level is at 1.5 to 2 months.

- Carbon black sales volume for H1 was at 9k tons, about Rs 88 Cr in value which is around 3% of revenues.

- The payback period for the brownfield expansion is expected to be at 4 years and for greenfield expansion, it is expected to be at 5 to 6 years.

- In India volumes, 40% is from Agri and 60% is from Industrial, Construction, and OTR.

Analyst’s View:

BKT has been a rising player in the off-road tires business for years now. The company witnessed another phenomenal quarter with its highest ever quarterly sales volumes ever sold and highest ever quarterly revenues. BKT is seeing continuous growth in North America while the India market was stagnant in Q2. It is looking to maintain a steady EBITDA margin of 28-30% and has done a price increase of 2-3% in July to preserve margins despite rising RM & logistics costs. The management maintains that the end industries are all seeing positive trends and good tailwinds and the company embarked on its big new capex due to the growth expectations arising from these trends. It remains to be seen how the India market shapes up for BKT in going forward and how the company’s plans for the new capex pans out. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q1FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 1891 | 962 | 96.57% | 1804 | 4.82% |

| PBT | 485 | 162 | 199.38% | 495 | -2.02% |

| PAT | 331 | 122 | 171.31% | 372 | -11.02% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 1885 | 979 | 92.54% | 1815 | 3.86% |

| PBT | 484 | 172 | 181% | 503 | -3.78% |

| PAT | 331 | 132 | 151% | 380 | -12.89% |

Detailed Results:

- The revenue for the quarter grew 93% YoY & 4% QoQ in consolidated terms.

- PBT was up 199% YoY & 181% YoY in standalone and consolidated terms in Q1.

- Consolidated PAT was up 151% YoY in the quarter.

- Sales volumes for the quarter came in at 68,608 tons which were up 80% YoY which was also its highest ever quarterly sales volume.

- The EBITDA margin improved 169 bps YoY to 29.2% in Q1.

- The company announced a interim dividend for FY22 of Rs 4 per share.

- Sales breakup in Q1 for the company is:

- Agri-65.9%, OTR-30.9%, Others-3.2%.

- Replacement-71.9%, OEM-25.6%, Others-2.6%

- EU-52.7%, Americas-16.1%, India-19%, RoW-12.2%

- The company saw a forex gain of Rs 38 Cr in Q1.

- The company remains debt-free with current cash holding at Rs 1557 Cr as of 30th June 2021.

Investor Conference Call Highlights

- The margins profile for the company is expected to be dragged in the next quarter due to raw material prices and logistics costs staying up.

- The company has taken price increases at the end of the quarter and the management maintains that it will keep EBITDA margins in the range of 28-30%.

- The company did Rs 366 Cr of capex in Q1. Around Rs 200 Cr of this Q1 capex was from the multi-year capex program of Rs 1900 Cr.

- The management is guiding for sales volumes of 250,000 to 265,000 MT in FY22.

- The price increase in July was at 2-3% for BKT.

- The management expects demand to stay strong and expand in the coming years and thus it had decided on the multi-year capex plan.

- The current capacity is 285,000 MTPA for BKT.

- The management states that all end industry segments are seeing positive trends with good tailwinds in all spaces.

- Despite the rise in demand, the company doesn’t have any understocking issues according to the management.

- USA has seen good growth for the business in recent quarters.

- The pricing gap between BKT and international competitors will narrow over time as the company will strive to build its brand and use it to get better prices and reduce dependence on the pricing advantage to keep up demand.

- At the base level, inventory at dealer level is at 40-45 days. Due to the rise in demand the dealer inventory levels fell to 20-25 days and it has now come back to 35-40 days.

- The company is indeed working on innovation and products that may be part of rising niches like EVs in agriculture or mining, but it is too early to tell on these developments according to the management.

- Other expenses have gone up 90 bps QoQ mainly due to a rise in logistics costs.

- The company will continue to maintain brand building spend at Rs 120 Cr at the aggregate level.

- The contribution from India has fallen from 23% in Q4FY21 to 19% in Q1 due to loss of operations from state lockdowns during the 2nd wave of COVID-19 which was going in April and May.

- The company’s utilization levels are nearing the peak level but the management is confident that the new capex will be online by the time it hits peak level.

- Although there have been floods in Germany which is a key market for BKT, it doesn’t seem to have had much effect on the demand situation in the region.

- The company expects good demand in the OTR segment from South America, Africa, and Australia.

- The company is indeed on the lookout for possible acquisitions, but it is looking for prospects in India only at the moment.

- The global Agri and OTR tire space is growing at a CAGR of 3-5% while BKT has a market share of 5-5.5% currently.

- The full-year capex for FY22 is expected to be around Rs 900-1000 Cr.

- Excluding China, the company’s global market share would be at 7-8%.

- In India, the company is pricing its products in the premium range and is on par with top manufacturers.

- Most of the volume growth has come from the existing distributor network and the company has not done any major distribution expansion in the last 1 year and has instead worked on identifying current network gaps and filling these gaps.

- The management has admitted that the China Plus One strategy that is present in many manufacturing industries is not going on in the international tires market.

Analyst’s View:

BKT has been a rising player in the off-road tires business for years now. The company witnessed another phenomenal quarter with its highest ever quarterly sales volumes ever sold and highest ever quarterly revenues. BKT is seeing continuous growth in North America while the India market was stagnant in Q1 due to state lockdowns. It is also looking to keep growing with a steady EBITDA margin of 28-30% and has even done a price increase of 2-3% in July to preserve margins despite rising RM & logistics costs. The management maintains that the end industries are all seeing positive trends and good tailwinds and the company embarked on its big new capex due to the growth expectations arising from these trends. It remains to be seen how the India market shapes up for BKT in going forward and how the company’s plans for the new capex pans out. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q4FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1804 | 1424 | 26.69% | 1556 | 15.94% | 5919 | 5031 | 17.65% |

| PBT | 495 | 339 | 46.02% | 424 | 16.75% | 1531 | 1123 | 36.33% |

| PAT | 372 | 257 | 44.75% | 322 | 15.53% | 1155 | 945 | 22.22% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1815 | 1438 | 26.22% | 1564 | 16.05% | 5955 | 5062 | 17.64% |

| PBT | 503 | 346 | 45% | 428 | 17.52% | 1555 | 1140 | 36.40% |

| PAT | 380 | 265 | 43% | 325 | 16.92% | 1178 | 960 | 22.71% |

Detailed Results

- The revenue for the quarter grew 26% YoY in consolidated terms.

- PBT was up 46% YoY & 45% YoY in standalone and consolidated terms in Q4.

- Consolidated PAT was up 43% YoY in the quarter.

- FY21 figures were also very good with revenues rising 18% YoY while PBT and PAT rose 36% YoY and 23% YoY respectively.

- Sales volumes for the quarter came in at 68,002 tons which were up 17% YoY which was also its highest ever quarterly sales volume.

- The EBITDA margin improved 254 bps YoY to 31.9% in Q4.

- The company announced a final dividend for FY21 of Rs 5 per share.

- Sales breakup in FY21 for the company is:

- Agri-64%, OTR-32%, Others-4%.

- Replacement-70%, OEM-26%, Others-4%

- EU-50%, Americas-15%, India-23%, RoW-13%

- The company remains debt-free with current cash holding at Rs 1475 Cr as of 31st Mar 2021.

Investor Conference Call Highlights

- FY21 sales volumes were at 227,131 metric tons.

- The management is guiding for sales volume between 250,000 to 265,000 metric tons in FY22.

- The greenfield tire project in Waluj is going as scheduled. The project is expected to be completed by 30th September 2021.

- The total new capex of Rs 1900 Cr is expected to be done by H1FY23.

- Other income for the quarter stood at INR 20 crores, while unrealized gains stood at INR 23 crores. For financial year ’21, other income stood at INR 119 crores, while unrealized gains stood at INR 18 crores.

- The gross debt stood at INR 893 crores.

- RM prices are expected to have risen 3-4% in Q1. The company has passed on the price increases to customers by doing a price increase in Jan & April.

- The management is expecting to see immediate capacity rise from debottlenecking, but it remains confident of delivering on the volume guidance for FY22.

- Capex guidance for FY22 is Rs 800-850 Cr including maintenance capex.

- The majority of the Rs 1900 Cr capex is for upgrading and automation of the existing tire plant. CapEx for the carbon plant and the power plant would come a little later.

- The management expects the OTR contribution to rise to 50% in the next few years.

- The main reason for the rise in other expenses in Q4 is the spike in logistics costs. Logistics costs are expected to ease by H2FY22.

- The margin contribution for OTR is the same as the tires from the Agri segment.

- India sales have grown 29% YoY and the company now has a market share of 4-5% here.

- The market size in North America is expected to be as big as EU for BKT.

- The company has also added distribution in the online channel in North America.

- The management states that the demand from OEMs is rising for both agri and OTR segments.

- The lead time from going to the customer to getting feedback on products is around 6-9 months for an OEM customer. Thus, the company will have its feedback ready by the time the capacity expansion is done.

- The management also expects RM prices to rise 4-5% in the next quarter. Availability is not an issue for RM procurement, but logistics is the main issue here.

- The incremental demand is coming from both old and new distribution points with the old ones accounting for the bulk of it.

- The company is holding around 38-40 days of inventory at present.

- The company is currently at 5-6% of the global market share.

- The total A&P spend in FY21 is around Rs 100 Cr. The company is looking to increase it to Rs 120-125 Cr in the coming years with capacity expansion.

- The price gap with international competitors is going to narrow going forward but BKT will maintain a min gap of 12-15% while trying to enhance its brand building. Currently, the price difference is around 20-22%.

- The management has stated that it is looking to maintain an EBITDA margin at 28-30% on a long-term sustainable rate.

Analyst’s View

BKT has been a rising player in the off-road tires business for years now. The company witnessed a phenomenal Q4 with its highest ever quarterly sales volumes ever sold. It has also hiked its volume guidance for FY22 due to a continuous rise in sales. BKT is seeing continuous growth in North America and India markets. It is also looking to keep growing with a steady EBITDA margin of 28-30%. The company is expecting the capex projects to run on schedule. The company is also expecting to see a rise in the OTR segment and both OTR & Agri segments to become equal contributors to sales in a few years. Although RM price inflation is expected in the near term, BKT is looking to pass on any price increases to customers as it has done so since Jan 2021. It remains to be seen how the India market shapes up for BKT in Q1 due to the 2nd wave of COVID-19 and how the company’s plans for the new capex pans out. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q3FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 1556 | 1191 | 30.65% | 1597 | -2.57% | 4115 | 3608 | 14.05% |

| PBT | 424 | 275 | 54.18% | 451 | -5.99% | 1036 | 784 | 32.14% |

| PAT | 322 | 221 | 45.70% | 339 | -5.01% | 783 | 688 | 13.81% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 1564 | 1186 | 31.87% | 1598 | -2.13% | 4141 | 3624 | 14.27% |

| PBT | 428 | 278 | 54% | 452 | -5.31% | 1052 | 793 | 32.66% |

| PAT | 325 | 224 | 45% | 341 | -4.69% | 798 | 695 | 14.82% |

Detailed Results

- The revenue for the quarter grew 32% YoY in consolidated terms.

- PBT was up 54% YoY in standalone and consolidated terms in Q3.

- Consolidated PAT was up 45% YoY in the quarter.

- 9M figures were also very good with revenues rising 14% YoY while PBT and PAT rose 33% YoY and 15% YoY respectively.

- Sales volumes for the quarter came in at 59,810 tons which were up 26% YoY.

- Sales volumes for 9M were up 11% YoY which is very good considering the fall in performance in Q1.

- The EBITDA margin improved 70 bps YoY to 31.9% in Q3.

- The company announced a third interim dividend for FY21 of Rs 5 per share.

- Net forex gain for Q3 was at Rs 15 Cr vs a gain of Rs 6 Cr a year ago.

- Sales breakup in 9M for the company is:

- Agri-64%, OTR-33%, Others-3%.

- Replacement-71%, OEM-25%, Others-4%

- EU-49%, Americas-15%, India-23%, RoW-13%

- The company remains debt-free with current cash holding at Rs 1423 Cr as of 31st Dec 2020.

- The previously guided CapEx programs are on track for the company.

- BKT announced new capex programs of Rs 1900 Cr which included:

- Debottlenecking and Brownfield expansion at Bhuj; Expansion to add ~50,000 MTPA capacity; expected completion by H2FY23; Capex cost of up to Rs 800 Cr.

- Expanding carbon black capacity to 200,000 MTPA including 30,000 MTPA of high value advanced carbon material and Power Plant; Capex cost of up to Rs 650 Cr; expected completion by H1FY23.

- Modernization, automation, and technology upgradation of existing facilities; Capex cost of up to Rs. 450cr; expected to be completed by H1FY23.

Investor Conference Call Highlights

- 9M volumes were at 159,310 MT. the management has increased its volumes guidance for FY21 to 215,000 to 220,000 MT.

- The new facility for 57-inch ultra large giant all-steel radial tire plant of 5,000 MTPA has been completed.

- The carbon black plant has been running at full capacity as third-party sales have also commenced and there is strong acceptance for the product.

- The management has stated that BKT has planned the new capex so that it doesn’t face any capacity constraints from FY23 onwards.

- Production is expected to commence in the greenfield tire plant at Waluj from Q1FY22.

- The management expects payback in 5-6 years on the new capex in the carbon black plant.

- The management has stated that the decision to expand carbon black capacity was taken due to good demand in the market for it and possible future requirements.

- The modernization project will mainly result in manpower reduction and automation of many processes. The impact should not only be reflected in the margin; it will also result in an increase in product quality according to the management.

- The management has stated that because of the market moving towards radialization, equipment upgradation is necessary. It has also clarified that the automation will only be in material handling and movement processes.

- Market share in USA and EU are between 5-6% for BKT.

- Around 25-30% of carbon black capacity is available for third party sales.

- The margin on carbon black sales is at 15-16% which is the industry norm.

- The management has stated that since 75-80% of carbon black is for internal consumption, it should not have any adverse impact on the overall margin for BKT.

- Maintenance capex will vary from Rs 100-200 Cr per year.

- The management has clarified that the Bhuj plant expansion is high because it will also have the automation and modernization aspect included in it.

- The management has reassured that the expansion of the carbon black plant is not at the expense of the tire business and the tire business will remain core for BKT. The carbon black expansion is mainly for pre-empting expansion in tire capacity in the future even after 5-7 years. It has also stated that carbon black capacity expansion cannot be done in small increments and that it should yield certain economies of scale and thus the decision to expand it in a large increment was taken.

- The rated capacity and achievable capacity for carbon black plant are different as the plant is required to be shut down from time to time as per the norms of the pollution boards.

- The management has stated that mostly the advanced variant of carbon black with a capacity of 30,000 Mt will be for third party sales. The margin in this variant should be 4-5% higher than the lower quality one.

- The modernization requirement is necessary as some of the plants like the one in Bhiwadi was formed in 2001-03. The management has stated that the requirement for modernization should come up every 7-10 years.

- Currently carbon black sales account for less than 2% of revenues.

- The company has not seen any opportunities from announced PLI schemes by the Govt of India.

- After abandoning the plan for an overseas plant, the company is looking to make its distributors stronger and getting them to stock more material to keep business close to end customers.

- The company developed small lots for testing which grade of carbon black would be well received and after testing and feedback it concluded to make the advanced carbon black which is basically mid-category that sits above the grade used to make tires and plastic.

- Starting Q4, the company is also going to take some price increase of 2-3% to negate these enhanced costs and maintain EBITDA margins near 28-30%.

- The management has also emphasized that the upgrades are also necessary to be able to compete fairly with international giants so that BKt can continue to compete effectively and doesn’t get left behind by the market leaders.

- The usage of the advanced carbon black will be mainly in print and ink grades and certain high-quality plastic grades.

- Depending on the demand situation, the new capacity can be ramped up to full utilization within 1 quarter after completion.

- Around half of the new capacity will come in H2FY23 and the rest will come in FY24.

- Capex done in FY21 to date is at Rs 600 Cr and around Rs 100-120 Cr is expected in Q4. This is including maintenance capex.

- The company has around 2 months of raw materials inventory at the moment. RM prices have gone up 4-5% in last 2 quarters. BKT is looking to pass on this rise in Q4 and the next quarter.

Analyst’s View

BKT has been a rising player in the off-road tires business for years now. The company witnessed a great Q3 with continued momentum from Q2. It has also hiked its volume guidance for FY21 due to a continuous rise in sales. BKT has also announced a capex plan for Rs 1900 Cr for expansion of the Bhuj plant, expansion of carbon black capacity, and modernization of existing plants. These projects are expected to be completed by H2FY23 and are necessary to maintain momentum and stay competitive according to management. It remains to be seen whether there are any other RM shocks to come for BKT and how the company’s plans for the new capex pans out. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q2FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 1597 | 1152 | 38.63% | 962 | 66.01% | 2559 | 2417 | 5.88% |

| PBT | 451 | 256 | 76.17% | 162 | 178.40% | 612 | 509 | 20.24% |

| PAT | 339 | 291* | 16.49% | 122 | 177.87% | 461 | 467 | -1.28% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 1598 | 1165 | 37.17% | 979 | 63.23% | 2577 | 2438 | 5.70% |

| PBT | 452 | 260 | 73.85% | 172 | 162.79% | 625 | 515 | 21.36% |

| PAT | 341 | 294* | 15.99% | 132 | 158.33% | 473 | 471 | 0.42% |

*includes a negative tax of Rs 35 Cr.

Detailed Results

- The revenue for the quarter grew 37% YoY in consolidated terms.

- PBT was up 76% and 74% YoY in standalone and consolidated terms in Q2.

- Consolidated PAT was up 16% YoY in the quarter.

- Record Sales volumes for the quarter came in at 61,224 tons which were up 61% QoQ and 35% YoY.

- Sales volumes for H1 were up a modest 3% YoY which is very good considering the fall in performance in Q1.

- The EBITDA margin improved 610 bps YoY to 34% in Q2.

- Net forex loss for Q2 was at Rs 4 Cr vs a gain of Rs 55 Cr a year ago.

- Sales breakup for the company is:

- Agri-64%, OTR-33%, Others-3%.

- Replacement-71%, OEM-25%, Others-4%

- EU-51%, Americas-14%, India-23%, RoW-13%

- The company remains debt-free with current cash holding at Rs 1299 Cr as of 30th Sep 2020.

- The previously guided CapEx programs are on track for the company.

- The company announced a 2nd interim dividend of Rs 4 per share.

- The company has become a premium partner for EUROLEAGUE BASKETBALL and is also sponsoring the Tractor of the year (TotY)-EUROPE award.

Investor Conference Call Highlights

- The company’s current capacity is at 3,05,000 MTPA including 5,000 MTPA for ultra-large All Steel radial mining tire.

- Due to some redundancy in product sizes and technology, this capacity can come down to 280,000 MTPA.

- BKT is exploring investments by the way of a brownfield CapEx at existing locations to create capacity.

- The management expects FY21 volumes to exceed FY20 volumes.

- The management is guiding for marginal growth in volumes in FY21 mainly due to the second coming of COVID-19 which is expected to slow down sales momentum in the company’s principal market of EU.

- The inventory buildup since March in the EU has come down significantly and is slowly being built up to normal levels. The company has also gained market share in both Agri and non-agri segments in the region.

- The management maintains that the company’s long term EBITDA margin shall stay in the 28-30% range.

- The company has generally seen a trend of rising rubber prices.

- The company has hedged for euro at 82.4 in Q2 and 83.4 in H1. For FY22, the rate is at 85.

- Production during the quarter was at 61,223 tons.

- The market trend in India is strong and the company is steadily gaining market share. It has also seen a good increase in visibility and brand image due to the sponsorship with IPL 2020.

- The management is aiming to keep expenses at around 21% of sales.

- The company has seen good growth in the OTR segment which has seen this segment revenue share rise to 33% from 20% previously. The company is also optimistic about this segment due to the launch of its ultra-large radial tires.

- The company is gaining good market share in Asia and Australia but is struggling in South America and Africa due to import restrictions in these regions.

- The import ban on tires in India has not had any impact on BKT as it is applicable only to commercial vehicles.

- The company has gotten confirmation from its OEM customers that there will not be any delay in procurement and distributors expect sales to continue despite lockdown in the EU.

- The management insists that the growth in volumes in the EU was organic in nature and was not due to any ban on Chinese tires as there hasn’t been any such ban.

- The EBITDA margin of 34% in Q2 is expected to be a one-off and over the long term, margins are expected to stay in the guided range of 28-30%.

- The company will not be looking to take any impairment charges for the reduced capacity as no machines will be redundant. The existing machines will be repurposed for larger sizes from smaller sizes and this will result in lower overall capacity. This shift towards larger sizes is purely due to current market trends.

- The company will continue to add around 100 SKUs each year.

- The gross margin for Q2 was at 61%. The management state that the sustainable gross margin for the company should be at 58%.

- The management is confident that the reduced capacity will be enough for the company’s growth prospects for the next 2-3 years.

- The carbon black sales are at 2% of overall sales for BKT. This is around 20% of the carbon black capacity for BKT.

- The Capex guidance for Fy21 was at rs 700 Cr out of which Rs 350 Cr is already done. Capex for FY22 should around similar levels. The maintenance Capex should be at Rs 200 Cr per year.

- In the USA, the company is seeing good pull demand due to its branding efforts in the last 2-3 years. It is also increasing its dealer network. The company is also developing USA specific products which should also help the company capture more market share here.

- The brand spending will remain roughly the same at current levels of Rs 100 Cr per year.

- There shouldn’t be a major change in average selling price due to the shifting product mix from the reduction in capacity. The ASP is expected to remain near Rs 250 per kg for the company.

- BKT’s market share is about 5% to 6% in the Indian market. There is good scope for market capture in India for BKT according to the management.

- On average selling price and realization is lower for sales in India as compared to export sales.

Analyst’s View

BKT has been a rising player in the off-road tires business for years now. The company witnessed a tepid Q1 mainly due to the disruption in sales from COVID-19. It has however been able to increase EBITDA margins and volumes YoY in Q2. The company is also expecting sales volumes to grow marginally in FY21 over FY20 which is a testament to the company’s revival post-COVID-19. The company is also looking to shift its product mix more towards larger sizes which are expected to result in marginally lower capacity which the management assures will be enough for growth prospects for the next 2-3 years. It remains to be seen whether there are any other economic shocks to come from COVID-19 and whether the company’s projections of rising demand from Agri and non-Agri sectors pans out as expected. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

Q1FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 962 | 1265 | -23.95% | 1424 | -32.44% |

| PBT | 162 | 254 | -36.22% | 339 | -52.21% |

| PAT | 122 | 176 | -30.68% | 257 | -52.53% |

| Consolidated Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 979 | 1273 | -23.10% | 1438 | -31.92% |

| PBT | 172 | 255 | -32.55% | 346 | -50.29% |

| PAT | 132 | 177 | -25.42% | 265 | -50.19% |

Detailed Results

-

- The revenue for the quarter declined 23% YoY in consolidated terms.

- PBT was down 36% and 23% YoY in standalone and consolidated terms in Q1.

- Consolidated PAT fell 25% YoY in the quarter.

- Sales volumes for the quarter came in at 38,096 tons which were down 25% YoY.

- The EBITDA margin improved 240 bps YoY to 26.7% in Q1.

- Net forex gain for Q1 was at Rs 13 Cr vs Rs 24 Cr a year ago.

- The company remains debt-free with current cash holding at Rs 1175 Cr as of 30th June 2020.

- The previously guided CapEx programs are on track for the company.

- The company announced an interim dividend of Rs 3 per share.

Investor Conference Call Highlights

- The non-agriculture segment is moving slowly on account of low commodity prices and end-user demand while the agriculture segment is showing strong demand across all geographies.

- The rise in EBITDA margin was mainly on account of lower absorption of fixed cost owing to lower production and sales.

- The market share for BKT in India currently is 7% and it is steadily increasing in this segment.

- Around 40-45% of domestic sales are from tractors.

- The management remains confident of achieving flat revenues for the year. BKT will continue to maintain the percentage of spend in sponsorships and other promoting methods at current levels which is at 2-3% of sales.

- Domestic growth was flat in Q1 while exports starting rising from June.

- The management does not expect much change in RM prices going forward. It has also mentioned that there will no further pricing action in FY21.

- Volumes produced for the quarter was at 41,576 tons.

- The management expects the non-Agri segment to pick up as construction and mining activities resume across the world.

- Volumes sold in the EU were at 20,000-21,000 tons while India has volumes of 9,400 tons. The USA saw volumes of 3000-4000 tons.

- 65% of volumes for Agri tires while 32% were for OTR. The remaining 3% was for smaller sized tires.

- OEM was at 27% while the replacement was at 70%.

- EU Agri segment market share for BKT is at 12-15%. The same figure in the USA is at 7-10%.

- The management is aspiring for BKT to improve in the non-Agri segment like mining, etc to reach its goal of 10% overall industry market share.

- The company does not expect any import duty restriction to come into place for imported rubber.

- There has been no change in channel inventory in Q1. The current channel inventory in the USA & EU is at 2-3 months.

- Around 15% of carbon black output is being sold on the marketplace.

- The company’s medium-term target is to increase the proportion of sales from India from the current level of 20-22%.

- The industry is widely expected to grow at a CAGR of 4-5%.

- The management expects EBITDA margins to remain close to 28-30% in the year ahead.

- There are currently no gaps in the distribution for BKT in India and it is able to maintain a Pan India network of SKUs.

- The management has stated that it does not take any actions to set realizations and change in realizations is largely dependent on forex changes given no pricing action.

- The company is currently facing no issues in the supply chain both for sourcing and dispatching.

- The current prices are fully reflecting the softening in commodity prices.

- The management has stated that the company has made good inroads in the mining sector in the USA and is getting repeat orders and rising market share in the sector. The current market share in this sector is at 2-3% which BKT hopes to increase to 5-6% in the next 2-3 years.

Analyst’s View

BKT has been a rising player in the off-road tires business for years now. The company has seen a tepid Q1 mainly due to the disruption in sales from COVID-19. It has however been able to increase EBITDA margins YoY. The addition of the carbon black plant is expected to bring about additional margin appreciation for the company bringing the guidance for FY21 at 28-31%. Although the company was hit by supply chain disruptions due to the lockdown it didn’t hamper its sales in the EU & USA since the channel inventory here is at 2-3 months. It remains to be seen whether there are any other economic shocks to come from COVID-19 and whether the company’s projections of rising demand from Agri and non-Agri sectors pans out as expected. Nonetheless, given the company’s sustained margin performance, its resilient market share in a slow global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

If you’d like to read our detailed analysis on BKT’s moat please click here.

Q4FY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 1424 | 1391 | 2.37% | 1191 | 19.56% | 5031 | 5459 | -7.84% |

| PBT | 339 | 276 | 22.83% | 275 | 23.27% | 1123 | 1183 | -5.07% |

| PAT | 257 | 185 | 38.92% | 221 | 16.29% | 945 | 782 | 20.84% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 1438 | 1397 | 2.93% | 1186 | 21.25% | 5062 | 5428 | -6.74% |

| PBT | 346 | 278 | 24.46% | 278 | 24.46% | 1140 | 1177 | -3.14% |

| PAT | 265 | 186 | 42.47% | 224 | 18.30% | 960 | 774 | 24.03% |

Detailed Results

-

- The revenue growth for the quarter was modest at a 3% rise in consolidated terms.

- PBT was up 23% and 24.5% YoY in standalone and consolidated terms in Q4.

- PAT rose 39% YoY in the quarter mainly on account of the reduction in the tax rate and improvement in margins.

- Sales volumes for the quarter came in at 57,966 tons which were up 5% YoY. It was also the highest ever quarterly sales volume sold by the company.

- Overall volumes for FY20 fell 4% YoY.

- The EBITDA margin improved 450 bps YoY to 29.3% in Q4. In FY20, EBITDA margins improved 140 bps YoY to 28.2%.

- Net forex gain for FY20 was at Rs 131 Cr vs Rs 128 Cr a year ago.

- The company remains debt-free with current cash holding at Rs 1086 Cr.

- The previously guided CapEx programs are on track for the company despite some delay caused by COVID-19 disruption.

Investor Conference Call Highlights

- The Capex spending in FY21 is expected to be around Rs 600 Cr.

- The revenue distribution for Q4 & FY20 according to geography is as follows:

- EU: (Q4 58%) (FY20 51%)

- India: (Q4 17%) (FY20 20%)

- USA: (Q4 15%) (FY20 17%)

- ROW: (Q4 10%) (FY20 12%)

- The management has stated that demand from retail for the company’s products remains stable especially from the construction industry.

- The management has stated that out of the total 2 lac tons of carbon black production, the company will be using only 55000-56000 tons and the rest will be sold to outsiders.

- The company didn’t face any difficulty from the partial shutdowns in the EU mainly as agricultural demand remained stable and distributors generally keep 2-3 months of inventory which was enough to meet the immediate demands.

- The RM cost for the company has come down 3-4% QoQ.

- The management remains optimistic about customer demand in FY21 mainly on the back of expectations of good agricultural seasons in the company’s principal markets.

- In the 2 ongoing projects in Bhuj and Waluj, the company expects to do CAPEX of Rs 500 Cr in FY21 and the timeline for these projects shouldn’t get delayed by more than one quarter off from the regular schedule.

- The company has a run rate of Rs 150 Cr per year for maintenance CAPEX.

- Ad expenses are expected to be Rs 75-90 Cr each year on the sports leagues while ocean freight is around 6-7% of exports. The overall promotional spending is expected to stay stable at around Rs 280 Cr each year.

- The sales volumes breakup according to industry segments is:

- Agri: 65%

- OTR: 31-32%

- Others: 3%+

- The sales breakup between replacement and OEM is 71% and 25% respectively. The offtake is around 4-5%.

- The management gross margins to stay stable near 58-60% in the long term.

- The company sources only 10-12% of raw materials from China.

- The management does not expect any large volatility in raw material prices going forward.

- IN raw materials sourced by the company, 35% is natural rubber, 3% is lead wire and the rest 62% is crude derivatives.

- The incremental margin benefit from carbon black in Fy21 is expected to be around 100-150 bps.

- The company is seeing good traction in France and has also reported a market share gain of 10-20 bps.

- The management has stated that any decrease in raw material prices will be passed on directly to the customers.

- The current capacity utilization level is at 70%.

- The company did not face any major issues from labour migration at any of its plants.

- The company has a market share of 5-6% in India today. Most of this is through replacement. The company is working hard to develop the OEM market in India.

- The industry OEM: replacement mix is 45:55.

- The management is optimistic of maintaining EBITDA margins near 30% in the coming times.

- The EBITDA guidance for FY21 is around 28-30%.

Analyst’s View

BKT has been a rising player in the off-road tires business for years now. The company has done well to bounce back in Q4 and record its highest ever quarterly sales volumes. It has also brought about margin expansion while doing so. The addition of the carbon black plant is expected to bring about additional margin appreciation for the company. Although the company was hit by supply chain disruptions due to the lockdown it didn’t hamper its sales in the EU. It remains to be seen whether there are any other economic shocks to come from COVID-19 and whether the expectations of normal agricultural seasons in the company’s principal markets pan out in expected manner. Nonetheless, given the company’s sustained margin performance, its resilient market share in a stagnant global market, and the rapid rise of the company in India, Balkrishna Industries is a good tire stock to watch out for.

If you’d like to read our detailed analysis on BKT’s moat please click here.

Q3FY20 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY20 | Q3FY19 | YoY % | Q2FY20 | QoQ % | 9MFY20 | 9MFY19 | YoY% | |

| Sales | 1190.56 | 1206.56 | -1.33% | 1151.93 | 3.35% | 3607.57 | 4067.52 | -11.31% |

| PBT | 274.83 | 216.5 | 26.94% | 255.69 | 7.49% | 784.07 | 907.13 | -13.57% |

| PAT | 220.68 | 144.7 | 52.51% | 291 | -24.16% | 687.68 | 597.26 | 15.14% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY20 | Q3FY19 | YoY % | Q2FY20 | QoQ % | 9MFY20 | 9MFY19 | YoY% | |

| Sales | 1186.41 | 1200.59 | -1.18% | 1165.02 | 1.84% | 3624.26 | 4034.39 | -10.17% |

| PBT | 278.27 | 222.43 | 25.10% | 259.79 | 7.11% | 793.21 | 897.72 | -11.64% |

| PAT | 223.8 | 150.98 | 48.23% | 294.31 | -23.96% | 694.95 | 586.41 | 18.51% |

Detailed Results

-

- The revenue for the quarter was flat at a 1.2% decline in consolidated terms.

- PBT was up 27% and 25% YoY in standalone and consolidated terms.

- PAT rose 48% YoY in the quarter mainly on account of the reduction in the tax rate and improvement in margins.

- Sales volumes for the quarter came in at 47,321 tons which is up 1% YoY.

- The EBITDA margin improved to 31.2% in Q3. The company also announced a dividend of Rs 16 per share.

- The markets continue to remain challenging due to environmental conditions in Europe and unfavourable macro-economic situations across the globe. The company expects better growth in FY21 from improving global macroeconomic conditions and the expectation of better weather conditions.

- The company has maintained its volume guidance for FY20 to minor decline.

- The company is establishing its brand in Canada by becoming the title sponsor of Continental Cup Curling in 2020.

Investor Conference Call Highlights

- The company is expected to be seeing the full benefit of phase 1 of the Carbon Black plant from H2 onwards.

- The management stated that the demand slowdown has been seen in the OTR segment across all geographies.

- The CAPEX for the Bhuj plant is expected to be done by the end of FY21.

- The management reports that they are getting the expected benefits in terms of margins and efficiencies as expected.

- The raw material prices have declined in the quarter which has helped the margins to improve.

- The management guides that present levels of gross margins should persist given there is no big surprise in raw material costs.

- The geographical volume is as follows:

- EU: 47%

- USA: 19%

- India: 20%

- Rest of World: 13%

- The management expects the geographical mix to be broadly the same and the contribution of India rising to almost 25%.

- The company is hedging 70-75% of its revenues at a rate of Rs 79-80 for a Euro.

- The total CAPEX in FY20 is expected to be around Rs 600 to 700 Cr. The CAPEX leftover for the rest of the year is around Rs 250 to 300 Cr. The CAPEX planned for FY21 is around Rs 600 Cr.

- The volume breakup is as follows:

- OTR: 36% share Up 10%

- Agriculture: 60% share Down <10%

- ATV & Others: 4% share

- The replacement market counts for 73% while OEM counts for 25% with off-take accounting for the rest of 2.5-3%.

- The management has guided that the current run rate of marketing expenses is expected to continue in FY21 as well.

- The company has maintained its market share in the Agri market of 8% and in OTR of 2%-2.5%.

- The company has taken a price reduction in line with the reduction in raw material costs which maintains the gap of 10%-15% in prices between it and its peers.

- The company continues to strengthen its distribution in the USA as its products get higher market adoption in the replacement market.

- All players in the market are maintaining a cautious stance with good pricing discipline and not pursuing market share by slashing selling prices.

- The company aspires to reach a market share of 10% in the global market in the next 3 years and the management is doing its best with the brand building to help achieve this figure.

- The management admits that the overall outlook across all segments and geographies remains challenging and they will probably see some volume decline in the year.

- The management expects H2 to be flat in terms of volumes and overall volumes of FY20 to decline almost 5% YoY.

- There has been a serious decline in the Agri tires industry of 20%-25% in the year so far.

- The management has maintained that they will not engage in price reductions to gain extra market share as reducing the prices unnecessarily will dilute the brand value.

- Latin America does not feature too high on the company’s priorities at the moment and they will revisit their plans for the region in the future.

Analyst’s View

BKT has been a rising player in the off-road tires business for years now. They have indeed suffered from volume contraction of 14% YoY but they remain committed to the CAPEX plans. The company has stayed true to its commitment of increasing brand presence to drive growth in India and abroad, all of which is evident from its various branding initiatives and incremental advertising costs. As mentioned above, the broad industry is in a slowdown and it remains to be seen how long these conditions persist. Nonetheless, BKT remains a good stock to keep an eye on considering their resilient performance and their efforts to keep margins stable and maintain their pricing advantage over their competition in such difficult industry conditions.

If you’d like to read our detailed analysis on BKT’s moat please click here.

Q2 2020 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY20 | Q2FY19 | YoY % | Q1FY20 | QoQ % | H1FY20 | H1FY19 | YoY% | |

| Sales | 1151.93 | 1416.34 | -18.67% | 1265.08 | -8.94% | 2417 | 2860.96 | -15.52% |

| PBT | 255.69 | 338.22 | -24.40% | 253.55 | 0.84% | 509.24 | 690.63 | -26.26% |

| PAT | 291 | 222.31 | 30.90% | 176 | 65.34% | 467 | 452.56 | 3.19% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY20 | Q2FY19 | YoY % | Q1FY20 | QoQ % | H1FY20 | H1FY19 | YoY% | |

| Sales | 1165 | 1403.12 | -16.97% | 1272.83 | -8.47% | 2437.85 | 2833.8 | -13.97% |

| PBT | 259.79 | 327.4 | -20.65% | 255.15 | 1.82% | 514.94 | 675.28 | -23.74% |