About the Company

Bajaj Finance is engaged in the business of lending. BFL has a diversified lending portfolio across retail, SME and commercial customers with a significant presence in urban and rural India. It also accepts public and corporate deposits and offers a variety of financial services products to its customers.

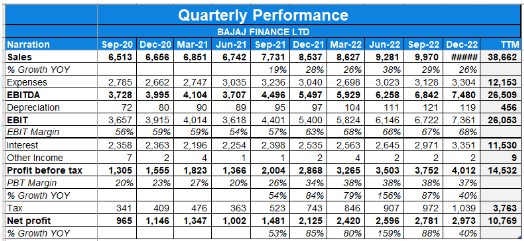

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results:

- Financial metrics showed core AUM grew 29% to INR2,47,000 crores

- PAT was at an ever-high of INR3,158 crores, with a growth of 30% in Q4.

- Gross NPA was the lowest ever in the history of the company, and net NPA came in at 34 basis points ending March ’23.

- Profit before tax grew 52%, and profit after tax grew by 53% to INR302 crores in the quarter gone by.

- The financials are showing growth across various metrics, with core assets under management growing by 29%, total income growing by 32%, net interest income growing by 28%, operating expenses growing by 27%, loan losses growing by 22%, and profits growing by 31%.

- ROE for the full year came in at 5.31%, and operating expenses to net interest income came in at 35.1%. ROE came in at 23.5%.

Investor Conference Call Highlights

- Bajaj Finance Limited had an excellent Q4 FY ’23, with core AUM growth of INR16,500 crores.

- The company stated that all products and services are now live on the web and app platform, and the app platform alone has 35.5 million net users.

- The company disbursed 29.6 million loans and added 11.6 million new customers, the highest-ever customer addition for the company.

- The company is confident about growth and portfolio metrics for FY ’24, with core AUM growth of 29% and opex-to-NIM at 35.1%.

- The company stated that NII grew 28% and opex-to-NIM continues its downward trajectory.

- The company added 19 locations and ended the year at 3,733 locations, with plans to add 150 new locations and over 300 stand-alone gold loan branches in Q1 alone.

- The company stated that credit cost is under INR860 crores, with GNPA at the lowest ever at 94 basis points and net NPA at 34 basis points.

- The company stated that all portfolios, including the auto finance portfolio, are green with 93.28% of the portfolio current.

- The company stated that Capital adequacy remains strong with ROE at 23.46% and ROA in Q4 at 5.4%.

- BHFL had a good quarter, with AUM up 30% to INR69,228 crores, driven by 24% growth in home loans.

- The company stated that loans against property grew by 4%, LRD grew by 64%, and developer finance grew by 92% on a lower base.

- The company stated that operating efficiencies were improved, with net interest income for BHFL growing 40%, and Opex-to-NII standing at 26.5% versus a year ago of 32.5%.

- The company stated that asset quality remains rock-solid, with GNPA and NNPA at 22 basis points, which is one of the lowest in the industry.

- The company stated that Bajaj Financial Securities is not a material subsidiary at this point in time.

- The company has recommended a dividend of INR30 per equity share of 1,500%.

- The company will publish a set of Web metrics that they will start to populate every quarter from Q2 onwards.

- The company stated that there has been significant progress in the payments business, with new features like Contact Mapper capability and UPI Autopay functionality going live. The company continues to invest in the payments business, with new payment CLP, refer and earn functionality, and faster settlement for merchants going live.

- The company is accelerating the deployment of QR codes, with a goal of deploying anywhere between 2.1 million to 2.5 million merchant QR codes of Bajaj Pay in FY ‘2

- The company stated that Core assets grew 29%, total income grew 31%, NIM grew 32%, and loan losses de-grew 34%, resulting in a 64% growth in profits.

- The company added 3.1 million new customers to the franchise in Q4, giving reasonable confidence that they can maintain 11 million to 12 million customer franchise growth in the near term.

- The company is strongly positioned with respect to stage-wise ECL, with a PCR of 64% on Stage 3, 31% on Stage 2, and 80 basis points on Stage 1.

- The company stated that personal loan disbursement growth is rapid, “which is a risk business, not a balance sheet business.”

- The company stated that margin moderation is expected in FY ’24 due to interest rate hikes, with a 40 to 50 basis points impact on NIM on a full-year basis.

- The company stated that capacity planning has been closely looked at in the last 120 days.

- The company has significantly ramped up staffing in the sales finance part of its business, and it has yielded significant results in the last 60-75 days. They expect to dispense 35 million loans in FY ’24, which would be a 20% growth.

- Bajaj Auto’s announcement of applying for an NBFC license is not expected to have a significant impact on the company’s business as it is only 5% of its balance sheet today and is essentially captive.

- The company stated that India seems well placed to grow at 6% and above and consumer credit growth is strong.

- The company expects to grow 28-29% on a consolidated basis with a focus on profitability in FY’24.

- The appointment of two senior colleagues as board members is to augment the bench as the company grows larger and works towards delivering its long-range strategy.

- The reasonable estimate for the company’s subvention market share is between 60% to 65%, and it’s likely to go back to that level in FY’24 in terms of value.

- The company has 30 million banking customers currently every month, and 18 million to 19 million monthly active users on the digital app platform.

- The company stated that the demand for home loans is slower due to higher interest rates and high inflation.

- The company grew 24% in the quarter and 30% on a full-year basis,

- The industry inventory level is at an all-time low, and the company has a lot of headroom to grow.

- The CEO doesn’t want to comment on competition but focuses on realizing the ambition of 100 million consumers and taking a disproportionate share of these consumers’ payments in financial services, with a laser-sharp focus on the frictionless experience.

Analyst’s View

Bajaj Finance is a leading non-banking financial company in India with a strong market position and diversified product portfolio. It is forecast that the total credit will grow from 149 lakh crore to 237 lakh crore and grow by 12.5% CAGR over the next five-year period. Profit per customer would continue to move in tandem and AUM per customer should continue to grow in line with nominal GDP, and return on equity should continue to sustain. The company’s focus on digital innovation, customer-centric approach, and risk management practices have been key drivers of its success. However, like any financial institution, Bajaj Finance is also exposed to certain risks such as credit risk, liquidity risk, and market risk. There was a degrowth in Assets Under Management. Any adverse economic or regulatory changes could impact the company’s performance.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

- AUM grew 27% to just a tad below 2 lakh 31,000 crore.

- Opex to NII came in at 34.7

- B2B disbursements were 16,026 crores on a year-on-year basis, up 6%.

- Cost of funds went up, was 7.14, it increased by 23 basis points, but the overall NIM remained flat, it didn’t dilute.

- Deposits on the balance sheet grew by 3,562 crores, overall now it’s 21% of the balance sheet.

- Loan loss of 841 crores, 1.5% of average asset.

- Capital adequacy remained pretty strong, Tier 1 capital was 23.3%.

- For BHFL the quarter was a little slow.

- Approvals grew 14% at 14,514 crores. Disbursements were 7,429, just a tad below 8,000 crores in Q3 last year.

- It was in the quarter a de-growth but overall, AUM is still up 33% on a nine-month basis to 66,000 crore.

- Cost of funds increased by 49 basis points

- Profit in BFSL came in at 3 crores.

- Balance sheet stack is now down to 9%.

Investor Conference Call Highlights

- Core AUM growth was 12,476 crores, slightly shorter in the mortgage side of the business due to intense pricing pressures.

- Liquidity buffer was strong at just a tad below 13,000 crores.

- The management states that the deposit booking was slower than than the previous two quarters.

- The management states that rate increases in Q3 have been slower than what it was in Q1 and Q2.

- NII growth was 24% in comparison to 28% in Q3 last year. This decrease is due to deregulation of the earnings through IPO financing last year.

- The company continues to hold 1,000 crores of management overlay for uncertainties at this point in time.

- The company took a 41.5% stake in Snapwork Technologies to strengthen our technology roadmap.

- Liquidity buffer was quite strong, as the company was expecting stronger divestment

- Loan losses in Bajaj Housing Finance Ltd were down 50% YoY.

- BHFL also holds a management overlay of 242-odd crores.

- The management stated that They are clearly the lowest risk business in India in terms of mortgages.

- The growth NPA in BFHL was 23 basis points and 10 basis points net NPA

- BFSL added 77,000 customers, 24 locations.

- BFSL upgraded their app and web platform and added 45 new features. They are planning to add another between 15 and 16 new features in Q4

- Service requests are growing quarter- on-quarter, 22 to 25% in BFSL

- Lastly BFSL had a benefit of the IPO financing on account of IPO allocation, they had a 7 crore one-time profit sitting in there.

- Bajaj Finance Ltd is now adding 7,500 to 8,000 merchant QRs on a daily basis.

- The company expects to start becoming visible at the point of sale universally in the next fiscal.

- The company talked about its long strange strategy for the first time which is an annual five-year rolling strategy plan with an execution plan of 12 to 24 months.Strategy is to build an omnipresent financial services company. Wherever the consumer goes, goes to a branch, goes to an app, goes to web, goes to social, goes for reward, and eventually goes virtual, they want to be omnipresent, offering all our products and services.

- The company forecast is that the total credit will grow from 149 lakh crore to 237 lakh crore and grow by 12.5% CAGR over the next five-year period

- Bajaj+, which is so-called finance-plus, in Januaryrolled out, launched New Autos.

- The company has invested the last four years in building out used cars though it has made less money. It is now among the top four, five monthly originators of used cars on the back of that.

- The company launched its new business in June of 2-Wheeler open architecture

- MFI, is a business that the company launched in a phased manner in Q4 and tractor in Q1. On the commercial side, emerging corporate business in Q3, B2B on QR and EDC in Q4

- The seasonality that used to exist at a particular point in time in Q3 and Q1 for us, increasingly has gone away.

- It would continue to generate disproportionately high customers to whom we excel in cross-selling.

- The largest part of Bajaj Finance Ltd’s Opex lines is salary increases because of new hiring.

- The company plans on getting into the MFI business and tractor financing.

- The management states that 55% of the B2B loans are now digital.

Analyst’s View

Bajaj Finance is a leading non-banking financial company in India with a strong market position and diversified product portfolio.It is forecast that the total credit will grow from 149 lakh crore to 237 lakh crore and grow by 12.5% CAGR over the next five-year period. . Profit per customer would continue to move in tandem and AUM per customer should continue to grow in line with nominal GDP, and return on equity should continue to sustain. The company’s focus on digital innovation, customer-centric approach, and risk management practices have been key drivers of its success. However, like any financial institution, Bajaj Finance is also exposed to certain risks such as credit risk, liquidity risk, and market risk. There was a degrowth in Assets Under Management. Any adverse economic or regulatory changes could impact the company’s performance.

Q2 FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 8,606.26 | 6,811.58 | 26.35% | 8,148.19 | 5.62% | 27,871 | 23,546 | 18.37% |

| PBT | 3,335.19 | 1,767.62 | 88.68% | 3,176.29 | 5.00% | 8,586 | 5,363 | 60.10% |

| PAT | 2,472.24 | 1,305.77 | 89.33% | 2,355.92 | 4.94% | 6,350 | 3,955 | 60.56% |

| Consolidated Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 9,972.63 | 7,734.90 | 28.93% | 9,284.55 | 7.41% | 31,640 | 26,683 | 18.58% |

| PBT | 3,752.29 | 2,004.45 | 87.20% | 3,502.76 | 7.12% | 9,504 | 5,992 | 58.61% |

| PAT | 2,780.65 | 1,480.99 | 87.76% | 2,596.25 | 7.10% | 7,028 | 4,420 | 59.00% |

Detailed Results:

- The company had an excellent Q2 with consolidated revenue increasing by 29% YoY & PAT growth of 88% YoY.

- AUM growth of ₹ 14,348 crore in Q2. AUM came in at Rs. 2,18,000 crore, up 31%. Did 6.76 million loans, that is a growth of 7% on a year-on-year basis.

- OpEx to NIM came in at 35.9%.

- PAT came in at Rs. 2,781 crores, a year-on-year growth of 88%.

- ROE came in at just a tad below 23.6%

- Overall capital adequacy remains at 25%

- Net NPA came in at 44 basis points

- NII grew 31%

- Sales finance grew 29%, urban B2C 31%, rural sales finance 33%, rural B2C 34%, SME lending grew 32%, securities lending 67%, commercial lending 36%, and mortgages 31%.

- Overall B2B disbursements grew 15%

- The new customer acquisition is 2.61 million customers.

- Cost of funds because of strong ALM management came in at 6.91% in H1.

- The balance sheet has grown virtually to Rs. 28,000 crores in H1.

- The company added Rs. 5,320 crore deposits last quarter.

- GNPA stood at 117 basis points, and NNPA at 44 basis points.

- Added 1,600 employees sequentially between Q1 and Q2 in the quarter across all the 3 entities, with higher addition in BFSL and in BFL

- BHFL:

- Balance sheet up 42% to just a tad below Rs. 63,000 crore

- Home loans grew 37%, loan against property 37%, lease rental discounting 72% and developer finance 68%.

- Home loan is 60% of the balance sheet, loan against properties 11%, LRD is 15%, DF is 7%, rural is 4%, and others 3%

- The cost of funds came in at 6.63%.

- Capital adequacy at 24.6%.

- Net profit of Rs. 306 crores, a growth of 84%.

- Loan loss and provisions are at 30 crores versus Rs. 61 crores a year ago.

- Management overlay of Rs. 242 crores

- GNPA 24 bps, NNPA 1 bps

Investor Conference Call Highlights

- The total number of users now across the app is 26 million

- 2-wheeler and 3-wheeler businesses are still in a degrowth mode, the management stated that by quarter 4, even that business should be back to growth mode.

- Management stated customer franchises are just a tad below 63 million, on course to get to 68 million, 69 million customers by end of the year.

- The company has added 99 locations, standing at just a tad below 3,700 locations and 143,500 distribution points.

- The management stated between volume and margin, they protect margin.

- The management stated there’s a reasonable chance that the company will exit the year at a deposit book of close to Rs.48,500 crore to 50,000 crores.

- Loan loss and provisions in the last 2 quarters have been between Rs. 725 crores, and Rs. 750 crores. The management expects this number to exit at between Rs. 750 crores to Rs. 825- odd crore on a quarterly run rate basis, between 135 to 145 basis points.

- Web platform, on track for Web=App by March ’23.

- The management stated they will add a total 10-11 million customers this year.

- Last year the company sold 2.23 million various other products, which are non-lending products. This year the run rate is at 1 million in the first half.

- Out of the total 39,423 headcounts, about 9,500 people are in recovery and collection channels.

- The management said earlier they had 4 key lenders/competitors, now there are 16, but Bajaj finance is doing everything to defend its market share and it has done it successfully.

- The management stated next year in addition to the B2B volumes the company move close to around Rs. 50-odd thousand crores of GMV.

- Management guided on the importance of omnipresence; they said in the credit business, cash will remain important, which means branches will remain important. cash and the debt management infrastructure will remain important. They want to take more products to more geography.

- The company has the ambition to have 100 million consumers.

- Out of the new loans booked, 62.3% of the loans have been given to existing customers.

- The management stated the company will see greater momentum in physical infrastructure, over the next 9, to 12 months.

Analyst’s View

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to bounce back quickly from the post-COVID situation and has seen good traction across most categories. The current quarter was good for the company with PAT rising 88% YoY revenue growth of 29% and AUM growth of 31% YoY. The company’s focus on building an omnichannel framework and app ecosystem is the immediate concern as it will also help it harness its potential through digital transformation. The company is also building a technology stack to monetize its strong franchise. The management has also stated that the immediate focus for Bajaj Finance is to scale up its payments and financial services businesses and it is not looking to become a commercial bank for the near future at least. It remains to be seen how the current situation evolves with the several new RBI regulations indicating similar compliances for NBFC & Banks in India and what obstacles will the company face in scaling up its digital payments business. Nonetheless, given the company’s strong market position, the management’s drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Q4 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 7620 | 6010 | 26.8% | 7525 | 1.3% | 27871 | 23546 | 18.4% |

| PBT | 3059 | 1571 | 94.7% | 2610 | 17.2% | 8586 | 5363 | 60.1% |

| PAT | 2268 | 1161 | 95.3% | 1934 | 17.3% | 6350 | 3955 | 60.6% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 8630 | 6855 | 25.9% | 8535 | 1.1% | 31640 | 26683 | 18.6% |

| PBT | 3265 | 1822 | 79.2% | 2868 | 13.8% | 9504 | 5992 | 58.6% |

| PAT | 2419 | 1347 | 79.6% | 2125 | 13.8% | 7028 | 4420 | 59.0% |

Detailed Results:

- The company had an excellent Q4 with consolidated revenue increasing by 25% YoY & PAT growth of 79% YoY due to the low base in Q4FY21.

- Consolidated AUM for the company has risen 26% YoY.

- Quarterly Opex to NII increased from 34.5% to 34.6% YoY while annual Opex to NII increased from 30.7% to 34.6%.

- Net NPA stood at 0.68% Vs 0.75%.

- In Q4, the Company booked 6.28 MM new loans Vs 5.47 MM in Q4 FY21.

- Volume growth in B2B biz was 15% & disbursements grew by 27% in Q4.

- 2.21 MM new customers were added in Q4.

- Deposits book grew by 19% YOY to ₹ 30,800 crore as on 31 March 2022 while their contribution to total borrowings stood at 19%.

- In Q4, loan loss to average receivables was 0.38%

- CAR stood at 27.22%.

- The company declared total dividend of Rs.20 for FY22.

- Customer franchise stood at 57.57 MM as of 31 March 2022 which is a growth of 19% YoY

- Quarterly ROE increased from 3.7% to 5.7% YoY & yearly ROE increased from 12.8% to 17.4%.

- BHFL had a good quarter with AUM growth of 37% to ₹ 53,322 Cr, Net Interest Income growing by 22% YoY to ₹ 452 Cr from ₹ 369 Cr.

- OPEX to NII of BHFL for this quarter increased significantly from 26.6% to 32.5% YoY due to accelerated investments for geographical expansion while GNPA & NNPA stood at 0.31% & 0.14% respectively.

- Capital adequacy of BHFL was 19.72% as of 31 March 2022.

- BFSL had a great quarter adding 62K new customers with margin trading finance book growing to Rs.720 Cr from 184 Cr YoY while total income growing from Rs. 14 Cr to 39 Cr YoY & PAT growing to Rs. 9 Cr from 4.5 Cr.

- The breakup of growth in the consolidated loan book is as follows:

- Auto Finance: -16% YoY

- Sales Finance: 30% YoY

- Consumer B2C: 27% YoY

- Rural Sales Finance: 43% YoY

- Rural B2C: 29% YoY

- SME Lending: 24% YoY

- Securities Lending: 79% YoY

- Commercial Lending: 39% YoY

- Mortgage lending: 24% YoY

Investor Conference Call Highlights:

- In Q4, the Company added 81 new locations making the total Geographic presence at 3,504 locations & 1,33,200 + distribution points as on 31 March 2022.

- In Q4, cost of funds was 6.71% whereas the Liquidity buffer stood at ₹ 10,110 Cr as on 31 March 2022

- The company is comfortable adding 8-9MM new customers in FY23.

- In Q4, the Company added net 2.6 MM users on its digital app platform as against 3.6 MM in Q3 FY22 & plans to add 14-16 MM net new users in FY23.

- The management states that 4th quarter is always important for the company as it determines what will be its entry run rate in the coming fiscal years.

- The management overlay for the current quarter is Rs.1052 Cr and the company plans to decrease this in the next 6 months provided there is no 4th covid wave.

- On 7th April, company infused Rs.2500 Cr in BHFL.

- The company acquired 455,000 new EMI card customers digitally.

- The company’s digital app platform delivered Rs.1,800 Cr of personal loans in the quarter that went by and 29,000 credit cards.

- The management believes that the app is critical for the company to reach 100 million customers someday from the current levels of 4-7 million.

- The management states that it will rather dilute growth than to dilute margin.

- The management believes that NIM is a function of pricing, product mix & cost of funds.

- The company isn’t worried about competition in SME biz due its 14 years of experience in that segment which has taught that new players get attracted seeing the gross margins however they abort the field quickly after showing inability to clock healthy net margins.

- The management expects Opex to NII to remain at 34-35.5% range in FY23.

- The consumer durables lending segment as a % to total balance sheet is 10% currently.

- The company is launching Bajaj Mall on 1st July.

- The company is building the entire technology stack itself so as to monetize its strong franchise.

- The management is focused on developing the company from a financial services business to a payments and financial services business with 100 million franchises in the next five years & thus doesn’t see conversion into a bank as an option for at least the next 3 years.

- The company’s market share in consumer electronics biz is 57-59% & 68-70% in consumer durables biz.

Analyst’s View:

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to bounce back quickly from the post-COVID situation and has seen good traction across most categories. The current quarter was good for the company with PAT rising 80% YoY with revenue growth of 25% and AUM growth of 26% YoY. The company’s focus on building an omnichannel framework and app ecosystem is the immediate concern as it will also help it harness its potential through digital transformation. The app suite is expected to be up and launched by Sep. The company is also building a technology stack to monetize its strong franchise. The management has also stated that the immediate focus for Bajaj Finance is to scale up its payments and financial services businesses and it is not looking to become a commercial bank for the near future at least. It remains to be seen how the current situation evolves with the several new RBI regulations indicating similar compliances for NBFC & Banks in India and what obstacles will the company face in scaling up its digital payments business. Nonetheless, given the company’s strong market position, the management drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Q4 FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 6010 | 6515 | -7.75% | 5848 | 2.77% | 23546 | 23834 | -1.21% |

| PBT | 1572 | 1205 | 30.46% | 1422 | 10.55% | 5363 | 6808 | -21.23% |

| PAT | 1161 | 892 | 30.16% | 1049 | 10.68% | 3956 | 4881 | -18.95% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 6855 | 7231 | -5.20% | 6658 | 2.96% | 26683 | 26385 | 1.13% |

| PBT | 1823 | 1278 | 43% | 1555 | 17.23% | 5992 | 7322 | -18.16% |

| PAT | 1347 | 948 | 42% | 1146 | 17.54% | 4420 | 5264 | -16.03% |

Detailed Results

- The company had a mixed Q4 with consolidated revenue decline of 5% YoY & PAT growth of 42% YoY.

- Consolidated AUM for the company has risen 4% YoY. The Company estimates disbursement levels to go up to 90-105% of Q4FY20 in Q4FY21.

- The Company booked 5.47 MM new loans in Q4 FY21 as against 6.03 MM in Q4 FY20. New loans origination across businesses except auto finance is back to pre-COVID levels.

- The Company acquired 2.26 MM new customers in the current quarter. Total customer franchise stood at 48.57 MM as of 31 Mar 2021, a growth of 14% YoY. The cross-sell franchise stood at 26.89 MM growing 11% YoY.

- Existing customers contributed to 59% of new loans booked during Q4 FY21.

- NII has risen 2% YoY in FY21.

- As of 31st Mar 2021, the Company had a consolidated liquidity buffer of Rs 16,485 Cr representing 12.5% of borrowing.

- Consolidated cost of funds was at 7.39% in Q4 vs 8.37% last year.

- Deposit book stood at Rs 25,803 Cr, a growth of 20% YoY. It accounted for 20% of total assets.

- The Retail: Corporate mix stood at 77:23 in Q4 FY21 as against 67:33 in Q4FY20.

- Opex has risen by Rs 153 Cr YoY. Total Opex to net interest income risen to 34.5% in Q4FY21 vs 31% in Q4FY20.

- Loan losses and provisions for Q4 FY21 was Rs 1,231 Cr. The company has done accelerated write off in the quarter of ₹1,530 crore due to COVID related stress and advancement of its write-off policy. The Company holds management overlay provision of Rs 840 Cr as of 31 Mar 2021 for COVID-19 related stress.

- CRAR remains at 28.34% while Tier-1 capital was at 25.1%.

- GNPA was at 1.79% while NNPA was at 0.75%. The company also maintained a PCR of 58.4%.

- In Q4, urban consumption businesses (B2B) were at 105%, rural consumption business (B2B) at 119%, credit card origination was at 95%, e-commerce was at 84% and auto finance business was at 85% of last year’s volumes.

- The Company is on course to deliver its 3-in-1 financial services for its 48.57 MM customers in a seamless manner by creating an omnichannel framework. It will also implement 3-in-1 financial services through an update in its Experia app.

- The company’s 4 productivity apps- Sales One app, Merchant app, Collections app and Partner app -will go live in a phased manner across businesses between May and September 2021.

- The breakup of growth in the consolidated loan book is as follows:

- Auto Finance: -7% YoY

- Sales Finance: -9% YoY

- Consumer B2C: -3% YoY

- Rural Sales Finance: 8% YoY

- Rural B2C: 11% YoY

- SME Lending: 4% YoY

- Securities Lending: 26% YoY

- Commercial Lending: 29% YoY

- Mortgage lending: 7% YoY

- Bajaj Housing Finance had a good quarter with AUM growth of 19% YoY and a rise in net interest income of 30% YoY. PAT increased 97% YoY. The entity’s Opex to NII improved to 26.6% in Q4FY21 vs 25.4% in Q4FY20.

- Bajaj Financial Securities Ltd (BFinsec) made a net profit of Rs 4.5 Cr on revenues of Rs 17 Cr in Q4 FY21.

- The company announced a dividend of Rs 10 per share in Q4.

Investor Conference Call Highlights

- The company has capped its retail EMI card spend business at 50,000 accounts per month versus 150,000 accounts that they used to do pre-COVID.

- The management states that it expects operating leverage to kick in as AUM starts to grow over the next 2, 3 quarters. Thus, Opex to NII should be back to pre-covid levels then.

- The company already has 7.5 million customers on the Experia app and it expects to have 10 million users at the time of launch.

- The first phase of eStore has gone live in February and it has around 25,000 SKUs currently.

- The onboarding app of Bajaj Financial securities has gone live, and the trading app will go live on the 31st of May.

- The B2B or point of sale business has fully automated underwriting. The B2C business has partial automation where the company decides on loaning money based on data points and analytics.

- Only around 10% of retail customers will be eligible for automatic underwriting. The rest will need a human hand for underwriting.

- As only 10% of customer acquisition will be fully automated, sales through the app through a merchant or others will be integral going forward.

- The company is not looking to compete with other fintechs on new customer acquisition but to build a durable customer franchise and enhance upon it while steadily adding new customers.

- There aren’t any significant switching costs in most products except in mutual funds.

- The company is planning on a small marketing budget of only Rs 40-50 Cr as it aims to drive customer acquisition through greater engagement at the point of sale.

- The management has planned for credit costs of 150-170 bps, given there isn’t any instance of full lockdown and the 3-4 large GDP states do not shut down together.

- The total write-off in Q4 was around Rs 2000 Cr with Rs 1500 Cr being COVID-related and the rest is normal.

- The management remains committed to maintaining the long-term guidance metrics of 25-27% balance sheet growth and 18-20% ROE. It states that the business should see the optimization payout once the apps are fully operational by Sep.

- The management states that except for the B2C business, all of the others have momentum going for them.

- The cost to NII ratio excluding the digital transformation costs would be 31.5%.

- The company is looking to originate almost 2 million customers per quarter.

Analyst’s View

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to bounce back quickly from the post-COVID situation and has seen good traction across most categories. The current quarter was good for the company with PAT rising 42% YoY despite revenues and AUM growth flat YoY. The company’s focus on building an omnichannel framework and app ecosystem is the immediate concern as it will also help it harness its potential through digital transformation. The app suite should be up and launched by Sep. It remains to be seen how the current situation evolves with the 2nd wave of COVID-19 in India and whether the company’s preparations are adequate to weather the incoming uncertainty. Nonetheless, given the company’s strong market position, the management drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Q3 FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 5848 | 6316 | -7.41% | 5787 | 1.05% | 17536 | 17319 | 1.25% |

| PBT | 1422 | 1999 | -28.86% | 1186 | 19.90% | 3791 | 5603 | -32.34% |

| PAT | 1049 | 1488 | -29.50% | 877 | 19.61% | 2795 | 3990 | -29.95% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 6658 | 7024 | -5.21% | 6520 | 2.12% | 19828 | 19155 | 3.51% |

| PBT | 1555 | 2170 | -28.34% | 1305 | 19.16% | 4170 | 6044 | -31.01% |

| PAT | 1146 | 1614 | -29.00% | 965 | 18.76% | 3073 | 4316 | -28.80% |

Detailed Results

- The company had a down Q3 with consolidated revenue decline of 5% YoY. PAT was down 29% YoY in Q3.

- Consolidated AUM for the company has fallen 1% YoY. The Company estimates disbursement levels to go up to 85-100% of FY20.

- Loan disbursement was at 81% of last year’s levels.

- In Q3, urban consumption businesses (B2B) were at 86%, rural consumption business (B2B) at 100%, credit card origination was at 102%, e-commerce was at 107% and auto finance business was at 62% of last year’s volumes.

- The Company acquired 2.19 MM new customers in the current quarter. Total customer franchise stood at 46.31 MM as of 31 Dec 2020, a growth of 15% YoY. The cross-sell franchise stood at 25.25 MM growing 8% YoY.

- Existing customers contributed to 64% of new loans booked during Q3 FY21.

- The company has received RBI approval for the issuance of a co-branded credit card in association with DBS Bank (India) Limited.

- NII was at Rs 4296 Cr vs 4535 Cr last year in Q3. This was mainly caused by interest reversal of Rs 450 Cr versus Rs 83 Cr in Q3 FY20 and cost of surplus liquidity of Rs 213 Cr against Rs 83 Cr in Q3 FY20.

- As of 31st Dec 2020, the Company had a consolidated liquidity buffer of Rs 14,347 Cr representing 11.6% of borrowing.

- Consolidated cost of funds was at 7.78% and is expected to go down to 7.5% by March 2021.

- Deposits book stood at Rs 23,777 Cr, a growth of 18% YoY. It accounted for 19% of total assets.

- The Retail: Corporate mix stood at 76:24 in Q3 FY21 as against 61:39 in Q3FY20.

- Opex declined by 9% YoY. Total Opex to net interest income came down to 32.3% in Q3FY21 vs 33.8% in Q3FY20.

- Loan losses and provisions for Q3 FY21 was Rs 1,352 Cr as against Rs 831 Cr in Q3 FY20. The company also took a one-time principal write-off of Rs 1,970 Cr on account of COVID-19 related stress. The Company holds management overlay provision of Rs 800 Cr as of 31 Dec 2020 for COVID-19 related stress.

- The company has accounted for additional losses on account of COVID-19 in FY22.

- FY22 onwards, the company expects loan losses and provisions to revert to pre-COVID-19 levels of 160-170 bps of average assets.

- The company estimates residual credit costs in Q4 at Rs 1,200-1,250 Cr bringing the total credit cost in FY21 to Rs 5,925-5,975 Cr.

- Consolidated PBT for Q3 contracted by 28% YoY due to increase in loan loss provisions by Rs 520 Cr, interest reversals by Rs 367 Cr, and cost of additional liquidity by Rs 130 Cr vs Q3 last year.

- CRAR remains at 28.18% while Tier-1 capital was at 24.73%. The Company has adequate capital to meet its next 3 years’ growth aspiration.

- GNPA was at 0.55% while NNPA was at 0.19% according to the Supreme Court directive. The company also maintained a PCR of 65%.

- The breakup of growth in the consolidated loan book is as follows:

- Auto Finance: -4% YoY

- Sales Finance: -27% YoY

- Consumer B2C: -1% YoY

- Rural Sales Finance: -10% YoY

- Rural B2C: 10% YoY

- SME Lending: 1% YoY

- Securities Lending: -22% YoY

- Commercial Lending: 15% YoY

- Mortgage lending: 6% YoY

- Bajaj Housing Finance had a good quarter with AUM growth of 18% YoY and a rise in net interest income of 15% YoY. PAT declined 24% YoY for this subsidiary due to higher provisioning. The entity’s Opex to NII improved to 26.4% in Q3FY21 vs 33.7% in Q3FY20.

- Bajaj Financial Securities Ltd (BFinsec) made a net profit of Rs 0.7 Cr in Q3 FY21.

Investor Conference Call Highlights

- The core AUM growth in Q3 was Rs 8000 Cr which was short of the normal growth rate of Rs 9000-9500 Cr per quarter which is expected to be back by Q4.

- The AUM growth in mortgage space was smaller despite disbursement at 90% of last year’s levels as there was significant portfolio attrition caused by pricing actions by competitors.

- The Pro-forma GNPA and NNPA were at 2.86% and 1.22% respectively. Other auto finance, all other segments are expected to come back to pre-covid NPA levels in Q4.

- The omnichannel framework for the complete online loan generation is expected to be completed by May 2021.

- The company will launch Bajaj Pay for consumers sometime in Q4. It will be providing the Bajaj Pay for its existing network of 103,000 merchants initially and will be aiming to double the volumes in this space in the medium term.

- Within a single app ecosystem, the customer will be able to access 5 proprietary marketplaces that Bajaj Finance is looking to create. These will include the company’s EMI Store, insurance marketplace, broking app, and many other financial services all rolled into a single app ecosystem across electronics, insurance, investments, and health. The EMI store is expected to go live in the next 30 days for existing customers.

- The first phase is expected to be launched in July, the second in August and the third will be done by end of Sep.

- H2 of FY22 is expected to be devoted to focusing on sharpening and refining this new offering.

- The management believes that this new app ecosystem development can act as a watershed moment for the company and take them from 46 million customers today to 75-100 million customers. The prime strategy here will be to enhance customer experience (both pre and post purchase) and reducing operational friction.

- The company is also moving to make 100% of calls by collection agents to be recorded for current level of 35-40%.

- The company is not converting any existing loans to flexi now after Q2. All new flexi loans will be from fresh origination.

- The segment that saw the biggest write-offs was auto finance particularly 3 wheeler finance.

- The company has restarted retail EMI cards focusing on an average ticket size of INR 15,000.

- The company will bring back higher ticket sizes once the Bajaj Pay for merchants is launched.

- The company is also offering retail fixed deposits at 6.6%.

- The management has stated that the bigger impact in the next 2 quarters will come from the productivity apps that the company has created rather than the consumer app.

- The Bajaj Pay app will be using Open loop universal QR infrastructure for customers to use universal QR and UPI infrastructure to allow the customer to use a single interface for credit card, UPI, EMI card, or other payment mechanism depending on the network.

- This pay app will integrate directly into the B2B business.

- The credit card offering with DBS is expected to be launched by July. The management maintains that this development will not cannibalize the tie-up with RBL bank.

Analyst’s View

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to bounce back quickly from the post-COVID situation and has seen good traction across most categories. The current quarter was dull for the company with revenues and AUM growth flat YoY while profits fell due to increased provisions. But the current cautious stance of the company is commendable with it deciding to frontload potential losses and focussing on building an omnichannel framework and app ecosystem with its sights at the next evolutionary phase of commerce in India. It remains to be seen whether there are any further disruptions in place from the evolving situation from COVID-19 in India and whether the company’s worst fears regarding credit losses come to exist. Nonetheless, given the company’s strong market position, the management drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Q2 FY21 Updates

Financial Results & Highlights

|

||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 6523 | 6323 | 3.16% | 6650 | -1.91% | 13173 | 12131 | 8.59% |

| PBT | 1305 | 2022 | -35.46% | 1310 | -0.38% | 2615 | 3874 | -32.50% |

| PAT | 965 | 1506 | -35.92% | 962 | 0.31% | 1927 | 2702 | -28.68% |

Detailed Results

- The company had a flat Q2 with consolidated revenue growth of 3% YoY. PAT was down 36% YoY in Q2.

- The company has made an extra contingent expected loss provision of Rs 1450 Cr on account of COVID-19. This brings the total provisioning up to Rs 2350 Cr.

- Consolidated AUM for the company has grown 1% YoY. The Company estimates AUM growth for FY21 at 6-7%.

- The Company booked 3.62 MM new loans during Q2 FY21 as against 6.47 MM in Q2 FY20.

- In Sep ’20, urban consumption businesses (B2B) were at 72%, rural consumption business (B2B) at 91%, credit card origination was at 73%, e-commerce was at 75% and auto finance business was at 54% of last year’s volumes.

- In Sep ’20, total loan disbursements were at 62% of last year’s volumes.

- The Company acquired 1.22 MM new customers in the current quarter. Total customer franchise stood at 44.11 MM as of 30 September 2020, a growth of 14% YoY. The cross-sell franchise stood at 23.87 MM.

- Existing customers contributed to 66% of new loans booked during Q2 FY21.

- In Q2 FY21, the Company has converted ₹1,750 crores of term loans into Flexi loans to provide customers the flexibility of lower repayment and higher prepayment.

- As of 20 October 2020, the Company had a consolidated liquidity buffer of ₹24,775 Cr and SLR investments of Rs. 2,582 Cr.

- Deposits book stood at ₹21,669 Cr, a growth of 23% YoY. It accounted for 17% of total assets.

- The Retail: Corporate mix stood at 75: 25 in Q2 FY21 as against 56: 44 in Q2FY20.

- NII grew by 4% but opex declined by 16%. Total Opex to net interest income came down to 27.8% in Q2FY21 vs 34.6% in Q2FY20.

- During the quarter, the Company has further increased its provisioning coverage for stage 1 and 2 assets by ₹1,370 Cr taking it to ₹5,099 Cr as of 30 September 2020.

- Against 15.7% of the moratorium book in June 2020, stage 2 (1 and 2 installments overdue) book as of 30 September 2020 stood at 8.0% versus 2.3% in Q2FY20.

- The Company has taken a loan loss provision of ₹3,386 Cr against its credit cost estimate of ₹6,000-6,300 Cr for FY21.

- Consolidated PBT for Q2 contracted by 35% YoY due to additional provisions of Rs 1370 Cr.

- CRAR remains at 26.6% while Tier-1 capital was at 23%.

- GNPA was at 1.03% while NNPA was at 0.37%. The company also maintained a PCR of 64%.

- The breakup of growth in the consolidated loan book is as follows:

- Auto Finance: 7% YoY

- Sales Finance: -42% YoY

- Consumer B2C: 5% YoY

- Rural Sales Finance: -19% YoY

- Rural B2C: 15% YoY

- SME Lending: 2% YoY

- Securities Lending: -26% YoY

- Commercial Lending: 5% YoY

- Mortgage lending: 14% YoY

- Bajaj Housing Finance had a mixed quarter with AUM growth of 30% YoY and a decline in net interest income of 6% YoY. PAT declined 36% YoY for this subsidiary. The entity’s Opex to NII improved to 28.2% in Q2FY21 vs 33.3% in Q2FY20.

- Bajaj Financial Securities Ltd (BFinsec) made a net profit of ₹2 Cr in Q2 FY21.

Investor Conference Call Highlights

- Opex for Q2 was down Rs 224 Cr out of which Rs 120 Cr is permanent cost reduction.

- The management wants to act cautiously in current times and is willing to front-load losses and backload income so that once normalcy comes back, the company will have additional momentum to grow.

- Around 70% of the total OEM subvention share used to be Bajaj Finance. This number has gone down to 60-63% but is expected to rise back to previous levels in the near future.

- The company is focussing on a primary transformation and has created a frame called 3-in-1 where fundamentally in 3 clicks, a customer should be able to do away with financial service products across loan, insurance, mutual fund, cards, etc.

- Total outstanding Flexi loans is around Rs 43,000 Cr. This is across mortgages to personal loans to gold loans, each part of the company portfolio is covered in this figure. Flexi loans are offered only in B2C loans.

- BHFL is focused on going back to pre-COVID growth levels by March-April 2021. It currently relies entirely on bank funding and once it completes 3 years of existence, it will have access to money market funding which should aid the entity in its growth quest.

- The management expects Opex to NII to go above 30% for the rest of the year ahead but overall Opex to NII for FY21 should remain below 30%.

- The company is still waiting for clarification from the Govt of India on the issue of interest on interest and how to handle it going forward.

- The company aims to become among the top 3,4 in the country in the credit card business. It already has a strategic and important partnership with RBL and may require an additional such partnership to attain its goals.

- The situation in 2 wheeler and 3 wheeler loans is very different as 3 wheelers customers will only see demand coming back once point-to-point transport necessity comes back. Till then, the company has no option but to provide restructuring options to those customers.

- The cross-sell opportunity for the 23 million is available for card business, mortgage business, personal loan business, insurance business, all businesses. It is harder to estimate the opportunity for just a few segments alone.

- Out of the 23 million, the company is ready to give personal loans to 11.2 million.

- The management firmly believes that as the franchise grows, e-commerce will also grow along with it.

- On a rolling basis, annually, 10% of eligible customers land up taking personal loans. This number is expected to multiply as 3-in-1 financial services come into place.

- The management states that fresh customers default at a much lower rate as they mature into the cycle, depending on what type of loan their bounce rate increases.

Analyst’s View

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to bounce back quickly from the post-COVID situation and has seen good traction across most categories. The company has done well to convert many of its term loans to Flexi loans, increasing customer convenience, and earning fee income along the way. It has also remained conservative by taking the decision to front-load losses and backload income. It remains to be seen whether there are any further disruptions in place from the evolving situation from COVID-19 in India and how it will impact the company’s operations. Nonetheless, given the company’s strong market position, the management drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Q1 FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 5901 | 5302 | 11.30% | 6511 | -9.37% |

| PBT | 1184 | 1744 | -32.11% | 1205 | -1.74% |

| PAT | 870 | 1125 | -22.67% | 892 | -2.47% |

| Consolidated Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 6650 | 5808 | 14.50% | 7231 | -8.03% |

| PBT | 1310 | 1851 | -29.23% | 1278 | 2.50% |

| PAT | 962 | 1195 | -19.50% | 948 | 1.48% |

Detailed Results

-

- The company had stable Q1 with consolidated revenue growth of 14.5% YoY. PAT was down 19.5% YoY in Q1.

- The company has made an extra contingent expected loss provision of Rs 1450 Cr on account of COVID-19. This brings the total provisioning up to Rs 2350 Cr.

- Consolidated AUM for the company has grown 7% YoY due to the lockdown which was in effect till 10th Currently around 86 locations remain closed for the company which accounts for 15% of the business.

- The company expects 75+ cities should revert to pre-COVID volumes by October, 40-75 Cities by end November, 10-40 cities by January, and the top 10 cities by March. Based on this assessment, the company estimates the AUM growth of 10-12% in FY21.

- In Q1, the company switched Rs 8600 Cr of term loans to Flexi loans for some of its customers with no overdue and good repayment track record.

- The company acquired 0.53 million new customers in Q1 showcasing a YoY growth of 16%.

- CRAR was at 26.4% with Tier-I capital at 22.6%.

- The company’s surplus liquidity as of 20th July 2020 was at Rs 20,590 Cr.

- Deposits book rose 33% YoY to Rs 20061 Cr. The retail to corporate mix stands at 70:30.

- Net interest income for Q4 was up 38% YoY to Rs 4684 Cr. The same figure rose 42% YoY for FY20.

- Total Opex to net interest income came down to 27.9% in Q1FY21 vs 35% in Q1FY20. Total Opex fell 11% YoY and 20% QoQ.

- Consolidated moratorium book was reduced to Rs 21705 Cr (15.7%) on 30th June 2020 from Rs 38599 Cr (27%) on 30th April 2020 due to a reduction in bounce rate coupled with improved collection efficiencies.

- GNPA was at 1.4% while NNPA was at 0.5%. The company also maintained a PCR of 65%.

- The breakup of growth in consolidated loan book is as follows:

- Auto Finance: 17% YoY

- Sales Finance: -34% YoY

- Consumer B2C: 17% YoY

- Rural Lending: 19% YoY

- SME Lending: 12% YoY

- Securities Lending: -56% YoY

- Commercial Lending: 3% YoY

- Mortgage lending: 23% YoY

- Bajaj Housing Finance had a good quarter with AUM growth of 52% YoY and growth in net interest income of 23% YoY. PAT growth for this subsidiary was at 31% YoY. The entity’s Opex to NII improved to 30.4% in Q1FY21 vs 41.4% in Q1FY20.

Investor Conference Call Highlights

- S&P Global downgraded the company’s long-term issuer rating on account of a sectoral downgrade due to COVID-19.

- The company has decided to reverse interest income of Rs 220 Cr on the ongoing moratorium book.

- The company got Rs 147 Cr from fee income from conversion to Flexi loans mentioned above.

- Keeping in mind that the ongoing pandemic is one that no one has seen before, the management wants to stay conservative in its stance and thus the company has decided to account for greater provision than required.

- The conversion to Flexi loans was not to mitigate the impact of the moratorium as around Rs 500 Cr of conversions were from loans that didn’t go to the moratorium. The management states that the conversion option was given mainly to keeping customer convenience in mind.

- The gold loan business is operating in 400 cities and is aggregating Rs 70 to 80 Cr of assets per month.

- The company has added 1500 new collection officers to its force.

- The company has kept provisioning on the moratorium AUM in auto finance book at 11.8% vs an average of 14% across other divisions. This is mainly because the company expects higher residual value due to BSVI conversion resulting in prices going up for second-hand assets.

- The management has clarified that the amount of Rs 21700 Cr of loans that are under a moratorium for June have not paid their EMIs for June. The rest of the customers have all paid up.

Analyst’s View

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to bounce back quickly from in the post-COVID situation and has seen good traction across most categories. The company has done well to convert many of its term loans to Flexi loans, increasing customer convenience, and earning fee income along the way. It has also remained conservative by increasing its COVID provisioning to Rs 2350 Cr. It remains to be seen whether there are any further disruptions in place from the evolving situation from COVID-19 in India and how it will impact the company’s operations. Nonetheless, given the company’s strong market position, the management drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Q4 2020 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 6511 | 4879 | 33.45% | 6312 | 3.15% | 23823 | 17386 | 37.02% |

| PBT | 1205 | 1726 | -30.19% | 1999 | -39.72% | 6808 | 6035 | 12.81% |

| PAT | 892 | 1114 | -19.93% | 1488 | -40.05% | 4881 | 3890 | 25.48% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY20 | Q4FY19 | YoY % | Q3FY20 | QoQ % | FY20 | FY19 | YoY% | |

| Sales | 7227 | 5294 | 36.51% | 7019 | 2.96% | 26374 | 18487 | 42.66% |

| PBT | 1278 | 1812 | -29.47% | 2170 | -41.11% | 7322 | 6179 | 18.50% |

| PAT | 948 | 1176 | -19.39% | 1614 | -41.26% | 5264 | 3995 | 31.76% |

Detailed Results

-

- The company had a good Q4 with consolidated revenue growth of 36.5% YoY. PAT was down 19% YoY in Q4 mainly on account of extra provision of Rs 900 Cr for COVID-19. Adjusting for this provision, PAT growth for Q4 would be up 38% YoY.

- FY20 was a good year for the company with revenue growth of 43% YoY and PAT growth of almost 32% YoY.

- Consolidated AUM for the company has grown 27% YoY. Without the 10 days of inactivity in Q4 due to lockdown, AUM growth would have been around 31% YoY.

- CRAR was at 25% which is amongst the highest in NBFCs in India.

- The company’s surplus liquidity as of 15th May 2020 was at Rs 20,900 Cr.

- New loans booked in Q4 rose 3% YoY only due to low acquisition in the last 10 days due to lockdown.

- Net interest income for Q4 was up 38% YoY to Rs 4684 Cr. The same figure rose 42% YoY for FY20.

- Total Opex to net interest income came down to 31% in Q4FY20 vs 34.4% in Q4FY19. The same figure was at 33.5% for FY20 vs 35.3% for FY19.

- GNPA was at 1.61% while NNPA was at 0.65%. The company also maintained a PCR of 60%.

- The company gave out an interim dividend of Rs 10 per share in February.

- The breakup of growth in consolidated loan book is as follows:

- Consumer B2B: 17% YoY

- Consumer B2C: 36% YoY

- Rural Lending: 44% YoY

- SME Lending: 23% YoY

- Commercial Lending: -7% YoY

- Mortgage lending: 36% YoY

- The deposits book saw a growth of 62% YoY in FY20.

- In the standalone business, AUM grew 18% YoY while net interest income for FY20 grew 39% YoY.

- Bajaj Housing Finance had a stellar year with AUM growth of 86% YoY and growth in net interest income of 119% YoY. PAT growth for this subsidiary was at 283% YoY. The entity maintained a CAR of 25.15%.

- The company is said to have tightened underwriting and LTV norms across all businesses till July.

- The company has resumed B2B lending in green and orange zones and has refrained from lending in any other category until the lockdown is lifted.

- B2B in rural has also been opened. Rural B2c is expected to be opened soon.

- The mix of retail to corporate in the company’s deposit book is 67:33. The company has reduced its retail deposit rate by 25 bps in May.

- The total provisioning in Q4 was at Rs 1419 Cr out of which Rs 129 Cr was for recalibration of ECL model, Rs 900 Cr for effects of COVID on overall business and Rs 390 Cr for 2 large identified stressed accounts.

- The company has offered moratorium to all of its non-NPA customers and has taken the decision of not providing moratorium to any customers that are more than 60 days overdue.

- ROA for Q4 was at 0.7% while ROE was at 2.9%. removing the impact of COVID provision, ROA and ROE would be 1.2% and 5% respectively.

- The company added 213 new locations in Q4 bringing its total up to 2392.

- The book value of the company share was at Rs 538 per share.

Investor Conference Call Highlights

- The company has frozen all hires until September 2020. The management has instituted measures to reduce fixed Opex by 22-24% in the last 3 months. This also includes a freeze in branch expansion.

- The management has stated that although growth is a primary focus for the company, it will not be hastily chasing growth even in tough conditions like at present. Instead, it will try and stay prudent and get ready to resume its high growth trajectory as soon as possible.

- The management has stated that although some amount of recovery can be expected from the stressed assets of ILFS and Karvy, the company has decided to write it off so that there isn’t much uncertainty arising from these accounts. Furthermore, whatever recovery comes from these accounts, it can be used to boost COVID provisions or even add on profits at a later date.

- The management has clarified that the company will indeed roll out its systematic deposit plan product on 1st It was supposed to be released earlier but got delayed due to the lockdown.

- The company has indeed formed various scenarios for estimating the impact on credit costs from COVID-19 and these scenarios are not fixed and are dependent on various factors like whether RBI extends the loan moratorium (which it did a week after this call was done). Thus the management has refrained from providing any specific guidance on how it expects credit costs to go in the future.

- The management has stated that there should no impact on the company’s books due to the suspension of the IBC process as the company does not have any clients under this.

- The management has stated that the company should be able to ensure robust fee income by utilizing cross-sell opportunities or by creating new products through data mining. The company has in fact developed its etch infrastructure to be able to allow for multi-card infrastructure so that it can facilitate different cards for different cards to be used for different purposes for the same customer. Although this has not been fully developed yet, there remains significant room for growth for the company using this mechanism.

- The management has stated that it is not correct to compare repayment behaviour for banks and non-banks as the customer set, behavioural characteristics, and nature of these repayments may not be comparable. Furthermore, these data vary a lot across all the players in the banking industry so it cannot be used as representative for such comparisons.

- The management has stated that it will not comment on behavioural change from COVID-19 as it is still too early to gauge customer preferences when the lockdown has not been fully lifted yet and things have not come to normalcy.

- The management has stated that it will not be focussing on disbursement growth right now. The fundamental focus for the company will be how to reopen its entire branch network properly and bring back business to the pre-COVID level safely while managing the risks arising from the new business and economic environment.

- The management reiterates that the primary focus areas for the company immediately post COVID will be managing the Balance Sheet, preserving capital, managing Opex and boosting collections. As long as the company can stay resilient in tough times, it can resume its growth momentum once things come back to normal.

- In the auto finance business, PCR is at 54%. The management made the decision to write off NPAs directly instead or carrying it on the books in 2 and 3 wheeler segment because there are higher delinquencies in this segment. Thus PCR comes down automatically.

- The cost of funds for the company in Q4 was at 8.76% with liquidity drag.

- The company already has a proprietary structure where the company works with an agency and fully outsources the collection operations. Under this structure, the company has a bottom-up structure where the division of collection codes in each geography depends on the characteristics of that particular area. For example, Mumbai has more than 48 different codes which is greater than the number pf pin codes in the city. This model has worked well for the company and the company will build and enhance it further going forward.

- The company’s current CP book is less than Rs 2000 Cr. This represents an opportunity for the company to reduce the cost of funds by raising more funds through the short term CP route.

- The ECB borrowing issued by the company in April was for $75 million at a rate of 7.2%. It is a 3-year program that is fully hedged for both principal and interest.

- The management has stated that the company has provided adequate support for its collection agencies so that staffing requirements remain adequate and things can bounce back fast once the economy opens up again.

- The interest rate charged during the moratorium will be the same as specified in the customer statement.

Analyst’s View

Bajaj Finance is one of the fastest-growing NBFCs in India today. The company has done well to maintain its status as a growth company and has had a stellar year in FY20. But the economic shock and disruption from COVID-19 have forced the company to alter its path and focus on the balance sheet resilience and managing Opex while the economic environment remains tough. The company has indeed been agile and decisive to take quick decisions as to which businesses to open and which to keep on hold in the current environment. It remains to be seen what second-order effects will the COVID-19 disruption have on the NBFC space and how Bajaj Finance navigates through the trying times ahead. Nonetheless, given the company’s strong market position, the management drive to derive new opportunities through the use of data and technology, and its strong balance sheet position, Bajaj Finance remains a pivotal NBFC stock for all Indian investors.

Disclaimer

This is not a piece of investment advice. Please read our terms and conditions.