About the Company

Ashiana Housing Ltd. (AHL) is an Indian real estate development company established in 1986 with its head office in New Delhi, India. It is a real estate company recognized by Forbes as Asia’s 200 Best Under A Billion (2010 and 2011) Ashiana Housing is a mid-income housing developer with a primary focus on Kid Centric Homes, Senior Living, Care Homes (i.e. assisted living) and also comfort homes.

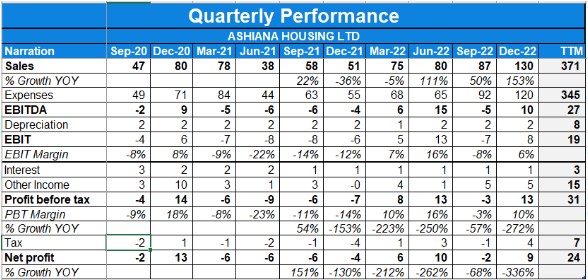

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results

Quarterly results-

- Value of Area Booked recorded at INR 435.82 Crores (Q4FY23) vs 485.29 Crores (Q3FY23).

- Area booked was 8.59 Lakh Sq Ft in Q4 FY23 vs 9.03Lakhs Sq. ft in Q3FY23

- Area constructed was 5.08 lakhs sq ft in Q4FY23 vs 3.42 lakh Sq. ft. (Q3FY23) and 5.07 lakh Sq. ft. (Q4FY22).

- EAC was 5.08 Lakh Sq Ft in Q4 FY23 vs 3.42 lakhs Sqft in Q3 FY23

- Total Revenue reported at INR 116.94 Crs (Q4FY23) vis a vis INR 135.31 Crs in Q3FY23.

- PAT increased to INR 10.38 Crores in Q4FY23 from INR 9.05 Crores in Q3FY23.

- TCI also improved to INR 10.51 Crores in Q4FY23 from INR 9.29 Crores in Q3FY23 .Sales Value for FY23 was INR 1313.43 Crores vs INR 573.25 Crores for FY22, YoY increase of 129%.

Annual results-

- Booking increased by 75% from 14.76 Lakhs Sq. ft. (FY22) to 25.86 Lakhs Sq. ft. (FY23).

- Sales Price improved to INR 5,080 psf (FY23) vs 3,883 psf (FY22), an increase of 31% YoY, driven by increasing prices acrossprojects and changing mix towards higher priced projects.

- Equivalent Area constructed(EAC) for the year was 16.73 Lakhs Sq. ft. (FY23) vs 16.20 Lakhs Sq. ft. (FY22).

- Pre-tax operating cash flows was positive at INR 84.84 Crores (FY23) vs positive at INR 165.05 Crores (FY22).

- Total Revenue increased to INR 425.19 Crores (FY23) vs INR 233.59 Crores (FY22), YoY increase of 82%.

- Total Comprehensive Income positive at INR 28.78 Crores (FY23) vs. negative INR 6.56 Crores (FY22) .

Investor Conference Call Highlights

- The company launched five new projects in the last year, totaling 29.46 lakh square feet.

- The company handed over 10.51 lakh square feet in FY 23, compared to 8.86 lakh square feet in FY 22.

- The company acquired new land parcels in Jaipur, with a potential saleable area of 6.5 lakh square feet and 4 lakh square feet, and in Manesar, Gurugram, with an approximate saleable area of 10.3 lakh square feet.

- The company is expecting sales value of INR 1,500 crores for FY 24.

- The gross margins on new projects are expected to be around 30%.

- Most projects are priced in the range of INR 4,000 to INR 6,000 per square foot.

- Some projects, like Jodhpur and Bhiwadi general housing, are priced below INR 4,000 per square foot.

- Bhiwadi senior living is priced around INR 4,500 per square foot, while Pune and senior living in other locations are priced above INR 5,000 and INR 6,000 per square foot.

- The lack of supply in Gurgaon has contributed to price increases in the market.

- Prices across different geographies, including Jaipur and Bhiwadi, range between INR 4,000 to INR 6,000 per square foot.

- Land prices have increased due to demand for plotted developments, and this has impacted overall pricing.

- The company expects a wider price bracket in the future, with different projects and locations influencing the price points.

- The target gross profit margin is 30%, with sales and marketing expenses around 4% to 4.5% of revenue.

- The company aims for a PAT margin of 13% to 15% after accounting for taxes and other costs.

- The current land bank potential is estimated at around INR 5,500 crores in sales value.

- The company is considering a buyback but hasn’t made any firm decisions yet.

- The hotel investment is generating around 15% returns on invested capital.

- The company is disposing of other assets to optimize capital allocation.

- The pre-launch process has been activated for a project in Bhiwadi, which is located in the industrial area of Bhiwadi.

- The company stated that the EBITDA margins have been low due to depressed volumes and higher operational costs compared to sales prices.

- The company is targeting INR 1,500 crores worth of area booked in FY ’24, with realizations between INR 5,000 crores and INR 5,500 crores.

- Land prices have increased by around double since FY ’20, and sale prices have increased by 20% on the base but up to 40-50% in some places.

- The company aims to increase the scale of the company to about twice its current size within a five-year timeframe.

- Builders plan to address affordability concerns by reducing flat sizes.

Analyst’s Views

Ashiana Housing is a unique presence in the Indian real estate industry. The company has seen a decent year with an increase in revenue of 182%. The company is investing heavily for the purpose of exapansion by launching new projects. It remains to be seen how long will it take for the company to recover and come back to pre-covid levels of performance, and handle the cyclicality and impact of the rising inflation on the real estate sector and Ashiana. Nonetheless, Given the unique and cautious business model of Ashiana and the rising trend of senior living in India coupled with a strong project launch pipeline, Ashiana is a good real estate sector stock to keep in one’s watchlist.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results

- Booking stood at 9.03 lakhs sq. ft Vs 4.9 Lakhs QoQ.

- The value of the Area Booked was recorded at Rs. 485.29 Crores (Q3FY23) vs Rs. 240.19 Crores (Q3FY22).

- The average realization price improved to ₹ 5,373 per sq. ft. in Q3 FY ’23 vis-a-vis ₹ 4,904 per sq. ft. in Q2 FY ’23.

- The area delivered stood at 3.6 Lkh sq. ft.

- The area constructed stood at 3.42 Lakh sq. ft Vs 4.38 Lakh sq. ft QoQ.

- Sales and Other income increased to Rs.135 Crores in Q3FY23 Vs Rs. 91 Crores in Q2FY23.

- PAT has recorded at Rs. 9.29 Crs for Q2FY23 Vs Rs. (1.31) Crores in Q2FY23.

- Pre-Tax Operating Cash Flow was at Rs. 35.6 Crs for Q3FY23 vs negative Rs. 1.05 Crs for Q2FY23

Investor Conference Call Highlights

- The Deliveries commenced in Daksh with 2.99 lakhs sq. ft. delivered in Phase 1.

- The company’s current trajectory indicates the construction of 20 – 25 lakhs sq. ft. zone annually from next year onwards.

- The construction volumes for the current quarter were lower owing to the ban in NCR for construction, delays in the launch of projects coupled with challenges on construction manpower and supply chain.

- The company’s two big project launches for Q4 are Ashiana Ekansh in Jaipur and Ashiana Prakriti in Jamshedpur.

- The company has 5 projects planned for the coming year which include two in Jaipur, one for Senior Living in Chennai, one at Mahindra World City, and another at Nemili. And another, namely, Ashiana Amodh in Pune, is also a Senior Living project.

- The company is seeing the price of land correcting especially in the Gurugram region.

- The company’s expected launch is 1 million sq. feet for Q4 & 3 million for Fy24.

- The company’s current land inventory is sufficient for the coming 3-4 years, however, it will keep bidding conservatively for future growth.

- The project Ashiana Advik in senior living which was newly launched has been launched at a higher price than Ashiana Nirmay leading to a realization bump of 7-8% coupled with a higher contribution from Gurugram.

- Even though the management is relatively pleased with Ashiana Malhar’s performance in Pune, it believes Ashiana Amodh (senior living project) will leave a much greater dent in the Pune market in the coming period.

- The key project on which deliveries happened in this quarter was Ashiana Daksh.

- The company expects to clock a blended GPM of 30% in the coming 2-3 years.

- Since the company missed out on a few deliveries, the ROE would still be in the high single digits for FY24.

- The company appreciates that it operates in a cyclical biz, but due to expanding of senior living & success in projects in Gurugram & Rajasthan, the company is confident of delivering 20-25% growth in pre-sales numbers.

- The company’s value of area booked for senior living is expected to grow from current levels of 150 Crores to 300-400 Crs in the coming 3-4 years.

- The senior living biz is less cyclical in terms of operations coupled with having 3-5% higher margins Vs general housing.

Analyst’s Views

Ashiana Housing is a unique presence in the Indian real estate industry. The company has seen a decent recovery with sales growth of 150% YoY. The company launched Ashiana Amarah & received a great response with all the projects getting sold out on day 1 itself & its senior housing projects are also seeing strong traction. It remains to be seen how long will it take for the company to recover and come back to pre-covid levels of performance, and handle the cyclicality and impact of the rising inflation on the real estate sector and Ashiana. Nonetheless, Given the unique and cautious business model of Ashiana and the rising trend of senior living in India coupled with a strong project launch pipeline, Ashiana is a good real estate sector stock to keep in one’s watchlist.

Q2 FY23 Updates

Financial Results & Highlights

Detailed Results

- Booking stood at 4.9 lakhs Sq. ft Vs 3.34 Lakhs QoQ.

- Value of Area Booked recorded at Rs. 240.19 Crores (Q2FY23) vs Rs. 152.14 Crores (Q1FY23)

- Area constructed stood at 4.38 Lakh sq. ft Vs 3.85 Lakh sq.ft QoQ.

- Sales and Other income increased to Rs.91.72 Crores in Q2FY23 Vs Rs. 81.2Crores in Q1FY23.

- PAT was recorded at negative Rs. 1.81 Crs for Q2FY23 Vs Rs. 10.3 Crores inQ1FY23.

- Pre-Tax Operating Cash Flow was at negative Rs. 1.05 Crs for Q2FY23 vs positive Rs. 27.72 Crs for Q1FY23

Investor Conference Call Highlights

- The company launched its first premium house project in Pune named Ashiana Malhar in Marunji and achieved 80 bookings till September 2022.

- Phase 3 of Ashiana Anmol was also launched in the quarter and 106 bookings were achieved in the quarter.

- The value of the area booked went up to Rs.240.19 Crores versus 152.14 Crores in the first quarter.

- The company saw an improvement in realization price at Rs.4,904 per square foot in the second quarter as compared to Rs.4,557 per square foot in the first quarter of FY 2022-23 which was driven by increasing prices across projects and change in mix towards higher price projects.

- The company handed over 2.07 lakh square feet in the second quarter out of which 1.63 lakh square feet were delivered in Shubham Phase 3.

- The management believes that the market in Gurgaon should remain good for a while.

- The response to the Pune project is not as good as Gurgaon’s due to high competition.

- The company is looking to launch another 1.5 million square feet in the second half of this financial year.

- The management states that the company is on track to get to Rs.1,100 Crores of area booked this year.

- The management states that except Malhar & Anmol (which are low-margin projects), all the other projects have sufficient margins & prices can be increased in line with an increase in construction costs.

- The company is confident of delivering t Ashiana Sehar and Ashiana Aditya Phase 1 in the current financial year.

- The company’s term sheet for developing senior living in Noida fell through because it found the market frothy in terms of land prices and challenging regulatory scenarios.

- The operating cash flow was negative due to collections being offset by high construction costs & marketing spending.

- The company tries to maintain gross margins of 30% in each of its projects.

- The management continues to target a 15% economic ROE.

- The company has a land inventory of 5-7 years if it keeps working at the same pace.

Analyst’s Views

Ashiana Housing is a unique presence in the Indian real estate industry. The company has seen a tepid recovery in Q3 with both sales and profits down YoY. But the projects are going ahead in time and the management expects good response to the upcoming projects in the future. The company has acquired land parcels for development in Chennai and Jamshedpur in Q3 and is looking to develop senior living in Chennai. It remains to be seen how long will it take for the company to recover and come back to precovid levels of performance and what impact will the rising inflation have on the real estate sector and Ashiana. Nonetheless, given the evergreen nature of the real estate industry in India, the unique and cautious business model of Ashiana and the rising trend of senior living in India, Ashiana is a good real estate sector stock with a lot of potential in the future.

Q4 FY22 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 62.8 | 69.7 | -9.9% | 42.8 | 46.7% | 181.9 | 217.1 | -16.2% |

| PBT | 8.8 | -5.7 | 254.4% | -6.1 | 244.3% | -12 | 3 | -500.0% |

| PAT | 9.3 | -5.8 | 260.3% | -3.5 | 365.7% | -5.9 | 3.6 | -263.9% |

| Consolidated Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 78.2 | 81.3 | -3.8% | 54.2 | 44.3% | 233.5 | 259.3 | -9.9% |

| PBT | 7.68 | -6.2 | 223.9% | 7.3 | 5.2% | -14.6 | 0.3 | -4966.7% |

| PAT | 6.3 | -5.6 | 212.5% | -3.8 | 265.8% | -7 | 1.7 | -511.8% |

Detailed Results

-

- Booking stood at 4.53 lakhs Sq. ft Vs 4.21 Lakhs QoQ.

- Area constructed stood at 5.07 Lakh sq. ft Vs 3.73 Lakh sq.ft QoQ.

- Value area Booked Rs.18,557 Vs 16,976 lakhs QoQ.

- The average realization for Q4 stood at Rs/Sq.ft 4093 Vs 4,028.

- Debt/Equity is 0.21.

- Area constructed higher at 16.20 Lakhs Sq. ft. FY22 vs 11.66 Lakhs Sq. ft. FY21.

- New land parcels acquired in the current year in Gurgaon 22.1 acres, Pune 11.93 acres, Jaipur 8.6 acres, Jamshedpur3.96 acres, and two land parcels in Chennai of 15.64 acres and 9.93 acres.

- Total Revenue increased to Rs.78.28 Crs vs 54.19 Crs QoQ due to higher deliveries.

Investor Conference Call Highlights

- The company’s total potential saleable area in new land parcels will be around 61 lakh square feet.

- The company’s bookings in Q4 were driven by Ashiana Amantaran Phase 3, Nirmay Phase 4, Bhiwadi; Ashiana Anmol Phase 2, Gurgaon, and Ashiana Shubham Phase 4 in Chennai.

- The management states that Sales price improved to Rs.3,883 per square foot in FY 22 versus Rs.3,571 per square foot in FY 21, driven by increasing prices across projects and changing mix towards higher-priced projects.

- The company is planning to add about 25 to 30 lakh square feet in FY23.

- The company expects to cross Rs.1000 Cr sales landmark & Rs.1100 Cr presale landmark in FY23 out of which Gurgaon is expected to make 1/4th contribution.

- The management believes that it will not be able to meet its guidance of 15% ROE in FY22. However, it expects the same to be in double digits.

- The company is expecting margin expansion in the next 3-5 years due to higher contribution from the senior living segment, operating leverage & increase in sales price.

- The management believes the key challenge in sustaining the growth post FY23 would be the availability of land parcels at reasonable rates rather than the availability of capital.

- The company expects to spend Rs.200 Cr on acquisitions.

- The company has filed for RERA for Phase 1 of Ashiana Adwik while Milakpur is currently in a status quo position.

- The management believes that the industry will be able to digest the home loan interest rates up to 8.5%.

Analyst’s Views

Ashiana Housing is a unique presence in the Indian real estate industry. The company saw a revenue decrease of 3% while PAT turned positive YoY. The projects are going ahead in time and the management expects a good response to the upcoming projects in the future. The management expects margin expansion in the future for Ashiana due to the rising share of senior living. It also expects to breach the Rs 1000 Cr sales mark in FY23. It remains to be seen how long will it take for the company to recover and come back to provide levels of performance and what impact will the rising inflation have on the real estate sector and Ashiana. Nonetheless, given the evergreen nature of the real estate industry in India, the unique and cautious business model of Ashiana and the rising trend of senior living in India, Ashiana is a good real estate sector stock with a lot of potential in the future.

Q3 FY22 Updates

Financial Results & Highlights

| Standalone financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 43 | 79 | -45.6% | 48 | -10.4% | 119 | 147 | -19.0% |

| PBT | -3 | 14 | -121.4% | -8 | -62.5% | -16 | 9 | -277.8% |

| PAT | -3.5 | 13 | -126.9% | 6 | -158% | -15 | 9 | -266.7% |

| Consolidated financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 54 | 90 | -40.0% | 61 | -11.5% | 155 | 178 | -12.9% |

| PBT | -7 | 14 | -150.0% | -6 | 16.7% | -22 | 6 | -466.7% |

| PAT | -4 | 13 | -130.8% | -6 | -33.3% | -16 | 7 | -328.6% |

Detailed Results

- Booking stood at 4.21 lakhs Sq. ft Vs 4.51 Lakhs QoQ.

- Area constructed stood at 3.73 Lakh sq. ft Vs 4.5 Lakh sq.ft QoQ.

- Revenue recognized from completed projects stood at Rs.30.9 Cr Vs Rs. 45.6 Cr QoQ.

- Income from partnerships stood at Rs.6.4 Cr vs (0.26) Cr.

- Total PAT improved to loss of Rs 3.28 Cr vs 6.36 Cr last quarter.

- The company acquired new land parcels of 9.93 acres Chennai for senior living project development and 3.96 acres in Jamshedpur.

- Bookings for 9M were at 10.23 lakh Sq Ft.

- New land parcels acquired for Ashiana in the current year were Gurgaon 22.1 acres, Pune 11.93 acres, Jaipur 8.6 acres, Jamshedpur 3.96 acres and two land parcels in Chennai of 15.64 acres and 9.93 acres.

Investor Conference Call Highlights

- The bookings in Q3 were relatively higher due to the launch of Ashiana Nirmay Ph 4, Bhiwadi and higher sales in Dwarka Ph 4, Jodhpur, launched towards the end of Q1.

- The management believes that there is no correlation between regular housing and senior housing as senior housing has lower supply vis-à-vis regular housing leading to the ability to appreciate prices by the company in its projects like Ashiana Nirmay Bhiwadi and Ashiana Shubham, Chennai.

- The management believes to get to about 2.5million to 3 million square feet,they have enough projects now in all micro markets except for Jaipur. In Jaipur they need to sign up two more projects over and above their current run rate and are in talks to get new land parcels however sudden increase in prices have slowed that talks.

- The management states that it enjoys premium brand positioning in areas like Jamshedpur and Jaipur leading to more JV’s thus ensuring lower capex and better margins. Further, Chennai is becoming an interesting play from a Senior Living perspective where the management believes that the company can see margin expansion and a brand premium coming in.

- The company is targeting a return of equity post tax of 15% by FY23 and has reduced its current cost of debt from 12-13% to 10%.

- The company’s borrowing strategy is counter cyclical where it pays off debt during upcycle and becomes more leveraged during down cycle.

- After multiple instances of misappropriation of funds by the company , the management has appointed Grant Thornton for internal audit coupled with developing ERP systems.

- The management states that they will sell the existing inventory in Ashiana town by 18-24 months.

- The company has 1 million square feet of land in Ashiana Tarang and has further purchased land parcels using IFC facilities.

- The management views that good golfer regular housing and Chennai for senior living will be good markets in the future.

- The management states that Lavasa project is not doing well due to city issues, its project in Gurgaon has started to pick up well in the last 12-15 months in terms of sales while its new project Gurgaon Ashiana Amara is expected to be a great success and increase brand image of the company.

- The company expects to sell its 11 million sq feet inventory by next 6 years.

- The company believes it has the construction capability but needs to improve its sales quotient for which they have started with channel partners in different cities like Gurgaon.

- The management expects a bull cycle and believes it will be able to pass input price hikes to customers.

- Fixed costs other than sales and marketing ranges between 65-75 Cr per year.

- The company has gross margins of 28-30% in its older projects and expects them to increase in coming years.

- The company enjoys free cash flows even during years of losses due to revenues being front loaded.

Analyst’s Views

Ashiana Housing is a unique presence in the Indian real estate industry. The company has seen a tepid recovery in Q3 with both sales and profits down YoY. But the projects are going ahead in time and the management expects good response to the upcoming projects in the future. The company has acquired land parcels for development in Chennai and Jamshedpur in Q3 and is looking to develop senior living in Chennai. It remains to be seen how long will it take for the company to recover and come back to precovid levels of performance and what impact will the rising inflation have on the real estate sector and Ashiana. Nonetheless, given the evergreen nature of the real estate industry in India, the unique and cautious business model of Ashiana and the rising trend of senior living in India, Ashiana is a good real estate sector stock with a lot of potential in the future.

Disclaimer

This is not a piece of investment advice. Please read our terms and conditions.