About the Company

Amber Enterprises India is engaged in the business of manufacturing a versatile range of products i.e. Air conditioners, microwave ovens, washing machines, refrigerators, heat exchangers, sheet metal components, etc. Currently, the Company has nine manufacturing facilities in India out of which two manufacturing facilities are operating in a tax exemption zone.

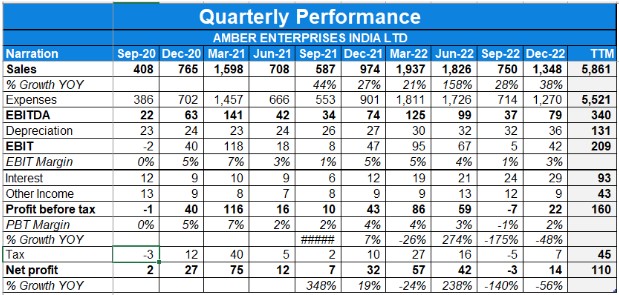

Q4FY23 Updates

Financial Results & Highlights

Detailed Results:

- The sales growth stood at 55% while profits grew by 82% in Q4.

- GPM in Q4 reduced from 13.8% to 13.6% while EBITDA% reduced from 6.9% to 6.8%.

- Finance cost and Depreciation increased to Rs.37 Crs and Rs.39 Crs as compared to Rs.19 Crs and Rs.30 Crs. in Q4FY22, respectively. The increase in Finance cost and Depreciation is largely due to capex incurred during the period and increased interest rates.

- FY23 Revenue & EBITDA growth for respective segments in Q4-

- RAC & Components division – 65% & 60%

- Electronics division – 82% & 95%

- Mobility division- 46% & 47%

- Motor division- 30% & 69%

Investor Conference Call Highlights:

- The management states that Indian RAC market has grown to almost 8.4 million units in FY2022-FY2023.

- Healthy growth is expected in the upcoming years owing to rise in temperatures, boom of residential sector, growing retail and hospitality sector, rising construction activities in the commercial and real estate space along with rampant expansion on SME and commercial hubs.

- The AC industry reached to a market size of 8.4 million in FY2022-FY2023 and with the continuous rising demand for air conditioners, Amber looks forward towards an optimistic and steady growth in coming quarters.

- The management states that this year many brands shifted their strategies to in-source assembly rather than outsourcing. While markets looked at this as a threat, Amber turned it into an opportunity by expanding offerings under the components and subassembly segment.

- Owing to the raise in components and sub-assembly’s businesses, Amber during the year expanded its market share in RAC industry and manufacturing footprint level in value terms to 29.4% in financial year FY2023 vis-a-vis 26.6% in FY2022.

- The company is marching ahead in its export initiatives, and has started getting approvals from its export customers, expecting orders to flow in current financial year FY2023-FY2024.

- The company closed the FY 2023 at a net debt level of Rs.588 crores at consolidated level.

- During FY2023, the company did a capex of 698 Crores at consol. level that helped in increasing the profitability and improving the share of business in RAC segments and other divisions.

- The management states that it is currently witnessing a muted Q1 FY2024 due to unseasonal rain in North India, however it hopeful to consistently grow the bottom line due to product mix change and operational efficiencies.

- The components division has added new customers during FY2023. This division has also realigned its strategy to offer comprehensive solutions in components and subassemblies in tandem with the strategy of RAC customers to insource the assembly businesses.

- On the mobility application division, which includes Sidwal for FY2023, revenue stood at Rs.422 Crores versus Rs.289 Crores in FY2022 marking a growth of 46%.

- The mobility application division is having a strong order book of more than 700 Crores as of today. It commenced production of pantry systems for Vande Bharat Express increasing its wallet share and increasing in existing customers.

- The mobility application division has done transfer of technology agreements in the plug door segments and gangway segment which will help in expanding their wallet share in the existing customers of railways and metros. Defense application for this division is seeing robust growth.

- In the electronic division, the wearable segment has strong growth. The pilot lot of telecom products have also started. It has on boarded new customers in variable and telecom sectors and the room AC PCBA market share has crossed 20% of the complete RAC sector in PCBA.

- The motors division is expanding BLDC Motors now in ODU, WACs and commercial segment of heating, ventilation and air-conditioning. It is at advanced stages to add marquee clients in exports and is also developing motors for newer application other than RAC segment.

- The management explains that the lead time to onboard a customer is quite high in its business. And the company’s Q4 revenues mainly jumped significantly due to new customers that the company was in touch with since two to three years.

- The management is very bullish on the railway and defense sectors, as the Vande Bharat trains that are being launched are completely air-conditioned trains coming in high numbers.

- The management gives guidance for the railway and defense sectors division revenues to double in the next three to four years.

- The company did Rs. 698 crores capex in FY23, and the board has planned a Rs. 350 to 375 crores capex for FY24 which will be largely be spent on the four areas R&D and maintenance capex. It will also be used for expansion of the subsidiary business and in brownfield expansion in the components and sub-assembly segment.

- Despite the unseasonal rains, the management is optimistic that the industry should be in a 10% to 15% range in the financial year end.

- The management recommends investors to not look at the balance sheet in terms of margins and look at absolute EBITDA numbers and levels.

- The management gives a guidance of delivering a 25% to 30% CAGR of absolute EBITDA numbers irrespective of the margins.

- The management states that PICL is the leading company today in the motors front with about close to about 26% to 27% market share on the component side.

- The management states that in sheet metal they are the largest in the country giving solutions in the sheet metal side with about 35% to 40% market share.

- The management states that there have been no price hikes because commodities are stabilized now and everybody has adjusted all the inventories for BEE norms and it has been digested by the market making it a new normal now.

- On PLI, the management comments that it has crossed threshold limits, on the incremental capex which was required and also the incremental sales peaked both the part of the PLI eligibility. They are thus eligible this financial year to receive the first part of the PLI .

Analyst’s View:

Amber Enterprises has a strong operating profile, characterized by its established market position as the leading original design manufacturer of room air conditioners. It had good growth in revenues at 55% while profits grew by 82% in Q4. Its clientele includes several of the leading RAC brands, such as Voltas, Panasonic, Daikin, LG, Godrej, Whirlpool, Samsung, Toshiba, and Bluestar, among others. In addition, over the years Amber has backward integrated into manufacturing key RAC components, which has supported its growth and profitability. Amber received approvals under the Production Linked Incentive (PLI) scheme announced for the AC component sector—Rs. 100 crores for the electronics division in ILJIN Electronics Private Limited and Rs. 300 crores for the AC components division—which is likely to support its growth prospects in the near to medium term. Seeing the developments, growth and order book of the company, Amber Enterprises Ltd is definitely a key stock to keep in the watchlist.

Q3FY23 Updates

Financial Results & Highlights

Detailed Results:

- The sales growth stood at 38% while profits degrew by 56%.

- GPM reduced from 18.3% to 17% while EBITDA% reduced from 7.6% to 6.6%.

- Finance cost and Depreciation increased to Rs.29 Crs and Rs.36 Crs as compared to Rs.12 Crs and Rs.27 Crs. in Q3FY22, respectively. The increase in Finance cost and Depreciation is largely due to capex incurred during the period and increased interest rates.

- 9M revenue & EBITDA growth for respective segments –

- RAC & Components division – 78% & 58%

- Electronics division – 91% & 139%

- Mobility division- 50% & 49%

- Motor division- 30% & 64%

Investor Conference Call Highlights

- AC industry witnessed a change in the manufacturing landscape, wherein some of the big brands shifted their strategy from outsourcing RAC to in-house AC assembly with varied levels of backward integration in order to take benefits from the PLI scheme. This change in the strategy of brands of in-house assembly of AC increased the requirement of components manufacturers, and Amber is one of the most preferred choices as per the management.

- The company’s strategy going forward is to maintain a share of 26% to 28% in the manufacturing footprint of the room AC industry.

- The growth in the RAC division was fueled by a strong order book, new customer addition, and expansion in newer geographies like Chennai, SriCity, and Supa in Pune, and Pantnagar areas.

- Electronics division is expected to grow at 50% in FY24.

- The Commercial production of ILJIN Chennai commenced in December ’22, and is expected to add four new customers in the ILJIN Chennai plant.

- Order book for the mobility segment stands at more than INR 700 crores.

- The motors division is expected to grow at 30-40% in the coming year owing to The strong order book with new product addition and geographical expansion.

- Out of the total sales of the AC division i.e. INR 2,822 crores, INR 1,137 crores is the components share.

- The company’s capex for the financial year will stand at 625-650 Crs.

- The gross margins of the standalone entity reduced owing to the addition of components & assembly biz which has lower margins.

- The electronics biz is expected to grow at a rapid pace due to new customer additions in AC, fans, microwaves, refrigerators, washing machines, hearable and wearable, & 5G equipment.

- The capex guidance for the coming year stands at around 250-275 Crs while the company plans to pay off a debt of around 300-350 Crs by the end of FY23.

- In the 5G equipment segment, the company has started with the equipment such as BBU and RRH, antennas & EO&D devices.

- THe company’s peak revenue capacity will be 5X its gross block.

- ESOP expense in Q3 is INR 7.32 crores.

- The management expects operational leverage since the capacity utilization of new plants is only 25-30% currently.

- The company strives to deliver a range bound of 30% plus absolute EBITDA number going forward.

- The company was not affected by the COVID situation in China because it preplanned its shipment factoring the high probability of a covid wave.

- The management summarized its capital allocation strategy by stating “ largely, whenever we invest even INR 1 invested if any return is coming beyond 4 to 5-year range, we don’t invest”.

- The company is on track to achieve the PLI incentive targets.

Analyst’s View:

Amber Enterprise India Limited’s (AEIL) strong operating profile, characterized by its established market position as the leading original design manufacturer (ODM) of room air conditioners (RACs) and its components in India, integrated operations, and established relationships with reputed players in the RAC industry. The company has ~70% share of the total outsourced RAC manufacturing business in India. Its clientele includes several of the leading RAC brands, such as Voltas, Panasonic, Daikin, LG, Godrej, Whirlpool, Samsung, Toshiba, and Bluestar, among others. In addition, over the years AEIL has backward integrated into manufacturing key RAC components, which has supported its growth and profitability. Further, AEIL was able to convert one of the customers from its refrigerant filling business (following the Government of India’s (GoI’s) ban on importing refrigerant filled ACs in October 2020) into opting for completely built units. The same is likely to provide additional contract manufacturing opportunities to the company over the medium term. AEIL received approvals under the Production Linked Incentive (PLI) scheme announced for the AC component sector—Rs. 100 crores for the electronics division in ILJIN Electronics Private Limited and Rs. 300 crores for the AC components division—which is likely to support its growth prospects in the near to medium term. Seeing the developments, it would be interesting to keep a watch on Amber Enterprises India Limited.

Q2FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1,432 | 574 | 149% | 1,557 | -8% | 3,138 | 2,296 | 36% |

| PBT | 19 | 10 | 90% | 49 | -61% | 70 | 78 | -10% |

| PAT | 13 | 7 | 86% | 32 | -60% | 48 | 52 | -7.69% |

| Consolidated Financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1,826 | 708 | 158% | 1937 | -5.7% | 4,206 | 3,031 | 38% |

| PBT | 59 | 16 | 268% | 86 | -31.39% | 154 | 120 | 28% |

| PAT | 43 | 11 | 283% | 59 | -27.11% | 111 | 83 | 33.73% |

*Contains Gain on disposal of discontinued operations.

Detailed Results:

- On the operating profitability the company has clocked 377 crores in operating EBTDA in trailing 12 months ended on 30th June 2022 versus 326 in FY20.

- In the motors division, motor division has grown by 131% in Q1 FY23 over Q1 FY22.

- In the room AC division, RAC division has grown by 138% in Q1 FY23 over Q1 FY22.

- The mobility application division grew by 91% in Q1 FY23.

- On the revenue Q1 FY23 revenues stood at Rs. 1,826 crores versus 708 crores in Q1 FY22.

- On the PAT Q1 FY23 PAT stood at Rs. 43 crores versus Rs. 11 crores in Q1 FY22.

- On the net working capital days, the company was able to reduce it on a consolidated level from 76 to 37 days in the comparative quarters.

- Gross debt is around 1,300 crores.

Investor Conference Call Highlights

- On the new greenfield facility, SriCity plant will be operational during H2 FY23.

- The quarter continued to bring challenges related to inflation, rising interest rates and foreign exchange fluctuations. With the recent revision in BEE ratings for the AC industry from 1st July 2022, there will be price increases across Air conditioners but with easing of commodity costs, we believe, demand will not be much impacted.

- Management believes demand is returning to normal for Q1FY23, as they were able to surpass the pre-pandemic sales level.

- Company was able to pass on the commodity price increase to our customers with a quarterly lag.

- RAC and Components division is expected to grow faster than the industry growth rate in FY23

- Motors division is expected to grow more than 30% in FY23

- Electronics division is expected to grow more than 35% in FY23

- Mobility Application division is expected to grow more than 15% in FY23

- New Acquisitions: AmberPR and Pravartaka are expanding their manufacturing footprints in western and southern regions respectively and both the companies are expected to grow more than 25% in FY23.

- Management expects ROCE to improve significantly from the current levels and is expected to be in the range of 17%-20% in the next 2-3 years’ time. The expected improvement in ROCE is despite investments in growth capex.

- The quarter however continued to bring challenges related to inflation, rising interest rates and foreign exchange fluctuations. The industry however witnessed some softening of raw material prices but it still continues to be higher than the pre-pandemic levels.

- During the quarter the company was able to pass on the commodity price increase to customers that happens with the quarterly lag as a standard industry phenomenon.

- Company’s market share in value terms at OEM manufacturing level has increased from 21.2% in FY18, the year when it was listed, to 26.6% in FY22.

- On the commercial side, company have added new products for commercial ductable ACs as well as Cassette ACs which they have started to offer to their existing customers now.

- Company’ve added new big customers through brownfield expansion in south India. As informed earlier we have added Boat as a customer and have started supplies for new age applications like smart variables and hearables. This is a large business segment which is growing at a fast pace.

- Company has also won some recycling of air conditioners businesses from Delhi Metro which we have accomplished this quarter.

- Q2 and Q3 are off-season for the room AC sector.

- 400 crores is what management will be investing this financial year, out of which some part is going into a greenfield facility at Sricity which will be getting over right now. Next year management expects it to be in the range of 150 to 175 crores.

- Management has been able to pass on commodity increases on a quarterly lag basis every time.

- Management guided that exports is a long-term strategy. The significant impact of exports should be visible in the balance sheet maybe 3 to 4 years from now.

Analyst’s View:

Amber Enterprise India Limited’s (AEIL) strong operating profile, characterised by its established market position as the leading original design manufacturer (ODM) of room air conditioners (RACs) and its components in India, integrated operations, and established relationships with reputed players in the RAC industry. The company has ~70% share of the total outsourced RAC manufacturing business in India. Its clientele includes several of the leading RAC brands, such as Voltas, Panasonic, Daikin, LG, Godrej, Whirlpool, Samsung, Toshiba and Bluestar, among others. In addition, over the years AEIL has backward integrated into manufacturing key RAC components, which has supported its growth and profitability. Further, AEIL was able to convert one of the customers from its refrigerant filling business (following the Government of India’s (GoI’s) ban on importing refrigerant filled ACs in October 2020) into opting for completely built units. The same is likely to provide additional contract manufacturing opportunities to the company over the medium term. AEIL received approvals under the Production Linked Incentive (PLI) scheme announced for the AC component sector—Rs. 100 crores for the electronics division in ILJIN Electronics Private Limited and Rs. 300 crores for the AC components division—which is likely to support its growth prospects in the near to medium term. Seeing the developments, it would be interesting to keep a watch on Amber Enterprises India Limited.

Q1FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1,432 | 574 | 149% | 1,557 | -8% | 3,138 | 2,296 | 36% |

| PBT | 19 | 10 | 90% | 49 | -61% | 70 | 78 | -10% |

| PAT | 13 | 7 | 86% | 32 | -60% | 48 | 52 | -7.69% |

| Consolidated Financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1,826 | 708 | 158% | 1937 | -5.7% | 4,206 | 3,031 | 38% |

| PBT | 59 | 16 | 268% | 86 | -31.39% | 154 | 120 | 28% |

| PAT | 43 | 11 | 283% | 59 | -27.11% | 111 | 83 | 33.73% |

*Contains Gain on disposal of discontinued operations.

Detailed Results:

- On the operating profitability the company has clocked 377 crores in operating EBTDA in trailing 12 months ended on 30th June 2022 versus 326 in FY20.

- In the motors division, motor division has grown by 131% in Q1 FY23 over Q1 FY22.

- In the room AC division, RAC division has grown by 138% in Q1 FY23 over Q1 FY22.

- The mobility application division grew by 91% in Q1 FY23.

- On the revenue Q1 FY23 revenues stood at Rs. 1,826 crores versus 708 crores in Q1 FY22.

- On the PAT Q1 FY23 PAT stood at Rs. 43 crores versus Rs. 11 crores in Q1 FY22.

- On the net working capital days, the company was able to reduce it on a consolidated level from 76 to 37 days in the comparative quarters.

- Gross debt is around 1,300 crores.

Investor Conference Call Highlights

- On the new greenfield facility, SriCity plant will be operational during H2 FY23.

- The quarter continued to bring challenges related to inflation, rising interest rates and foreign exchange fluctuations. With the recent revision in BEE ratings for the AC industry from 1st July 2022, there will be price increases across Air conditioners but with easing of commodity costs, we believe, demand will not be much impacted.

- Management believes demand is returning to normal for Q1FY23, as they were able to surpass the pre-pandemic sales level.

- Company was able to pass on the commodity price increase to our customers with a quarterly lag.

- RAC and Components division is expected to grow faster than the industry growth rate in FY23

- Motors division is expected to grow more than 30% in FY23

- Electronics division is expected to grow more than 35% in FY23

- Mobility Application division is expected to grow more than 15% in FY23

- New Acquisitions: AmberPR and Pravartaka are expanding their manufacturing footprints in western and southern regions respectively and both the companies are expected to grow more than 25% in FY23.

- Management expects ROCE to improve significantly from the current levels and is expected to be in the range of 17%-20% in the next 2-3 years’ time. The expected improvement in ROCE is despite investments in growth capex.

- The quarter however continued to bring challenges related to inflation, rising interest rates and foreign exchange fluctuations. The industry however witnessed some softening of raw material prices but it still continues to be higher than the pre-pandemic levels.

- During the quarter the company was able to pass on the commodity price increase to customers that happens with the quarterly lag as a standard industry phenomenon.

- Company’s market share in value terms at OEM manufacturing level has increased from 21.2% in FY18, the year when it was listed, to 26.6% in FY22.

- On the commercial side, company have added new products for commercial ductable ACs as well as Cassette ACs which they have started to offer to their existing customers now.

- Company’ve added new big customers through brownfield expansion in south India. As informed earlier we have added Boat as a customer and have started supplies for new age applications like smart variables and hearables. This is a large business segment which is growing at a fast pace.

- Company has also won some recycling of air conditioners businesses from Delhi Metro which we have accomplished this quarter.

- Q2 and Q3 are off-season for the room AC sector.

- 400 crores is what management will be investing this financial year, out of which some part is going into a greenfield facility at Sricity which will be getting over right now. Next year management expects it to be in the range of 150 to 175 crores.

- Management has been able to pass on commodity increases on a quarterly lag basis every time.

- Management guided that exports is a long-term strategy. The significant impact of exports should be visible in the balance sheet maybe 3 to 4 years from now.

Analyst’s View:

Amber Enterprise India Limited’s (AEIL) strong operating profile, characterised by its established market position as the leading original design manufacturer (ODM) of room air conditioners (RACs) and its components in India, integrated operations, and established relationships with reputed players in the RAC industry. The company has ~70% share of the total outsourced RAC manufacturing business in India. Its clientele includes several of the leading RAC brands, such as Voltas, Panasonic, Daikin, LG, Godrej, Whirlpool, Samsung, Toshiba and Bluestar, among others. In addition, over the years AEIL has backward integrated into manufacturing key RAC components, which has supported its growth and profitability. Further, AEIL was able to convert one of the customers from its refrigerant filling business (following the Government of India’s (GoI’s) ban on importing refrigerant filled ACs in October 2020) into opting for completely built units. The same is likely to provide additional contract manufacturing opportunities to the company over the medium term. AEIL received approvals under the Production Linked Incentive (PLI) scheme announced for the AC component sector—Rs. 100 crores for the electronics division in ILJIN Electronics Private Limited and Rs. 300 crores for the AC components division—which is likely to support its growth prospects in the near to medium term. Seeing the developments, it would be interesting to keep a watch on Amber Enterprises India Limited.

Q4FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1565 | 1314 | 19.1% | 670 | 133.6% | 3170 | 2326 | 36.3% |

| PBT | 49 | 94 | -47.9% | 18 | 172.2% | 70 | 77 | -9.1% |

| PAT | 32 | 60 | -46.7% | 14 | 128.6% | 48 | 51 | -5.9% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1946 | 1607 | 21.1% | 983 | 98.0% | 4240 | 3064 | 38.4% |

| PBT | 86 | 116 | -25.9% | 43 | 100.0% | 154 | 120 | 28.3% |

| PAT | 59 | 76 | -22.4% | 33 | 78.8% | 11 | 83 | 33.7% |

Detailed Results:

- The company had a poor quarter with a rise of 21% YoY in consolidated revenues while consolidated profits declined by 22% YoY.

- Operating EBITDA in Q4 for Amber was at Rs 133 Cr with the margin at 6.9%.

- Operating EBITDA in FY22 for Amber was at Rs 296 Cr with the margin at 7%.

- Working capital days for FY22 stood at 39 days Vs 56 days YoY.

- The subsidiary revenues for FY22 were at:

- PICL: Rs.236 Cr

- ILJIN & EVER:: 650 Cr

- Sidwal/ mobility applications: Rs. 289 Cr

- Amber PR : Rs.51 Cr

- Pravartaka : Rs.26 Cr

- The order book for Sidwal stands at more than Rs.600 Cr.

Investor Conference Call Highlights:

- The management states that the company is ready for the new BEE rating revision to be implemented on 1st July 2022.

- FY22 revenues were the highest annual revenues recorded by Amber.

- The company’s contribution value in the RAC sector for both finished goods and components is around 26.5% as of today.

- The company was able to convert a few customers from the first phase of gas filling to offering completely built units CBUs. It also added the entire product lineup of commercial ductable ACs as well as cassette ACs to its portfolio in FY22.

- The company acquired a 60% stake in Pravartaka Tooling Services Private Limited which is engaged in the business of injection mould tool manufacturing and injection moulding components for various applications.

- The management states that due to BEE norm change, the company expects finished goods to get expensive by at least Rs.1000 to Rs.1200 on a model-to-model basis.

- The company’s gross margin decreased to 10.9% due to the company’s practice of passing on commodity cost increases through price hikes with a quarter’s lag & the management expects margins of Q1FY23 to be much better due to the price hike.

- The management expects 100% YoY growth in the value & volume of exports of motor components.

- The company expects to increase its market share by at least 100 bps in the RAC division due to strong growth in its component segment.

- The company will incur CAPEX in the range of Rs.350-400 Cr in FY23.

- The management expects RAC’s contribution to come down to less than 50% in the coming years.

- The company expects the industry to grow by 30% in volumes term in the next FY.

- The company’s geographical mix stood as north @ 35% to 40%, South @ 30% to 32%, and West and East contributing the remaining portion.

- The company expects 3-4% points of benefits in the coming years due to an increase in the capacity of critical components in India, 80-85% of which are currently imported.

- The management states that the contribution from CAC is somewhere to the tune of Rs.20-25 Cr which it expects to go up by around Rs.100 Cr in the next two years.

- The company expects a good festive season due to new policies coming in place from 1st July where brands are pre- cautioning, so the current model is likely to be sold till 15th or 20th June and then from 10th July, they will get into new models because of which demand rather than spreading into the quarter, would go until August and September.

Analyst’s View:

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter was poor with YoY growth in sales while margins collapsed due to input cost inflation. The demand for components is expected to rise significantly with pent up demand coming to the fore this summer. The management remains optimistic about the industry growing at 30% YoY & amber growing at a similar rate. It has stated that Amber stands ready for the new BEE ratings change. It remains to be seen how the industry demand will be affected by rising RM costs and whether the company will be able to achieve its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q3FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 670 | 584 | 14.7% | 353 | 89.8% | 1605 | 1011 | 58.8% |

| PBT | 18 | 27 | -33.3% | -8 | 325.0% | 20 | -17 | 217.6% |

| PAT | 14 | 18 | -22.2% | -6 | 333.3% | 16 | -9 | 277.8% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 982 | 774 | 26.9% | 596 | 64.8% | 2293 | 1457 | 57.4% |

| PBT | 43 | 40 | 7.5% | 9 | 377.8% | 68 | 4 | 1600.0% |

| PAT | 33 | 28 | 17.9% | 8 | 312.5% | 52 | 7 | 642.9% |

Detailed Results:

- The company had a decent quarter with a rise of 27% YoY in consolidated revenues while consolidated profits rose to Rs 43 Cr from a profit of Rs 40 Cr last year.

- On a standalone basis, the decline in profitability is due to commercialization expenditures for three new facilities in Kadi (Gujarat) for injection molding, Chennai (Tamil Nadu) for sheet metal components and heat exchangers, and Supa (Maharashtra) for sheet metal components.

- PAT margins stood at 3.4% in this quarter.

- Operating EBITDA in Q3 for Amber was at Rs 74 Cr with the margin at 7.6%.

- Operating EBITDA in 9M for Amber was at Rs 163 Cr with the margin at 7.2%.

- The consolidated revenue mix was at 39:61 in Q3 for RAC: Components+Mobility respectively.

- The consolidated revenue mix was at 46:54 in 9M for RAC: Components+Mobility respectively.

- The subsidiary revenues for Q3 were at:

- PICL: Rs 80 Cr

- ILJIN: Rs 123 Cr

- EVER: Rs 63 Cr

- Sidwal: Rs 85 Cr

- AmberPr: Rs 12 Cr

- Amber added 1 new customer for EVER and 2 new customers for IL JIN in Q3.

- The order book for Sidwal stands at more than Rs 425 Cr.

- The company invested Rs 73 Lacs to set up Amber Enterprises USA to expand its global presence.

Investor Conference Call Highlights:

- The acquisition of a majority stake in AmberPR Technoplast will help the company in expanding its footprint in the manufacturing of cross-flow fans and other plastic components for a variety of sectors.

- Seeing a surge in demand for air-conditioned coaches and many forthcoming Metro projects around the country, the company has strengthened its product portfolio for Railways, Metros, and Bus Air Conditioning in Sidwal.

- The management states that input costs rose due to high commodity prices and supply chain issues. However, the company has been able to pass on the price hike to the customers & expects to maintain its EBIDTA margins in the future, says the management.

- The company has surpassed pre-pandemic revenue & EBIDTA for the quarter.

- The acquisition of majority ownership in AmberPR Technoplast India Private Limited, erstwhile Pasio India Private Limited is expected to help help the company to grow its component segment, with a greater focus on providing more backward integrated solutions in key components of the RAC segment i.e. cross-flow fan, along with injection molding components for other industries, like refrigeration and automobile segments.

- The company received approval for production of AC components under normal investment category under a threshold incremental investment of Rs.300 Cr while its subsidiary IL JIN electronics received approval for manufacturing of lower value intermediaries of AC under large investment category with a threshold incremental investment of Rs.100 Cr.

- The management expects the motor division & electronics division in PICL to double in revenues.

- In the component division, the company has added new customers like Samsung for sheet metal components and heat exchangers & Voltas Beko for injection molding components for washing machines and refrigerators.

- The company has also started offering a full range of cassette ACs to existing customers.

- Due to the new product additions in the commercial RAC division, the management expects to outnumber the industry in terms of volume.

- The management expects the company to do volumes of close to 3 million units in the AC segment for the current fiscal year.

- The management expects to see good numbers in the coming year due to the import ban leading to Amber receiving a bigger share of brands that were previously importing finished units.

- The management believes the AC demand will hit 7.5-7.8 million units from the current levels of 6.2-6.5 million which would mean surpassing the pre-covid levels. The company expects to outpace the industry growth rate & gain market share like it has done in the past as well.

- The company has introduced cassette AC, which is a new offering & is seeing good traction no one in the industry is offering it today as an ODM solution. However, the management expects the revenue contribution of this segment to be marginal.

- The company will require 1.5-2 years to crack the mass production in export markets like the USA due to the high-reliability cycle.

- The company is expected to generate revenues of Rs.90 Cr from its new acquisition of AmberTechnoplast.

- The management expects to carry out the current Capex through internal accruals & believes that the new product line addition in the component segment (even though it is a low margin business) will help in improving asset utilization.

- New ratings, new model lineups, and conversations with the customers for a long time helped the company to completely pass on the commodity price hike impact.

- Due to make in India, PLI initiatives, work from home culture, wide product line & company’s new entrance in Southern market, the management is confident of doubling the revenues in the next 3 years.

- The management is aiming for 25% EBIDTA growth in the next 3 years.

- The company believes that it is competitive with China when it comes to exports of components. However, it lags when it comes to the finished goods side.

- The company is focusing on increasing its wallet share & improving asset utilization by increasing component segments’ revenue rather than investing in ODM and finished goods as they require large capex.

- The management is envisaging a CapEx of around 375 crores on a consolidated basis and in the next financial year, a CapEx of somewhere around 250 crores to 275 crores is expected.

- At the year-end, the management expects the net debt level to be close to Rs.300 Cr.

- The company has a majority share in window air conditioners, however, it doesn’t expect any further growth from this segment, instead, growth is expected to come from split & inverter ACs.

Analyst’s View:

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter was decent with 27% YoY growth in revenues and 18% YoY in PAT. The company is adding new customers for its various component-making businesses and has also acquired AmberPR which is expected to add to its already large components portfolio. The business for Sidwal remains steady with an order book of above Rs 450 Cr. The company is also looking to expand globally and has set up its USA subsidiary in Sep for gaining international contracts. The management expects Amber to outpace industry growth and establish itself in the export ODM market slowly. It remains to be seen how the industry demand will be affected by rising RM costs and whether the company will be able to achieve its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q2FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 353 | 233 | 51.5% | 581 | -39.2% | 935 | 427 | 119.0% |

| PBT | -8 | -15 | 46.7% | 10 | -180.0% | 2 | -44 | 104.5% |

| PAT | -5 | -8 | 37.5% | 7 | -171.4% | 1 | -27 | 103.7% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 596 | 421 | 41.6% | 715 | -16.6% | 1311 | 683 | 91.9% |

| PBT | 10 | -0.6 | 1766.7% | 16 | -37.5% | 26 | -36 | 172.2% |

| PAT | 8 | 3 | 166.7% | 11 | -27.3% | 19 | -21 | 190.5% |

Detailed Results:

- The company had mixed quarter with a rise of 41.6% YoY in consolidated revenues while consolidated profits rose to Rs 8 Cr from a profit of Rs 3 Cr last year. But QoQ the company saw revenues fall -16.6% and PAT was down -27.3%.

- The major reason for this QoQ fall was the seasonality of the business.

- Operating EBITDA in Q2 for Amber was at Rs 39 Cr with the margin at 6.6%.

- H1 performance was also good with revenues rising 92% YoY while the company made a profit of Rs 19 Cr vs a loss of Rs 21 Cr last year.

- Operating EBITDA in H1 for Amber was at Rs 88 Cr with the margin at 6.8%.

- The consolidated revenue mix was at 37:63 in Q2 for RAC: Components+Mobility respectively.

- The consolidated revenue mix was at 52:48 in H1 for RAC: Components+Mobility respectively.

- The subsidiary revenues for Q2 were at:

- PICL: Rs 40 Cr

- ILJIN: Rs 91 Cr

- EVER: Rs 50 Cr

- Sidwal: Rs 72 Cr

- Amber added 1 new customer in EVER and 2 new customers in IL JIN.

- The order book for Sidwal stands at more than Rs 425 Cr.

- The company invested Rs 73 Lacs to set up Amber Enterprises USA to expand its global presence.

Investor Conference Call Highlights:

- During the quarter sales of consumer durable goods have rebounded sharply as the pandemic restrictions were eased.

- Higher raw material prices led to an increase in prices of finished goods. However, this was well accepted by the end consumer and there was no significant impact on demand.

- During the quarter the company applied for the PLI scheme in the RAC industry. The management believes that the additional capacity coming under the PLI scheme would have a big multiplier effect.

- The main tailwind behind this PLI scheme is the government’s objective to develop a component ecosystem in India and increase domestic component manufacturing from 25% to 75% of domestic demand.

- The company has signed new customers for gas charging and is now in discussions with OEM/ODMs.

- Sidwal order book currently stands at Rs 450 Cr and more growth is expected with government tailwinds and the rapid expansion of metro networks in India.

- At PICL R&D has been done for BLDC motor and required capex work has also started. The company is in advance talks with large OEMs for BLDC motors.

- In Q2 2,31,000 RACs were sold. H1 sales volumes were at near 7 Lacs. The management is confident of achieving more than 3million for the year.

- Amber has been able to successfully pass on all the commodity prices to its customers which has resulted in revenue growth outpacing volume growth.

- There is a lag of 1 quarter in passing on commodity prices rises. The management doesn’t expect commodity prices to fall.

- Total consolidated net debt stands at Rs 250 Cr.

- Although sales for the industry were impacted due to COVID-19 in Q1, there wasn’t any loss of market share and it only resulted in a rise in inventory levels which have normalized now.

- The company is waiting for approval for its RAC products in US from many customers and it is estimated to take about 1 to 2 years before orders start coming in.

- In motor products, purchase orders are expected from Q1 of next FY from US.

- Working capital has overall reduced from 135 to 84 days and more reduction is expected ahead according to the management.

- Captive consumption during H1 for OEM business in other subsidiaries was INR 23 crores and it is expected to rise to Rs 60-70 Cr by the end of FY22.

- The management expects the market share to increase in FY23 in the RAC segment because of the two upcoming greenfield facilities and the expected conversion of gas charging customers to ODM customers.

- Amber will focus on growing at 400 to 500 bps higher than the industry growth rate according to the management.

- The company is in discussion to convert 4 new customers from OEM to ODM which is expected to add 800k to volumes in FY23.

- Production for heat exchangers, plastic molding, and sheet metal solutions for 3 new customers to begin in Q4.

- IL JIN has developed an inverter PCB which has received approval from 2 large-size customers.

- Amber has also added 2 new customers for commercial refrigeration which should start seeing sales from FY23.

- The management expects to earn Rs 100 crore revenue in the next 2 years from the commercial RAC portfolio and Rs 30 to 50 crore in the current year.

- Approvals in process for washing machines and refrigerators should help IL JIN and Ever double their revenue in the next two years according to the management.

- The capex planned for FY22 is Rs 400 Cr and for Fy23 it is Rs 300 Cr. This is inclusive of growth and maintenance capex.

- Around 35% of PICL’s sales demand comes from Amber.

- The current capacity of BLDC motors is at 8 Lacs which is expected to increase to 2 million post the planned expansion.

- Percentage margins for the company are better in component as compared to fully finished AC assembling selling.

- The current cost of funds for Amber is at 5 to 6% and maintenance capex is at Rs 80 to 100 Cr.

Analyst’s View:

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter was mixed with YoY growth, but QoQ decline due to localized lockdowns leading to a drop in sales. The demand for components is expected to rise significantly with the new PLI scheme coming into play in which the company is applying for 6 out of the total 10 components covered by the scheme. The potential market size for Sidwal is also expected to rise a lot with the announcement of new metro lines in 27 cities. The company is also looking to expand globally and has set up its USA subsidiary in Sep for gaining international contracts. It expects international RAC sales to start in the next 2 years while component exports are expected to start from Q4. The management remains optimistic about Amber exceeding industry growth by 4-5%. It remains to be seen how the industry demand will be affected by rising RM costs and whether the company will be able to achieve its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q1FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 581 | 194 | 199.48% | 1314 | -55.78% |

| PBT | 10 | -29 | 134.48% | 94 | -89.36% |

| PAT | 7 | -19 | 136.84% | 61 | -88.52% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 715 | 262 | 172.90% | 1607 | -55.51% |

| PBT | 16 | -36 | 144% | 116 | -86.21% |

| PAT | 11 | -24 | 146% | 76 | -85.53% |

Detailed Results:

- The company had mixed quarter with a rise of 172% YoY in consolidated revenues while consolidated profits rose to Rs 11 Cr from a loss of Rs 24 Cr last year. But QoQ the company saw revenues fall 55% and PAT was down 85%.

- The major reason for this QoQ fall was the tight lockdown restrictions which led to a drop in sales in April and May.

- Operating EBITDA for Amber was at Rs 50 Cr with the margin at 7%.

- The consolidated revenue mix was at 64:36 in Q1 for RAC:Components+Mobility respectively.

- The subsidiary revenues for Q1 were at:

- PICL: Rs 36 Cr

- ILJIN: Rs 43 Cr

- EVER: Rs 18 Cr

- Sidwal: Rs 50 Cr

- The order book for Sidwal stands at Rs 425 Cr.

Investor Conference Call Highlights:

- The company expects the share of components from domestic sources will rise from 25% to 75% in the next 5-6 years for the Indian RAC industry.

- The company is in talks with 2 new export customers from the Middle East and USA. For the customer in the Middle East, it has already started exporting components and RACs. The USA customer is still in the approval process, and this should be completed by FY23.

- Margin for Sidwal stood at 24.6%. Sidwal is developing new products like dumper ACs for mining, electric AC for electric buses, ACs for harvester combines, and Metro ACs for different climate conditions for Mumbai, Delhi, and Bangalore Metros.

- PICL saw an EBITDA margin at 9% in Q1.

- The company added 5 new customers for ILJIN in Q1.

- The new energy table should add Rs 700 to Rs 1200 to the product pricing, but it should not lead to any drop in demand in the industry according to the management.

- The company maintains a quarterly lag in passing on any rise in RM costs.

- The company has applied for PLI for a Rs 300 Cr investment in the normal RAC category and it is planning to apply for its motor subsidiary for a Rs 50-100 Cr investment.

- The planned investment of Rs 50-100 Cr in PICL is expected to be done over the next 5 years.

- The company is planning to enter into other segments for PCB making like electricals, fans, speakers, wearables, smart switches, and OTT devices. This should help in generating better sales than when making PCBs for consumer durables only.

- Of the 10 components identified by the govt for the PLI scheme, Amber is going to enter into 6 of them.

- The company sold 4.78 Lac RAC units in Q1.

- The company was able to add 2 new customers in Jan or Feb when the import ban was announced. These 2 customers are expected to add at least 8 Lac units to annual sales volumes for Amber.

- The company is aiming to target almost 50% of the current import requirement of the RAC market.

- The possible market size for Sidwal is expected to expand a lot given the recent announcement of almost 1071 km of new metro lines to be laid out in 27 cities.

- The impact from RM prices increases was around 10-12% which was passed on to the customers.

- Although the company is making BLDC motors for RACs only, it can expand into other products in the future given the planned rise in capacity.

- The company is expecting to make Rs 45-50 Cr of revenues from the commercial AC segment in FY22.

- Currently, the segment of commercial AC has only 2 products and the company is looking to add new products to this portfolio.

- The company expects to sell 8000-10000 units to the Middle East in FY22. The company’s products operate in the 50 Hz space, and it is looking to add products to the 60 Hz space as well.

- The company expects growth of 30-40% for the next 3 years from the Middle East.

- The major challenge in exporting to the USA is coming up with a new product line-up since the existing product portfolio may not be suited for USA conditions even though they have been adapted for exports to the Middle East.

- Around 45% of the industry output is outsourced at the moment of which 70% comes from Amber.

- The cost of the electronic units and motors in an AC unit is around Rs 4000 currently of which 60-70% is imported.

- The import substitution opportunity from these AC components is around Rs 1600 Cr in Fy21 and this is expected to grow at a CAGR of 15-16%.

- The 5 new customers for IL JIN were old Amber customers who used to get their invertor PCBs from China.

- The management has identified 4 main milestones for expanding in export markets which are product availability, regulatory clearance, entering the market, and increase market share. The company has already completed the first 2 steps for the Middle East while it is still at the 1st step for USA.

- The market share for the company is at 24%.

- OEM capacity expansion shouldn’t pose a threat to ODMs like Amber according to the management.

- The current capacity for Amber is at 4.5 million units. It is looking to increase it to 6.5-7 million units with the planned capex by the end of FY23.

- After the change in the BE table, the management expects inverter AC market share to rise to as high as 80-85%. Currently, it is at 60%.

Analyst’s View:

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter was mixed with YoY growth, but QoQ decline due to localized lockdowns leading to a drop in sales. The demand for components is expected to rise significantly with the new PLI scheme coming into play in which the company is applying for 6 out of the total 10 components covers by the scheme. The potential market size for Sidwal is also expected to double or triple with the announcement of making new metro lines in 27 cities. It remains to be seen how the industry demand will be affected by rising RM costs and whether the company will be able to achieve its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q4FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1314 | 1045 | 25.74% | 584 | 125.00% | 2326 | 3009 | -22.70% |

| PBT | 94 | 52 | 80.77% | 27 | 248.15% | 78 | 129 | -39.5% |

| PAT | 61 | 53 | 15.09% | 18 | 238.89% | 52 | 118 | -55.93% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1607 | 1315 | 22.21% | 774 | 107.62% | 3064 | 3971 | -22.84% |

| PBT | 116 | 70 | 66% | 40 | 190.00% | 120 | 191 | -37% |

| PAT | 76* | 63** | 21% | 28 | 171.43% | 83 | 164 | -49.39% |

*Contains deferred tax charge of Rs 16 Cr

**Contains deferred tax credit of Rs 11 Cr

Detailed Results

- The company had decent quarter with a rise of 22% YoY in consolidated revenues while consolidated profits rose to Rs 21% YoY.

- Operating EBITDA for Amber was at Rs 147 Cr with margin at 9.2%.

- The consolidated revenue mix has remained unchanged from 55:45 in FY21 and moved to 60:40 in Q4 for RAC:Components+Mobility respectively.

- Working capital days increased to 56 days in FY21 from 37 days in FY20 mainly on account of lockdown in H1FY21.

Investor Conference Call Highlights

- The channel inventory at the end of March 2021 stood at normalized levels.

- The PLI scheme of air conditioners will provide an incentive of 4% to 6% on incremental sales of AC components manufactured in India over 5 years.

- Amber has completed the acquisition of land for the Pune facility and construction has already started. This facility is expected to start operations in Q4FY22.

- Q4 FY ’21 revenues for Sidwal stood at INR 80 Cr with operating EBITDA at INR 21 Cr. FY ’21 revenues for Sidwal stood at INR 201 Cr with operating EBITDA at INR 48 Cr.

- In the recent budget, 26 new cities have been earmarked to have metro lines and 1,700 km of line to be added under metros. This should bring immense opportunity to supply more ACs for metro coaches to Sidwal.

- Revenues for PICL stood at INR 71 Cr in Q4 & INR 131 Cr for FY21. Operating EBITDA stood at INR 6 Cr in Q4 & INR 7 Cr in FY21. The management expects to double the revenues for PICL along with the improvements in margins in the next 2 to 3 years’ time.

- Revenues for IL JIN stood at INR 118 Cr in Q4 & INR 307 Cr for FY21.

- Revenues for Ever stood at INR 59 Cr in Q4 & INR 154 Cr for FY21.

- Amber saw a positive cash flow of INR 115 Cr as against net debt of INR 246 Cr as of 31st March 2021.

- Amber sold around 2.1 million units in FY21 vs industry volumes of 5.1 million.

- Inventory build-up due to local lockdowns should get liquidated as things open in June.

- IL JIN & Ever saw operating EBITDA of Rs 14.65 Cr & Rs 7.34 Cr respectively in FY21.

- The main opportunity from the gas changing operations is to help convert these customers to full manufacturing customers.

- The company is awaiting clarification on how the PLI scheme will apply on the components side of the RAC business.

- With the rising penetration of VRV & VRF air conditioning, Amber is also looking to get into commercial refrigeration with offerings of 5.5 ton, 8.5 ton, 11.5 ton of air conditioning.

- The company is indeed looking for external partners for the software side of the commercial refrigeration business.

- The company has been able to pass on all the RM cost rise to end customers.

- Of the Rs 2300 Cr of standalone revenue, around Rs 320 Cr was for compressors which is a full pass-through item for Amber.

- Around 70% of motors are imported at present in the RAC industry.

- The company is not only targeting import substitution for PICL but also in a China plus one strategy for export destinations.

- Volume drop for FY21 was around 30% YoY.

- The company’s factories are running at 40-45% capacity at present.

- Around 60% of the market today is from inverter ACs.

- Although input metal prices have risen a lot recently, the management expects these prices to stabilize going forward.

- Although competition is rising in the components space, the management is confident of Amber’s prospects mainly due to its price competitiveness which is derived from R&D support and the backward integration of critical components.

- FY22 volumes should generally surpass FY21 volumes as current local lockdowns have not curbed sales as much as the lockdown last year.

- The incremental capex for the next 2 years is around Rs 290 Cr, which is for the 2 upcoming facilities.

- Sidwal has a current order book of Rs 350 Cr which is to be executed over the next 2 financial years.

Analyst’s View

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter was good with good growth in both sales and volumes. The demand for components is expected to rise significantly with the new PLI scheme coming into play. The management has outlined plans for capacity expansion in 2 new sites and for entering commercial air conditioning space with VRV & VRF. It remains to be seen how the industry demand will be affected by the current ongoing local lockdowns and whether the company will be able to achieve its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q3FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 584 | 570 | 2.46% | 233 | 150.64% | 1011 | 1963 | -48.50% |

| PBT | 27 | 6 | 350.00% | -15 | 280.00% | -17 | 77 | -122.08% |

| PAT | 18 | 12 | 50.00% | -9 | 300.00% | -9 | 65 | -113.85% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 774 | 791 | -2.15% | 421 | 83.85% | 1457 | 2656 | -45.14% |

| PBT | 40 | 24 | 67% | -1 | 4100.00% | 4 | 121 | -96.69% |

| PAT | 28 | 25 | 12% | 3* | 833.33% | 7** | 101 | -93.07% |

*Contains negative tax expense of Rs 3.4 Cr

**Contains negative tax expense of Rs 3 Cr

Detailed Results

- The company modest quarter with a decline of 2% YoY in consolidated revenues while consolidated profits rose to Rs 28 Cr.

- Operating EBITDA for Amber was at Rs 62 Cr with margin at 8.2%.

- The consolidated revenue mix has remained unchanged from 55:45 to 54:46 in Q3 for RAC: Components+Mobility respectively.

- 9M revenue mix has come to 50:50 from 60:40.

- Amber has signed 6 new customers since the import ban on Air conditioners with Refrigerants.

- The Company has bought land in Supa region near Pune for its upcoming greenfield project.

Investor Conference Call Highlights

- The PLI scheme for ACs and components is of Rs 5000 Cr and details of this scheme are expected to be finalized soon.

- Q3 FY21 revenues for Sidwal stood at Rs 44 Cr, operating EBITDA stood at Rs 9 Cr and margin stood at 21.4%. 9M revenues for Sidwal stood at Rs 120 Cr with operating EBITDA of Rs 27 Cr with operating EBITDA margin at 22.5%.

- Revenues for PICL stood at Rs 35 Cr, operating EBITDA stood at Rs 3 Cr, and operating EBITDA margin stood at 7.7%. The management expects some margin expansion over the next 2 to 3 years’ time.

- Q3 revenue for IL JIN stood at Rs 91 Cr and in Ever stood at Rs 33 Cr. Operating EBITDA margin for IL JIN stood at 6.3% and Ever stood at 6.6%. 9M revenue for IL JIN stood at Rs 189 Cr and Ever revenue was at Rs 95 Cr, while operating EBITDA margin for IL JIN at 5.3% and for Ever at 3.8% in the same period. IL JIN added 4 new customers and has a few more to be approved.

- Volumes sold in Q3 were at 5,43,000 units vs 5,72,000 units last year.

- Consolidated debt as of 31st Dec 2020 was at Rs 263 Cr vs Rs 343 Cr last year.

- Industry inventory levels have dropped as most brands have pushed a lot of inventory into the primary sales due to the expected cost increases of the product due to commodity and commodity impacts.

- The management has stated that any increase in RM costs will be passed on to end customers. The company will be inserting this kind of price variation clause in all its orders soon.

- The plot in Supa has an area of 10 acres and the company is constructing on 2.5 lac sq feet area initially. It is also adjacent to Toshiba manufacturing plant and Carrier Midea plant. Commercial production in the facility is expected to start by FY22.

- The starting capacity for this plant is around 1 million units and some spare parts capacity.

- The company will be submitting samples for top through window air conditioners in USA which is very different from the models sold in India.

- In overall, RM cost increases are expected to cause prices of finished goods to rise by 5-7% according to the management.

- The management doesn’t feel that a price increase is going to deter most customers as it would be only around Rs 1500-2000. For someone who is looking to upscale from cooler to AC, such a price increase may cause them to move to EMI schemes or postpone the purchase.

- Currently Amber has an overall RAC market share of 24% and RAC ODM market share of almost 70%.

- The company is seeing the opportunities from the import ban on finished goods to unfold in 2 phases. In Phase 1, the company will be supplying finished units to customers till they can set up their manufacturing facilities. In Phase 2, once these customers have their manufacturing setup, Amber can supply them with components for the unit manufacturing.

- The validation phase in the components business takes around 18-24 months and thus the uptake from the components is expected to start rising in 2-3 years.

- There are a total of 15 manufacturers who are servicing a market of 7 million units per year in India.

- Sidwal has grabbed 2 or 3 new orders worth Rs 120 Cr in Q3. The current order book for Sidwal is at Rs 400 Cr which is expected to be executed within the next 2 years.

- The management is also expecting custom duty increases on the component side and the unfinished goods side.

- The company has recently started commercial air conditioner line with 3.5- and 4.5-ton units. The company will also be adding 22 new products in this segment in the next 2 years catering to commercial and industrial applications.

- Mobility applications now account for 5.5% of total revenues for Amber.

- The company will be the first ODM in the commercial AC space and it is thus expecting good response.

- Exports now account for 20% of PICL revenues. The management expect this number to rise to 30-35% in next 2 years.

- Capex guidance is for Rs 300 Cr for the next 2 years for the expansion of the 2 new sites.

- The local procurement of components for the RAC space accounts for only 25% of industry demand. the PLI scheme is looking to increase this number to 75%in the next 5 years.

- The management has stated that setting up a 2 million units’ capacity compressor plant from scratch will take around 18-24 months and Rs 250 Cr.

- The company has already gotten an order from Voltas Beko for refrigerator and washing machine components. It has also gotten 2 customers for washing machine motors.

- In washing machines, Amber is supplying tub assemblies, inverter PCB board, injection molding components, and motors which account for around 25% of washing machine manufacturing.

- In refrigerators, Amber is doing sheet metals, door liner and case liners, and electronics. All of these account for 20-25% of refrigerator manufacturing.

- The components are being supplied for semi-auto and top-loading washing machines only.

- The management expects around 10-15% of revenues to come from exports in the next 4-5 years.

Analyst’s View

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter was good with recovery back to Q3FY20 levels in both sales and volumes. The demand for components has been steadily rising and the company is also looking to supply components for other consumer electronics like washing machines and refrigerators. The management has clearly outlined how the company plans to take the opportunities arising from the import ban on finished goods. It remains to be seen how the industry demand will be affected by the rise in RM costs and whether the company will be able to achieve its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q2FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 233 | 393 | -40.71% | 194 | 20.10% | 427 | 1394 | -69.37% |

| PBT | -15 | -5 | -200.00% | -29 | 48.28% | -44 | 71 | -161.97% |

| PAT | -9 | 5 | -280.00% | -19 | 52.63% | -27 | 53 | -150.94% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 421 | 623 | -32.42% | 262 | 60.69% | 683 | 1865 | -63.38% |

| PBT | -1 | 5 | -112.00% | -36 | 98.33% | -36 | 96 | -137.50% |

| PAT | 3* | 12** | -75.00% | -24 | 112.50% | -21*** | 77 | -127.27% |

*Contains negative tax expense of Rs 4 Cr

**Contains negative tax expense of Rs 7 Cr

***Contains negative tax expense of Rs 15 Cr

Detailed Results

- The company dismal quarter with a decline of 32% YoY in consolidated revenues while consolidated profits fell to Rs 3 Cr.

- Operating EBITDA for Amber was at Rs 22 Cr with margin at 5.4%.

- The management expects normalcy to return in H2.

- ~Rs.4000 crs of RACs were being imported in India of which 70-75% consisted of Completely Build Units have been banned for import. This creates significant opportunity for local manufacturers.

- The consolidated revenue mix changed to 64:36 from 50:50 for RAC: Components+Mobility respectively.

Investor Conference Call Highlights

- The ban on import of refrigerant fill RACs has created an additional opportunity of Rs 4,000 Cr for local manufacturers.

- Amber successfully completed a QIP of Rs 400 Cr in Q2 which got oversubscribed by more than 5.5x. The money raised from QIP has been temporarily being used for paying off the debt, CapEx, working capital, and acquisition of the balance 20% stake of Sidwal.

- The company is getting inquiries, RFQs from big global players for RACs as well as components as per the China Plus One strategy.

- Q2 revenues for Sidwal was at Rs 47 Cr with operating EBITDA at Rs 13 Cr. H1 revenues were at Rs 77 Cr with operating EBITDA at Rs 18 Cr and EBITDA margins of 22%.

- Q2 revenues for PICL was at Rs 17 Cr with operating EBITDA loss at Rs 0.6 Cr.

- PICL has successfully widened its product offering from current PFC motors to BLDC motors. PICL is also in discussion with various customers to launch motors for washing machines and higher voltage motors for the commercial AC segment. It has also been approached with RFQs from various large global manufacturers based out of the U.S. and the Middle East.

- Q2 revenues for IL JIN was at Rs 81 Cr with operating EBITDA at 7.4% vs 5.7% last year. Q2 revenues for Ever was at Rs 45 Cr with operating EBITDA at 5.9% vs 5.4% last year.

- Inventory levels in the industry have normalized to pre-covid levels.

- The management expects Q4 to be a positive quarter for the industry.

- February and March is when the management is expecting a volume increase from this ban on the refrigerant air conditioner import. Largely the impact is expected to be reflected in the next financial year.

- Volumes for Q2 were at 1.9 lac units. Capacity utilization was at 45-50%.

- In components. The company is expecting export orders to come in from FY22 onwards as the development cycle gets completed in FY21.

- The company’s first sample will be ready to be shipped out by January and the rest of FY21 will be reliability testing and approval cycles. FY22 is when export orders should start coming in.

- Amber has started exporting motors and heat exchangers and is talking to some customers for PCBs.

- PICL revenue mix is 20% is exported and 80% is domestic. This ratio is expected to become 60:40 in the coming 2 to 3 years’ time.

- In commercial AC, the company has recently launched 2 new products and is on track to build up the whole portfolio of about 18 to 20 products in the next 2 to 3 years’ time.

- The addressable market for commercial AC is around Rs 6500 Cr.

- In Sidwal, 2 tenders from DMRC, Delhi Metro Corporation for Rs 98 Cr were won in Q2.

- The current order book in Sidwal is at Rs 350 Cr which will be delivered in 18 to 24 months’ time.

- Industry decline in H1 is expected to be at 32-33% in H1.

- The company added 4 new large customers since the announcement of the import ban. All of these 4 had been importing 100% of their requirement earlier. These new customers will start in February onwards.

- On the RAC export front, China and Thailand are the 2 large exporters with volumes of 65 million, 80% from China and 20% from Thailand.

- For the PCB board for IL JIN and Ever, the company has already started getting orders and has started shipping. Mass volumes will start picking up from the next financial year.

- Currently, around 48% of the RAC industry is outsourced with Amber having a market share of 70% in it. The overall industry is growing at a CAGR of 12% while the ODM part is growing at a CAGR of 17-18%.

- Even today, 75% of the components are imported. The import substitution opportunity in components is around Rs 5500-6000 Cr. The addressable market for components is $ 2 billion without counting compressors.

- 60% of component revenues came from non-AC components.

- The long term revenues split in RACs and components is expected to be at 50:50.

- USA & Middle East are 2 geographies that Amber is concentrating on currently.

- The import ban opportunity in terms of volume is around 2.4 million units.

- Of this 2.4 million, 70% was refrigerant filled of which Amber hopes to capture at least 55%.

- Margin expansion in subsidiaries was due to lower expenses.

- The company’s goal is to reach 24% market share in the overall RAC market in India and have the rest 76% have some components in them made by Amber.

- Amber currently has the widest range of products available in the complete room air conditioner range from starting from 0.75 ton to 2 ton in all-star categories from 1 star to 5-star and is doing inverter ACs also. On the component side, it has become a one-stop solution for all components except compressors.

Analyst’s View

Amber Enterprises has cemented its position as a prime AC and white good components manufacturer in India. The performance of the quarter continues to improve from the disruption from COVID-19 in the peak summer season. The demand has been steadily rising since after the lockdown. The industry is widely expected to come back to normalcy by Q4. Despite the loss of sales and reduced activity in 3 of the peak months for the company, the management is optimistic about the company’s prospects due to the increased opportunity from the import ban of refrigerant cooled products in RAC and the steadily rising components businesses. It remains to be seen whether there are any more large scale manufacturing disruptions to come from COVID-19 and whether the company will be able to maintain its optimistic expectations in the exports and components space. Nonetheless, given the massive opportunity size from import substitution, the growth prospects of the industry, and the company’s dominant position in the ODM market, Amber Enterprises remains a pivotal stock in the fast-rising air conditioning industry. However, the current valuation appears to be very stretched for the company.

Q1FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 194 | 1001 | -80.62% | 1045 | -81.44% |

| PBT | -29 | 76 | -138.16% | 52 | -155.77% |

| PAT | -19 | 49 | -138.78% | 53 | -135.85% |

| Consolidated Financials (In Crs) | |||||

| Q1FY21 | Q1FY20 | YoY % | Q4FY20 | QoQ % | |

| Sales | 262 | 1242 | -78.90% | 1315 | -80.08% |

| PBT | -36 | 92 | -139.13% | 70 | -151.43% |

| PAT | -24 | 64 | -137.50% | 63 | -138.10% |

Detailed Results

-

- The company dismal quarter with a decline of 79% YoY in consolidated revenues while consolidated profits fell to a loss of Rs 24 Cr.

- Operating EBITDA for Amber was at Rs (3) Cr.

- The pent-up demand from retail-led to the release of high inventory levels from the channel, which in turn led to an increase in manufacturing orders by OEMs.

- The management expects normalcy to return by Q3/Q4.

- The consolidated revenue mix changed from 69:31 to 61:39 for RAC: Components respectively.

- The increase in contribution was due to early resumptions and order execution from Sidwal for the Mobility Application business.

- The performance for subsidiaries was:

- Sidwal: Sales of Rs 30.1 Cr, EBITDA of Rs 5 Cr

- IL JIN: Sales of Rs 16.7 Cr, EBITDA of Rs (1.7) Cr

- EVER: Sales of Rs 16.8 Cr, EBITDA of Rs (1.2) Cr

- PICL: Sales of Rs 8 Cr, EBITDA of Rs (1.8) Cr

Investor Conference Call Highlights

- The company was operating at 50-60% capacity in June.

- The Govt of India is looking to implement a phased manufacturing plan, for room air conditioner and its components, under which import duties will be hiked in a phased manner over the period of 5 years; to bring air conditioners under the licensing system, and to also introduce a production-linked incentive scheme for air conditioners.

- The company is also seeing good inquiries and RFQs from global RAC players for China Plus One strategy for both finished units & components.

- PICL has successfully widened its product offering from current PFC motors to BLDC motors and is in discussion with various customers to launch motors for washing machines and higher-voltage motors for commercial leasing segment. It has also been approached with RFQs from various large global manufacturers based out of the U.S. and the Middle East. The management expects PICL to double in revenues in the next 2 years.

- The management remains confident of increasing market share for IL JIN and EVER as the market moves towards inverter ACs.

- The order book in July was at 65-70% of last year’s figure. The company saw around 1.5 million RAC units moving out of inventory in Q1.

- The company is developing prototype models for the USA which it expects to launch by December or January. The company may need to add additional capacity once policy reforms are announced for the AC industry. The company currently has an annual capacity of 5 million units.

- The expected capex for these estimated expansions is around Rs 150 Cr which is to be distributed across 2 years.

- The management expects the component ecosystem to rise due to the PLI schemes for the RAC industry which will be beneficial for the company even if it doesn’t manage to get any gains in the RAC space.

- The net working capital days for Sidwal were reduced from 180 to almost 83. Sidwal also plays a role in defense applications. This margin expectation for Sidwal remains strong.

- The company has already gotten an order from a Japanese client for washing machine motors from PICL. It is also developing a unique motor for US markets.

- The company has taken an enabling provision up to Rs 500 Cr capital raise. This can be used for both organic (expanding production capacity) or inorganic (acquisition) opportunities.

- The compressor ecosystem is starting to come up in India. There is a company in Ahmedabad called Highly which has 2.4 million capacity while GMCC, the largest compressor manufacturer in the world, is also opening up a factory in India with an initial capacity of 1.5 million which can be scaled up to 6 million. A large Japanese player is also looking to add a compressor plant in India. All in all, the management believe that dependence on China for compressors will come down a lot in the next 2 years.

- The industry is has done a joint meeting with Hindalco for setting up a facility for aluminum foil which is instrumental in making PCB invertor boards.

- Volumes sold in Q1 were at almost 200,000 units vs almost 1 million sold last year.

- Margins were down for the quarter because the majority of sales were for IDUs which are mostly imported.

- Gross debt for the company is at Rs 550 Cr while cash is at Rs 150 Cr.

- The management expects around 35% of motors business to come from exports as compared to only 10% last year.

- The company is competitive in all segments except some in finished goods for 1 ton and below.

- The management has stated that it will take some time for the company to properly scale up exports especially for components as it takes about 4 to 5 years to build up being a standard supplier to any large customer or multinational companies.

- According to the management, the basic weak spot for the compressor ecosystem is the basic RM of electrical steel which is import-dependent.

- The company has bagged orders of Rs 115 Cr since that start of the pandemic. Its order book currently stands at Rs 555 Cr.

- The maintenance capex per year for the company is currently at Rs 28-30 Cr.